Banks Borrow Most Since 2008, First Republic Bailed Out, ECB Hikes 50 bps, Recession Odds Climb...

Banks Borrow Most Since 2008, First Republic Bailed Out, ECB Hikes 50 bps, Recession Odds Climb...

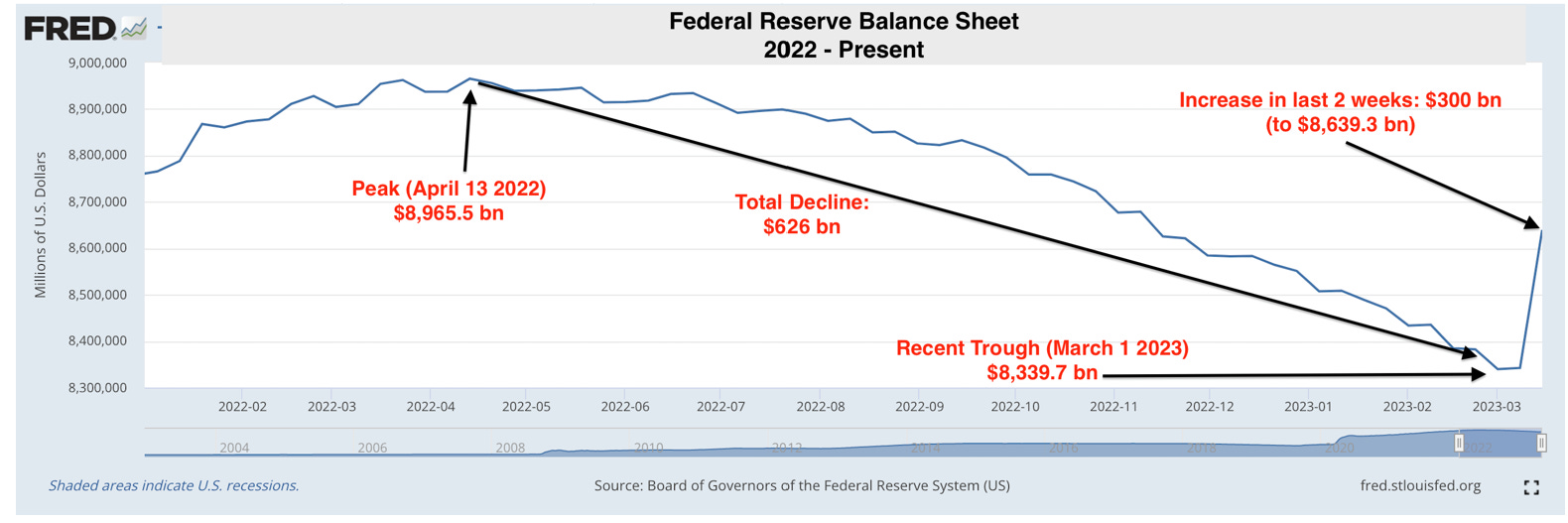

And just like that, I guess quantitative tightening is over.

Over the past 2 weeks, the Fed’s balance sheet has expanded by $300 billion, which has reversed almost half the net amount of its 11-month QT program ($626 bn).

There are two major reasons for this change of direction.

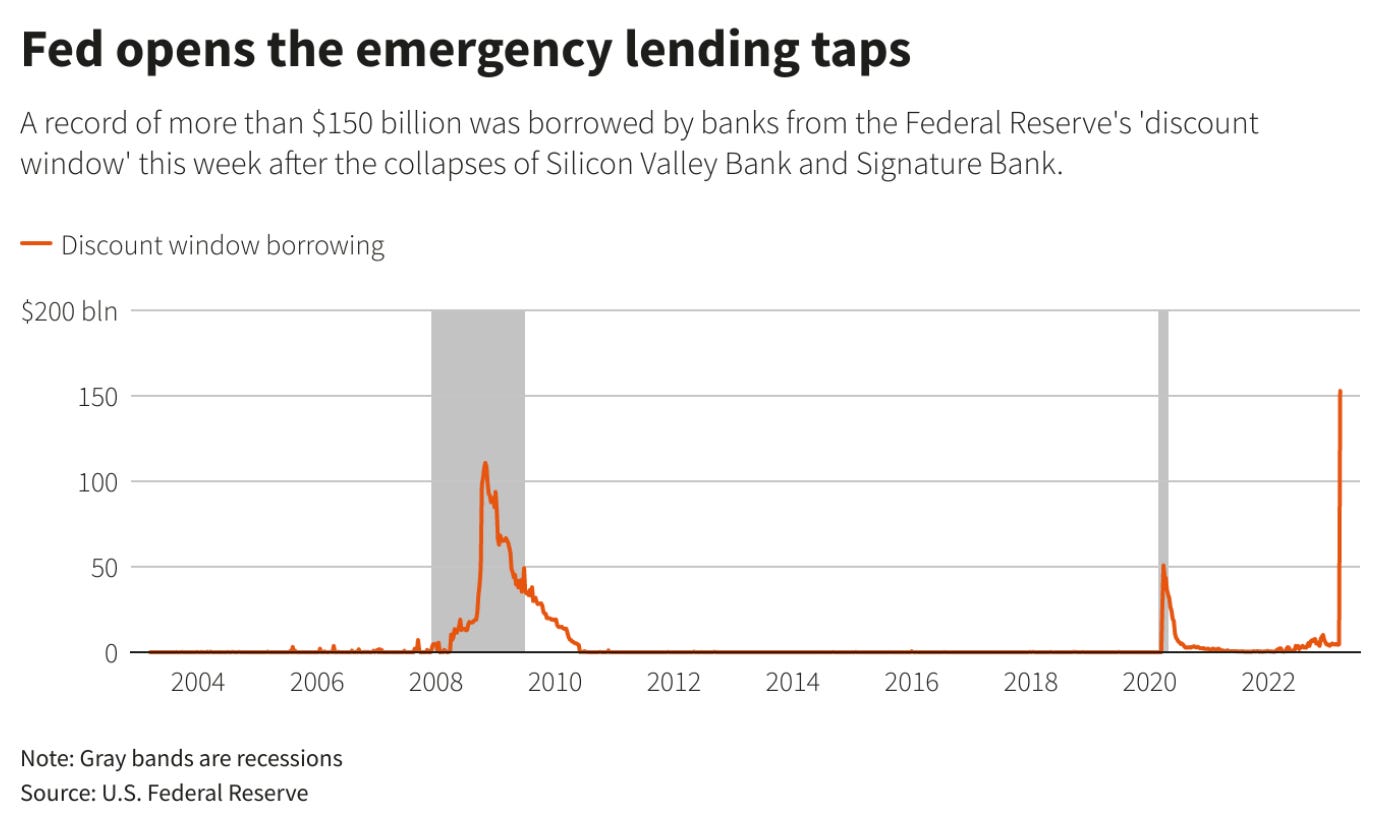

The first is an increase of $148 billion in bank usage of the Fed's Discount Window. This is a facility the Fed provides where banks can post collateral and receive cash in return. The discount window usage over the past few weeks trounced the prior record of $112 billion in the fall of 2008, during the most acute phase of the financial crisis.

The second is a $143 billion increase in collateralized loans made to banks insured by the Federal Deposit Insurance Corporation (FDIC).

These two actions highlight the fact that banks are needing liquidity to satisfy potential/actual deposit withdrawal requests. In order to meet these demands, banks are resorting to handing over securities to the Fed in exchange for the necessary cash.

While supporting the banking system through a period of uncertainty is worth doing, the optics of reducing the balance sheet and then also increasing it right when trouble pops up is awkward and counterproductive.

This expansion in the Fed’s balance sheet will almost certainly come up during next week’s post-FOMC Jerome Powell press conference.

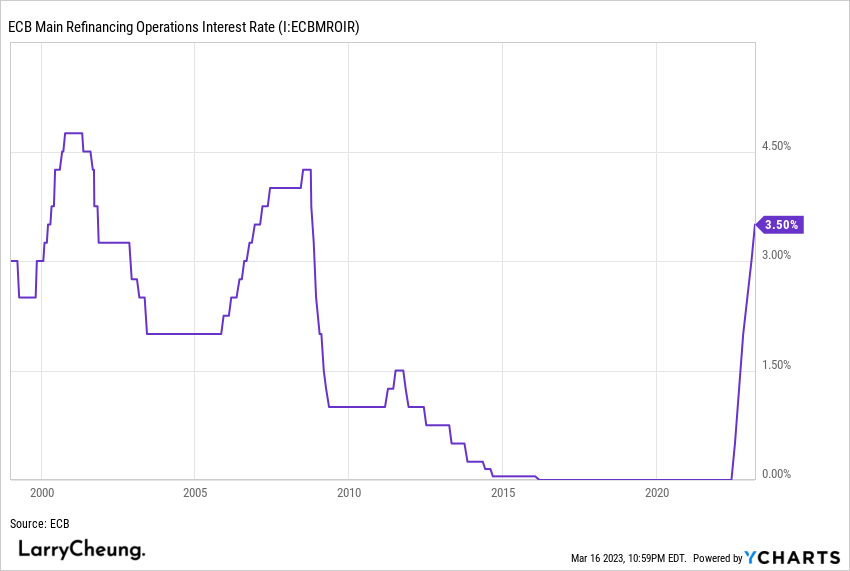

Despite the recent struggles of Credit Suisse, the European Central Bank (ECB) raised rates by 50 bps, above the 33bp priced ahead of the decision, as inflation was projected to remain“too high for too long.”

President Lagarde revealed in the press conference that today’s decision had received a large majority approval, while only a few members had preferred to wait to observe the situation.

That said, the ECB was quick to note that "the Governing Council is monitoring current market tensions closely and stands ready to respond as necessary to preserve price stability and financial stability in the euro area."

It also noted that "the euro area banking sector is resilient, with strong capital and liquidity positions" and added that "the ECB’s policy toolkit is fully equipped to provide liquidity support to the euro area financial system if needed and to preserve the smooth transmission of monetary policy."

Prices continue to rise at a rapid pace across the European Union. Initial estimates show inflation was 8.5% in the 12 months through February 2023, down a tick from the 8.6% the prior month.

In new economic projections released yesterday, ECB officials anticipate inflation will average 5.3% this year. Their estimates show inflation won't fall close to its 2% target until 2025 when they project it'll reach 2.1%.

A long way to go…

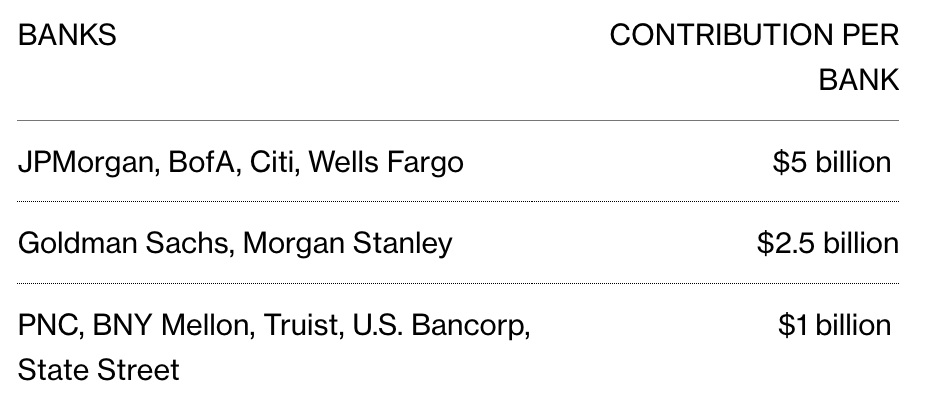

America’s biggest banks announced yesterday that it would deposit as much as $30bn with First Republic Bank (FRC) in an effort supported by the US government to stabilize the bank.

First Republic execs were obviously very thankful:

“We would like to share our deep appreciation for Bank of America, Citigroup, JPMorgan Chase, Wells Fargo, Goldman Sachs, Morgan Stanley, Bank of New York Mellon, PNC Bank, State Street, Truist, and U.S. Bank.

Their collective support strengthens our liquidity position, reflects the ongoing quality of our business, and is a vote of confidence for First Republic and the entire U.S. banking system”.

While the crisis for First Republic Bank is temporarily avoided, the implications are quite scary.

As Bianco Research noted, “Tier 2 bank First Republic is signaling it cannot survive as a stand-alone bank anymore. This signals wider problems for all regional banks. This loss of confidence in regional banks means there has been a sudden and significant contraction of credit availability for the economy”.

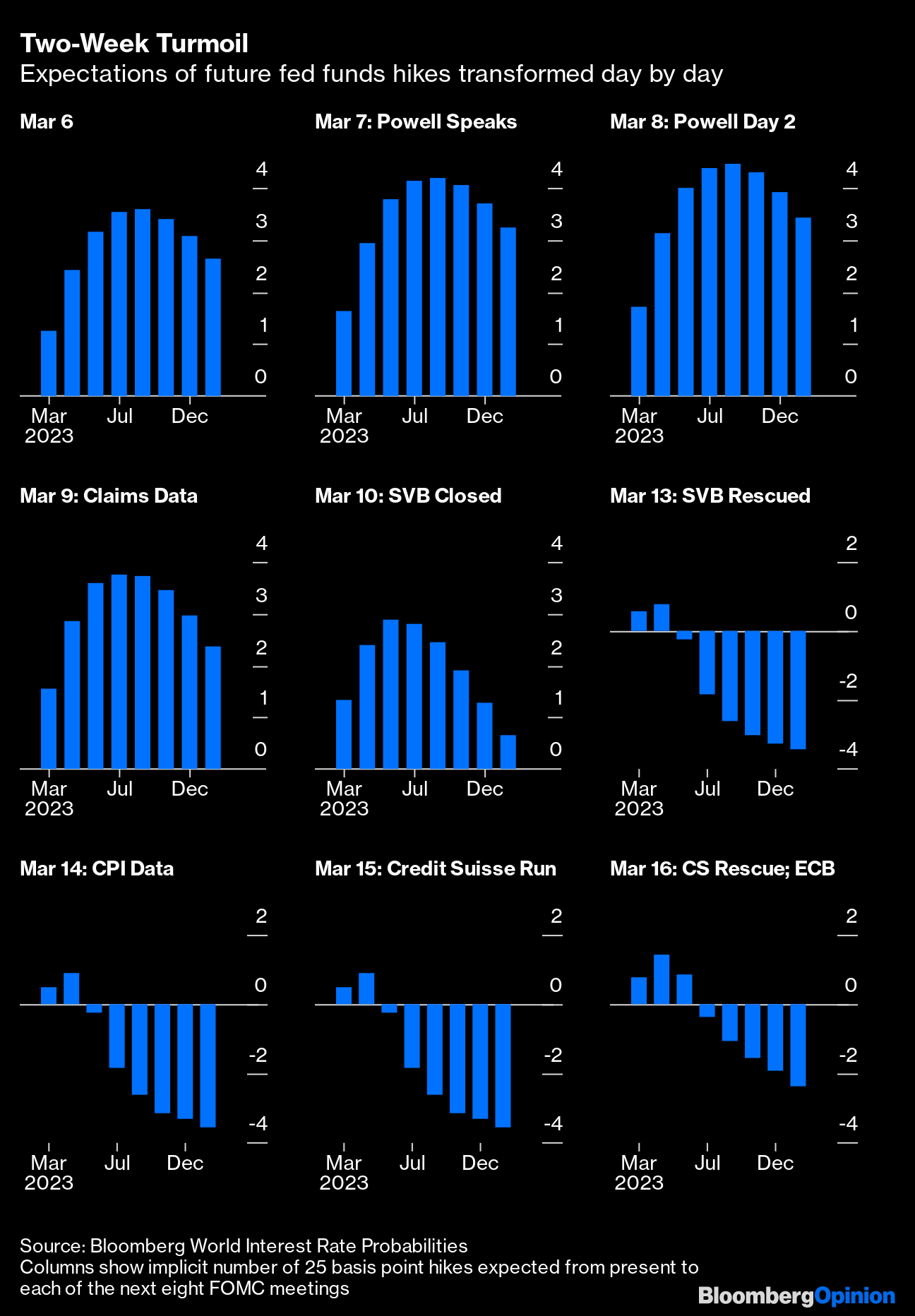

It still blows my mind how much fed fund futures have moved over the past week…

Goldman recently raised its recession odds to 35%, from 25% due to “increased near-term uncertainty around the economic effects of small bank stress”.

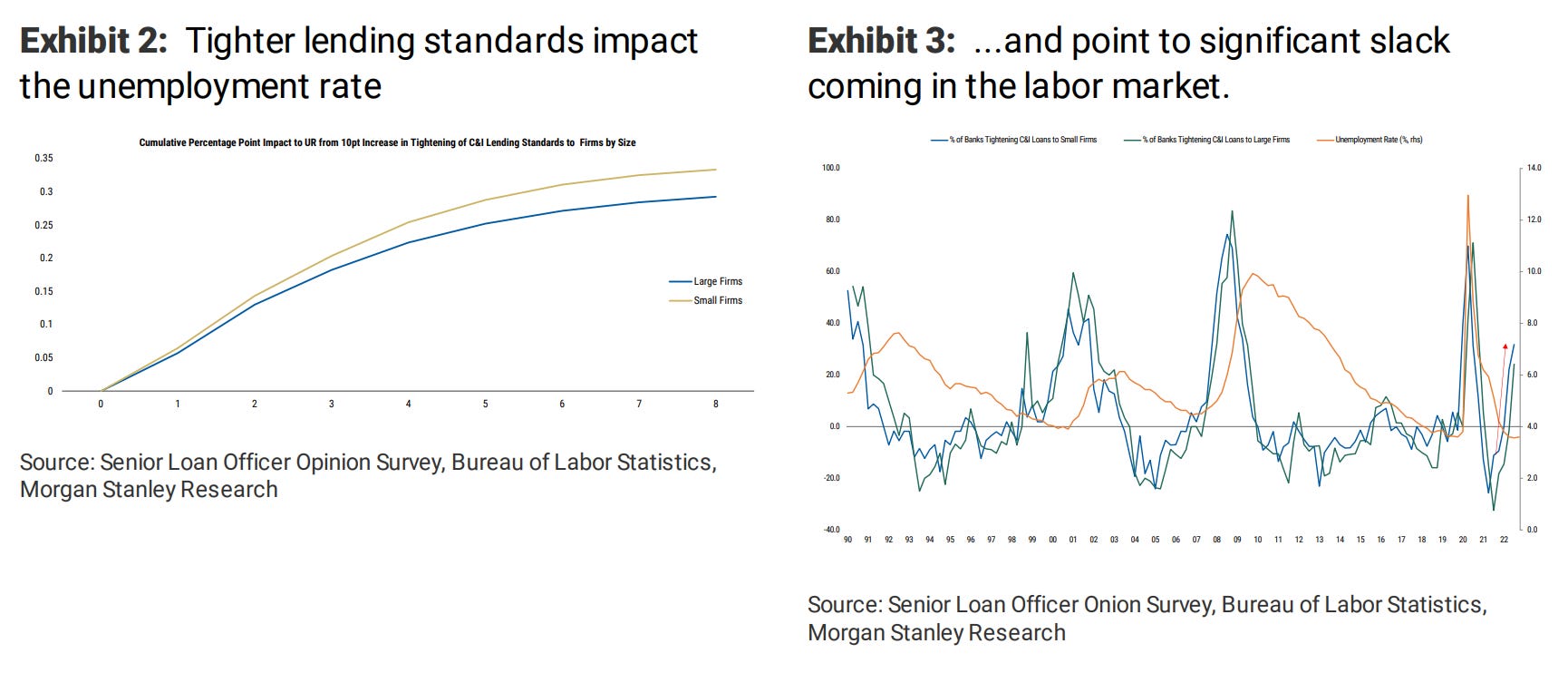

This reasoning is pretty similar to Morgan Stanley, who wrote a note yesterday titled “Tighter Lending Threatens Growth & Jobs Outlook”. In the note, it discusses a “meaningful slowdown in growth and job gains over the coming months, and the prospect of substantial tightening in credit conditions raises the risk that a soft landing turns into a harder one”.

The bank pointed out that during the 2008 financial crisis, lending standards for small firms tightened by 100pts, and the unemployment rate increased by 4.5%. From 3Q21 through 1Q23, lending standards have tightened by 70pts, which may imply a 2.5% increase in the unemployment rate over the next two years.

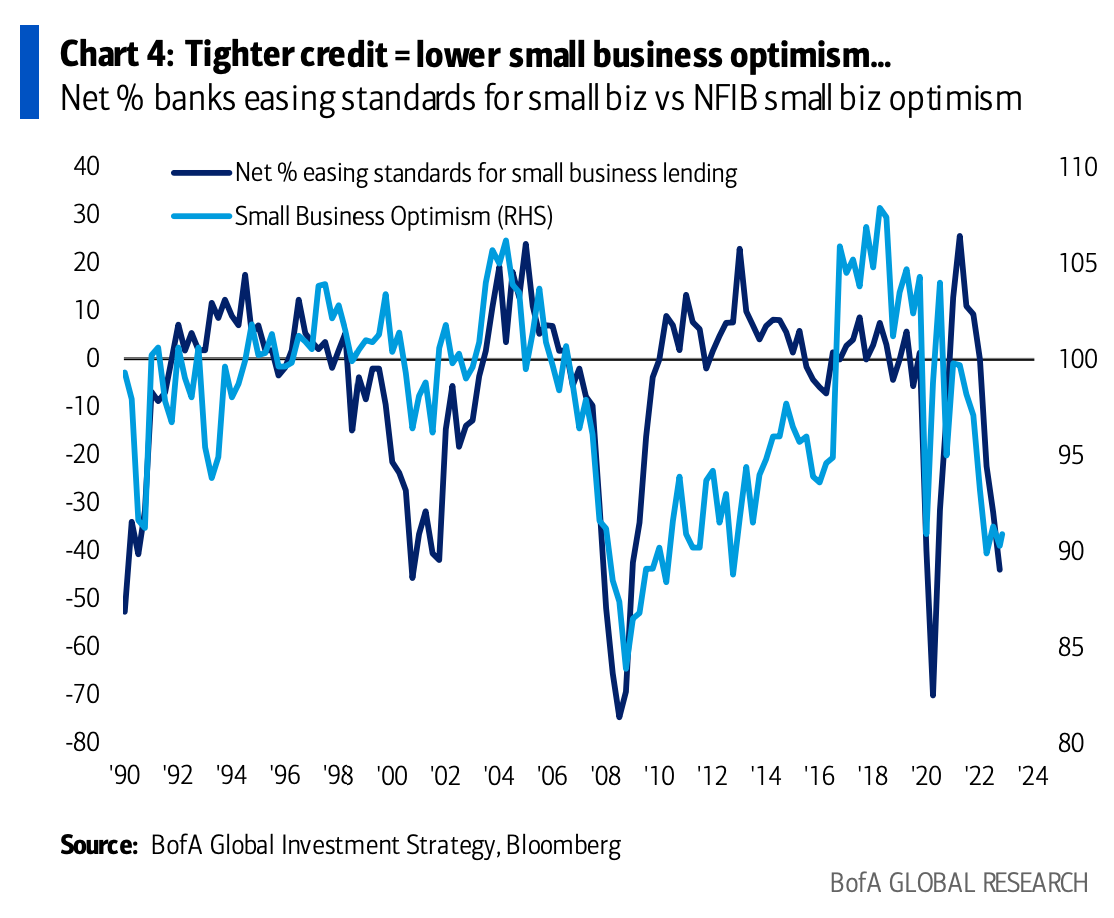

The risk of tighter lending standards was also noted by BofA’s Michael Hartnett’s thinking, who wrote yesterday:

2023 = credit crunch = recession: banking crises are followed by tighter lending standards (they have been getting tighter in recent quarters – Chart 3) and lower risk appetite…small businesses most negatively affected as most reliant on regional bank lending (tighter credit = lower small business optimism – Chart 4); US small businesses create 2/3 jobs in America so lower availability of credit causes surge in unemployment (see credit & claims – Chart 5); note banks with under $250bn of assets make up 80% of commercial real estate lending & with v high US office vacancy rates (18.7% in 4Q22)…commercial real estate widely seen as next shoe to drop.

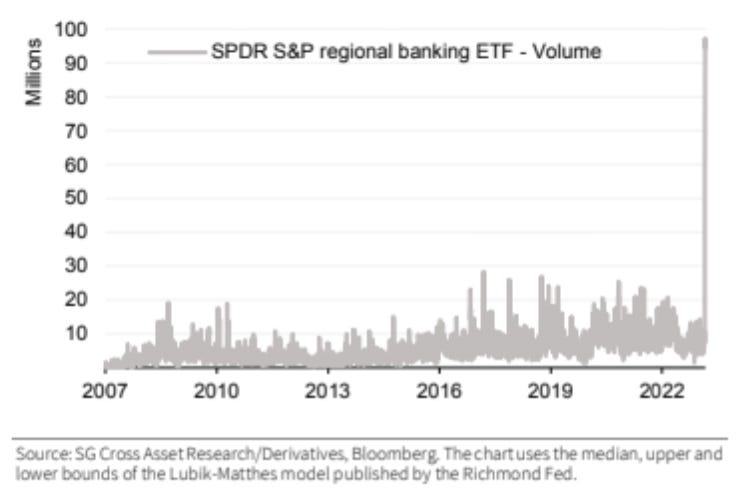

To round it out, here were two charts from SocGen that caught my eye.

Volume on March 10th and March 13th was 10x the normal volume… Total inflows into the Regional Banking ETF since March 7th is equal to 63% of the AUM…

Recent rally in yields is likely due to 1) concerns over the health of the economy + 2) short covering of negative positions by levered funds… There is extreme short positioning on short-term US bond futures…

Thanks for reading! I really appreciate the support. :)

Sources

Research from BofA, Goldman Sachs, Morgan Stanley, SocGen

https://www.cnbc.com/2023/03/16/banks-take-advantage-of-fed-crisis-lending-programs-.html

https://www.reuters.com/markets/us/banks-sought-record-fed-liquidity-wake-svb-collapse-2023-03-16/

https://www.ecb.europa.eu/press/pr/date/2023/html/ecb.mp230316~aad5249f30.en.html

https://www.axios.com/2023/03/16/europe-bank-rate-hike-banking

https://www.zerohedge.com/markets/first-republic-bank-shares-crash-exploring-strategic-options

https://www.barrons.com/articles/first-republic-bank-stock-deposits-ad1e2334?mod=hp_LEAD_1

https://www.axios.com/2023/03/16/first-republic-rescue-markets