UBS acquires Credit Suisse, Central Banks Inject More Liquidity, Equities Stay Expensive, Tech Sees Major Inflows...

UBS acquires Credit Suisse, Central Banks Inject More Liquidity, Equities Stay Expensive, Tech Sees Major Inflows...

The big news of the weekend was UBS's acquisition of Credit Suisse.

UBS will be paying CHF 3bn (US$3.25 billion), or 0.76 per share, specifically shareholders of Credit Suisse will receive 1 share in UBS for 22.48 shares in Credit Suisse. The price per share marked a 99% decline from Credit Suisse’s peak in 2007. As part of the deal, the Swiss National Bank is offering UBS CHF 100bn in liquidity assistance while the government is granting a CHF 9bn guarantee for potential losses from assets UBS is taking over.

What I found fascinating about this deal was that the AT1 (Additional Tier 1) bondholders will see their bonds written to zero. Meanwhile, equity holders will get CHF 3bn.

AT1 bonds, short for Additional Tier 1 bonds, were introduced in Europe after the 2008 global financial crisis to help protect banks during tough times. AT1 bonds are structured to either convert into shares or cause bondholders to incur lasting losses if a bank's financial strength drops below a specific threshold. This mechanism helps improve the bank's financial situation, supporting its balance sheet and enabling it to continue operating.

In the Swiss National Bank’s press release, it wrote:

With the takeover of Credit Suisse by UBS, a solution has been found to secure financial stability and protect the Swiss economy in this exceptional situation.

Both banks have unrestricted access to the SNB’s existing facilities, through which they can obtain liquidity from the SNB in accordance with the ‘Guidelines on monetary policy instruments’.

Treasury Secretary Yellen and Fed Chair Jerome Powell also released a joint statement:

We welcome the announcements by the Swiss authorities today to support financial stability. The capital and liquidity positions of the U.S. banking system are strong, and the U.S. financial system is resilient. We have been in close contact with our international counterparts to support their implementation.

Yesterday the Fed announced a "coordinated central bank action to enhance the provision of U.S. dollar liquidity".

The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Federal Reserve, and the Swiss National Bank are today announcing a coordinated action to enhance the provision of liquidity via the standing U.S. dollar liquidity swap line arrangements.

To improve the swap lines' effectiveness in providing U.S. dollar funding, the central banks currently offering U.S. dollar operations have agreed to increase the frequency of 7-day maturity operations from weekly to daily. These daily operations will commence on Monday, March 20, 2023, and will continue at least through the end of April.

The network of swap lines among these central banks is a set of available standing facilities and serve as an important liquidity backstop to ease strains in global funding markets, thereby helping to mitigate the effects of such strains on the supply of credit to households and businesses.

Dollar swap lines allow other central banks to borrow dollars from the Fed in exchange for their own currencies. The foreign central banks can then supply dollars locally to ease any strains. The Fed usually provides access to these swap lines when there’s a squeeze on the availability of dollars.

Just last week, we discussed how over the past 2 weeks, the Fed’s balance sheet has expanded by $300 billion, which has reversed almost half the net amount of its 11-month QT program ($626 bn). And now, we get a dollar liquidity swap line…

It makes you wonder how bad this banking crisis really is…

So given fears of financial stability, where might the markets take us? Per BNP Paribas, “when the markets made lows in each of the past recessions, it was against a backdrop of rapidly declining rates. When equities made lows in 2020, 10y rates had fallen at through >100 bps, in 2002 and 2008 by >200 bps. In all three instances, the 6-month realized correlation between rates and equities peaked around +80%”.

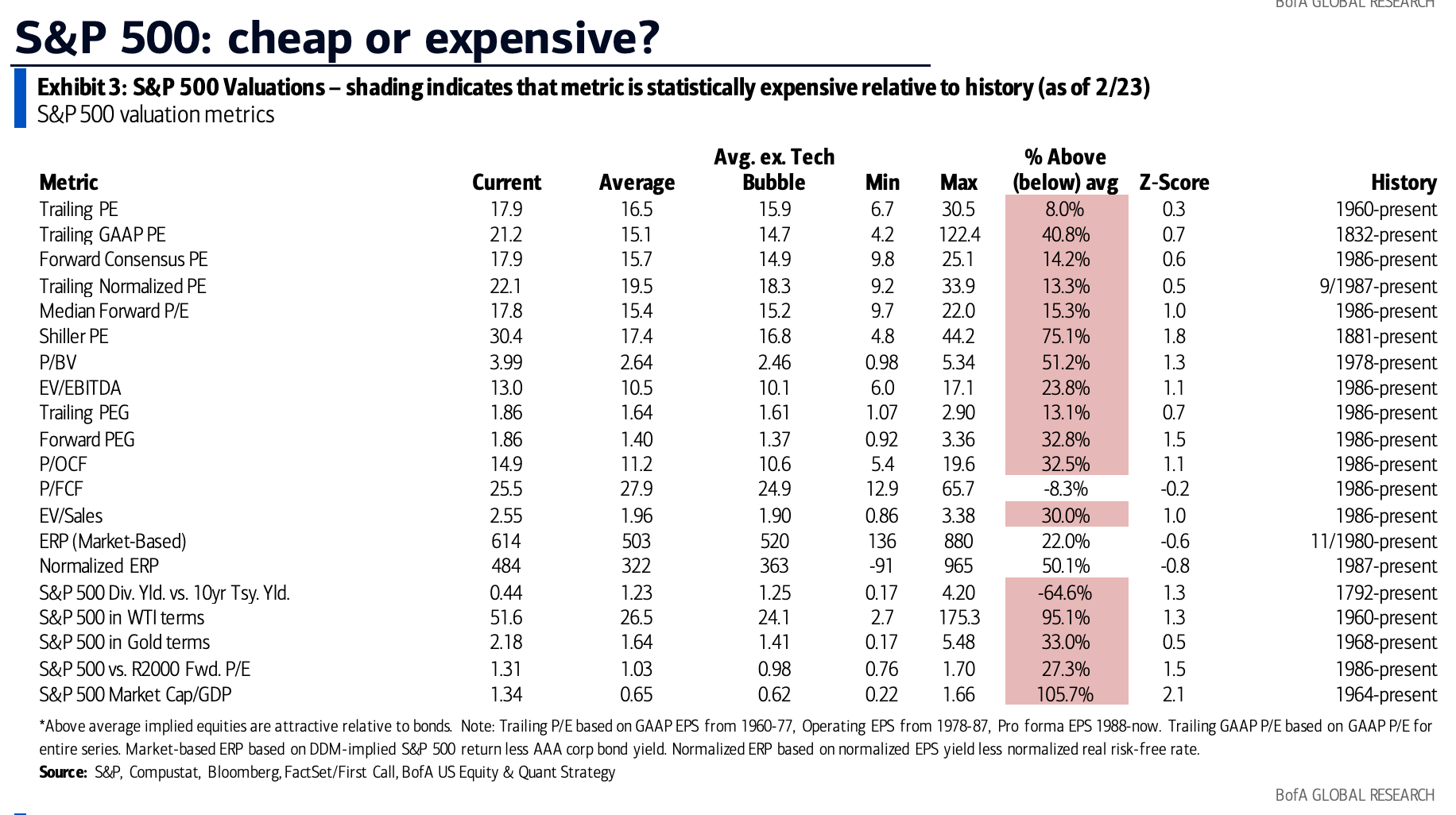

In the meantime, equities still don’t look attractive… Goldman notes that the second valuation problem (besides multiples) for equities is that there is a much higher hurdle rate.

Cash rates are higher and, with zero risk and volatility, cash and short-duration debt look very attractive relative to equities. This is particularly so given that the US 10-year bond yield is well above the dividend yield, and the real (TIPS) yield is about the same as the dividend yield. With greater uncertainty about the near-term path for profits, the risk/reward remains poor.

While the stock market still looks expensive in general, it’s possible that a potential buying opportunity is approaching.

Morgan Stanley’s Mike Wilson wrote in a note Sunday pointing out that the events of the past few weeks could mean that “credit availability is decreasing for a wide swath of the economy, which may be the catalyst that finally convinces market participants the equity risk premium (ERP) is way too low. We have been waiting patiently for this acknowledgment because with it comes the real buying opportunity”.

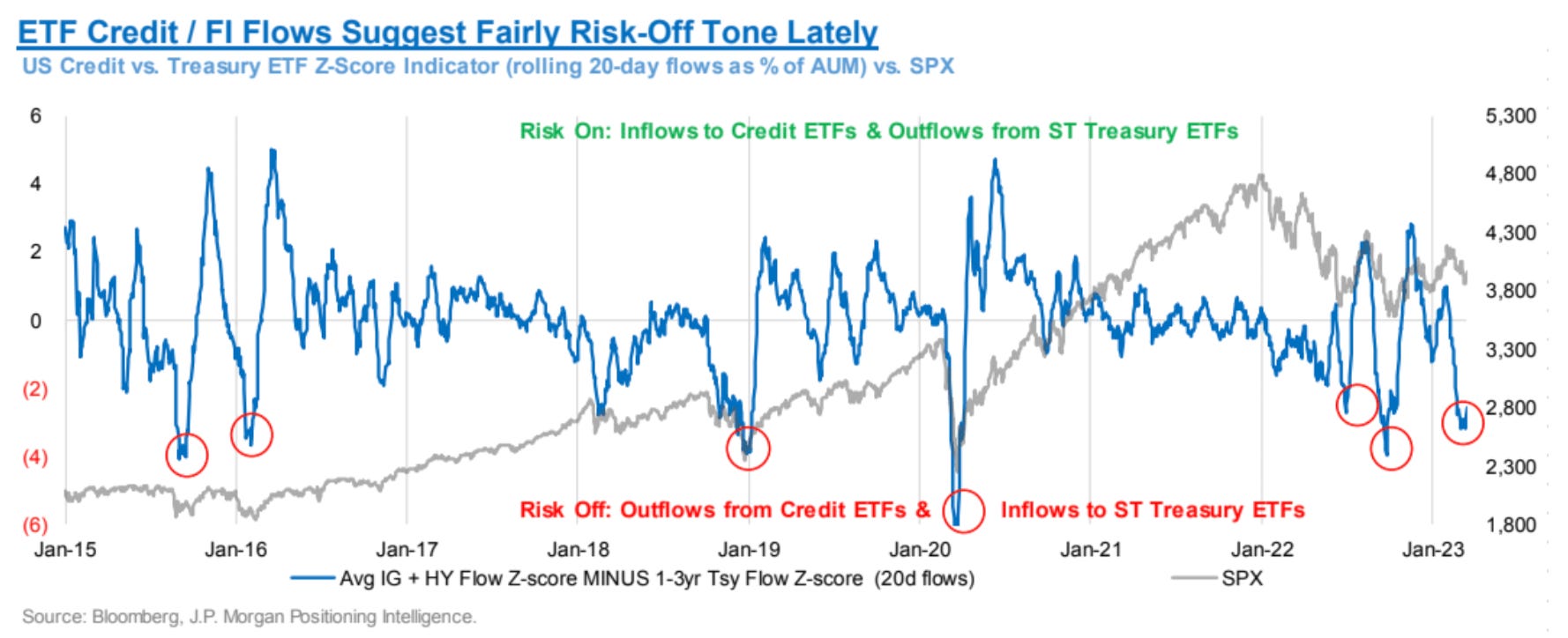

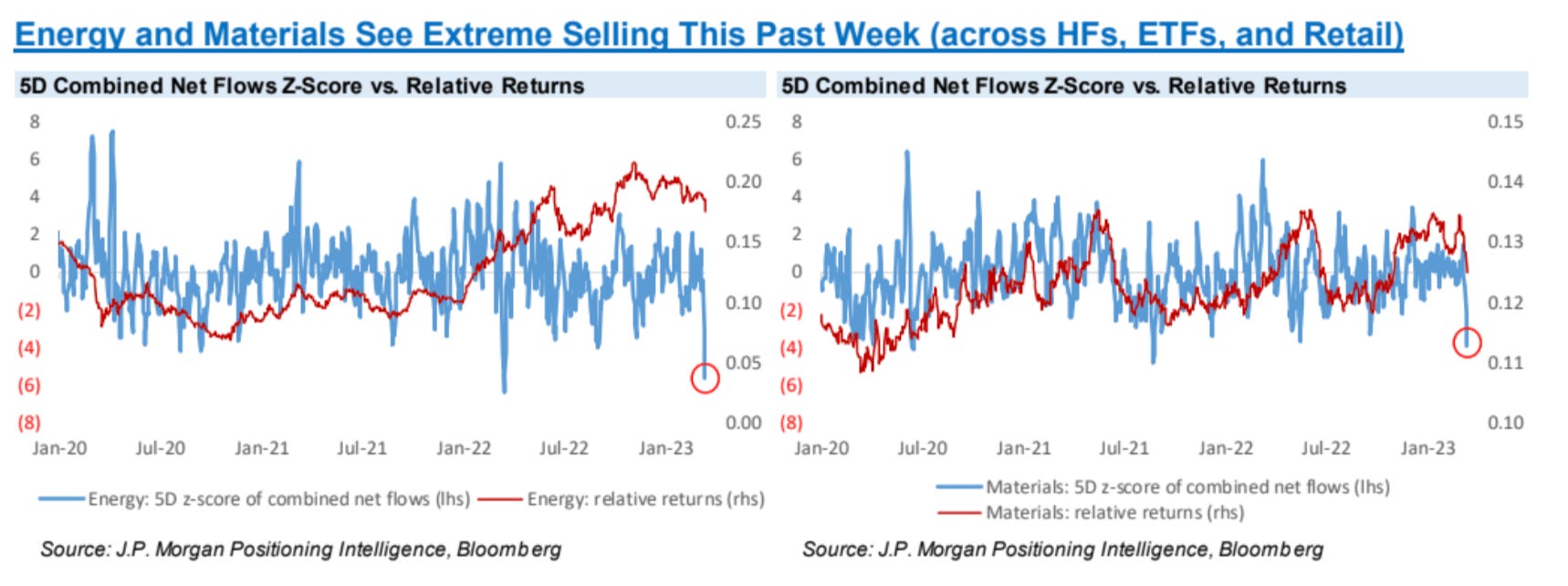

To wrap it off, here were some interesting data points I came across from JP Morgan’s Prime Group on investor positioning.

Hedge Funds added shorts hovering around the +2 z-score level on a 4-week rolling basis. “Given how similar periods of large short additions have coincided with near-term market lows, there could be risk of an upside reversal once again.”

The outflows from Credit ETFs vs. inflows to short-term Treasury ETFs are very negative and could be troughing. “This tends to trough with equity markets, which is why we’re watching this dynamic closely.”

“Mega cap tech has been among the most net bought groups with +2z net buying over the past 10 days and net exposure rising rapidly.”

Meanwhile, energy and materials have seen extreme selling as hedge funds, retail, ETF flows all turned negative in the past week. “The 5-day net selling of Energy and Materials is among the most extremely negative we’ve seen in the past few years.”

Research from BofA, Goldman Sachs, BNP Paribas, JP Morgan, Morgan Stanley

https://www.federalreserve.gov/newsevents/pressreleases/monetary20230319a.htm