FOMC Analysis and Breakdown: Fed Raises Rates by 25 bps, 'Banking System is Sound', Powell and Yellen Give Contadictory Messages...

Yesterday, the Fed raised rates by 25bps, bringing the fed funds rate to a target range of 4.75% to 5%.

Here were some notable revisions to the FOMC statement in comparison to previous statements:

Highlights that job gains have “picked up in recent months”.

No longer mentions that inflation “has eased somewhat”. Instead, the statement notes that “inflation remains elevated”.

No longer mentions the war in Ukraine.

Mentions that the “U.S. banking system is sound and resilient. Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain.”

Added that “the Committee will closely monitor incoming information and assess the implications for monetary policy”… Increased data dependence.

Changes wording from “ongoing increases in the target range will be appropriate” to “some additional policy firming may be appropriate”. Increased uncertainty.

Highlights from Jerome Powell’s prepared remarks:

“FOMC participants expect supply and demand conditions in the labor market to come into better balance over time, easing upward pressures on wages and prices. The median unemployment rate projection in the SEP rises to 4.5 percent at the end of this year and 4.6 percent at the end of next year.”

“We believe, however, that events in the banking system over the past two weeks are likely to result in tighter credit conditions for households and businesses, which would in turn affect economic outcomes. It is too soon to determine the extent of these effects and therefore too soon to tell how monetary policy should respond. As a result, we no longer state that we anticipate that ongoing rate increases will be appropriate to quell inflation; instead, we now anticipate that some additional policy firming may be appropriate. We will closely monitor incoming data and carefully assess the actual and expected effects of tighter credit conditions on economic activity, the labor market, and inflation, and our policy decisions will reflect that assessment.”

This paragraph is extremely important. The Fed will likely hike less than they would have absent the stress in the banking sector. Exactly how much less will depend on the depth and duration of the stress as well as the effects of tighter credit conditions. Policy decisions are now more data-dependent than ever.

“Reducing inflation is likely to require a period of below-trend growth and some softening of labor market conditions”

Highlights from Jerome Powell’s Q&A with the Press:

“Such a tightening in financial conditions (referring to tighter credit conditions due to recent banking stress) would work in the same direction as rate tightening. In principle as a matter of fact, you can think of it as being the equivalent of a rate hike or perhaps more than that, of course it's not possible to make that assessment today with any precision whatsoever.”

The decision to allow uninsured depositors to be protected at Silicon Valley Bank and Signature Bank was “really not about those specific banks, but about the risk of a contagion to other banks and to the financial markets more broadly”.

Referring to disinflation, “What we didn't have in February, and we still don't have now, is a sign of progress in the non-housing services sector. And that is, that's just something that will have to come through softening demand and perhaps some softening in labor market conditions, we don't see that yet. And that's of course 56 percent of the [core PCE] index”.

On Fed balance sheet expansion over the past few weeks (see here for more info), “The balance sheet expansion is really temporary lending to banks to meet those special liquidity demands created by the recent tensions, it's not intended to directly alter the stance of monetary policy. We do believe that it's working, it's having its intended effect of bolstering confidence in the banking system and thereby forestalling what otherwise have been an abrupt and outsized tightening in financial conditions.”

Highlights from the Fed’s Summary of Economic Projections:

Median GDP growth estimates have been revised down from December.

The unemployment rate is expected to reach 4.5% by end of the year. Current rate at 3.6%.

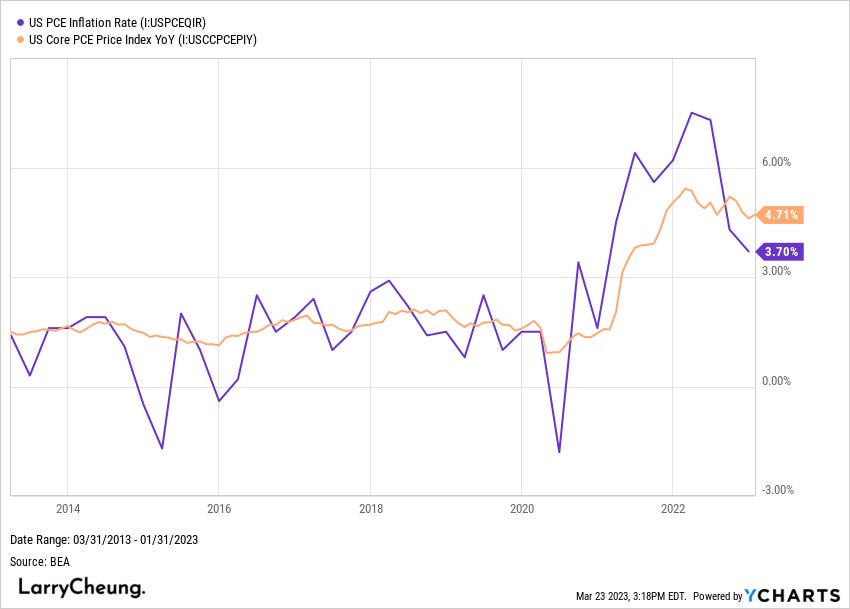

PCE inflation expectations revised up to 3.3% from 3.1% by end of the year.

Core PCE inflation is expected to fall to 3.6%.

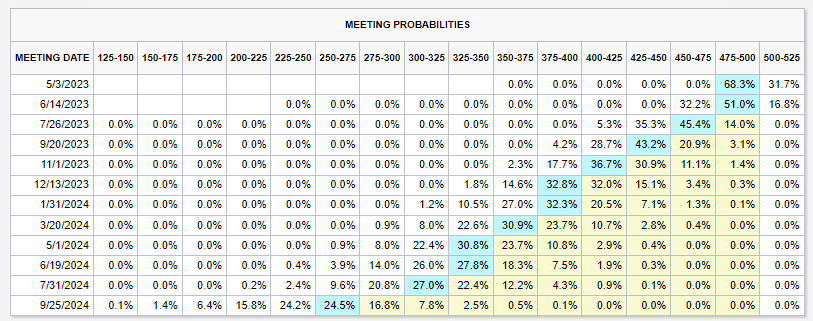

The majority of FOMC participants expect the Fed funds rate to end 2023 at 5.00%-5.25%, implying just one more 25 bps this year. This is quite different from market probabilities as fed fund futures are pricing zero hikes and four rate cuts this year.

Jerome Powell mentioned in the press conference that “rate cuts are not in our base case”. In other words, if financial stability continues to deteriorate, rate cuts are in the cards.

Contradicting Messages…

What I found most interesting from yesterday were the contradicting messages that Jerome Powell and Janet Yellen gave regarding depositors.

When Jerome Powell was asked, “Are you saying that de facto deposit insurance covers all savings?”, he responded, “I think depositors should assume that their deposits are safe”.

However, when Janet Yellen was asked whether the Treasury would circumvent Congress to insure all depositors, Yellen responded, “I have not considered or discussed anything having to do with blanket insurance or guarantees of all deposits”. When asked about a broad increase in deposit insurance, Yellen noted that it was “not something that we have looked at. It is not something we are considering”. Quite the mixed signals.

Main Takeaways

Fed views recent banking stress as equivalent to a rate hike as financial conditions have dramatically tightened. Apollo Global Management believes that the impact of recent banking stress is equivalent to a 150 bps rate hike…

Monetary policy decisions are more data-dependent than ever as the Fed explicitly states it will closely monitor the ”actual and expected effects of tighter credit conditions on economic activity, the labor market, and inflation”.

Still a large spread between FOMC participants’ dot plot projections and fed fund futures pricing. The dot plot implies one more 25 bps hike this year and no cuts. Fed fund futures pricing no hikes and four cuts this year.

Still no consensus on how to approach insuring depositors. As a guest on Bloomberg TV described, “Powell essentially said that all deposits are safe, Yellen said, ‘Hold my beer.’ You would have thought that they would have coordinated”…