The Paradox of Rising Rates, Assets Surge for the Ultra Wealthy, Student Loan Repayments Begin

The Paradox of Rising Rates, Assets Surge for the Ultra Wealthy, Student Loan Repayments Begin

The Paradox of Rising Rates

Higher rates, in theory, can slow down a red-hot economy. But things don’t always work as planned… For many companies, higher rates have actually boosted profits and spending power.

High-quality borrowers weren’t affected by the increased rates, as they had secured low interest rates during the pandemic with bonds set to mature further in the future than at any other time this century. The rise in rates doesn't immediately influence their borrowing expenses, impacting only when bonds are refinanced, but they instantly profit more from their accumulated cash.

This brings a very unique impact on the economy. Ideally, rate increases raise the cost of capital for companies, which means spending less. Instead, if companies are profiting more at higher rates, they can raise dividends, buy back more stock, and invest more, all supporting shareholders and the economy.

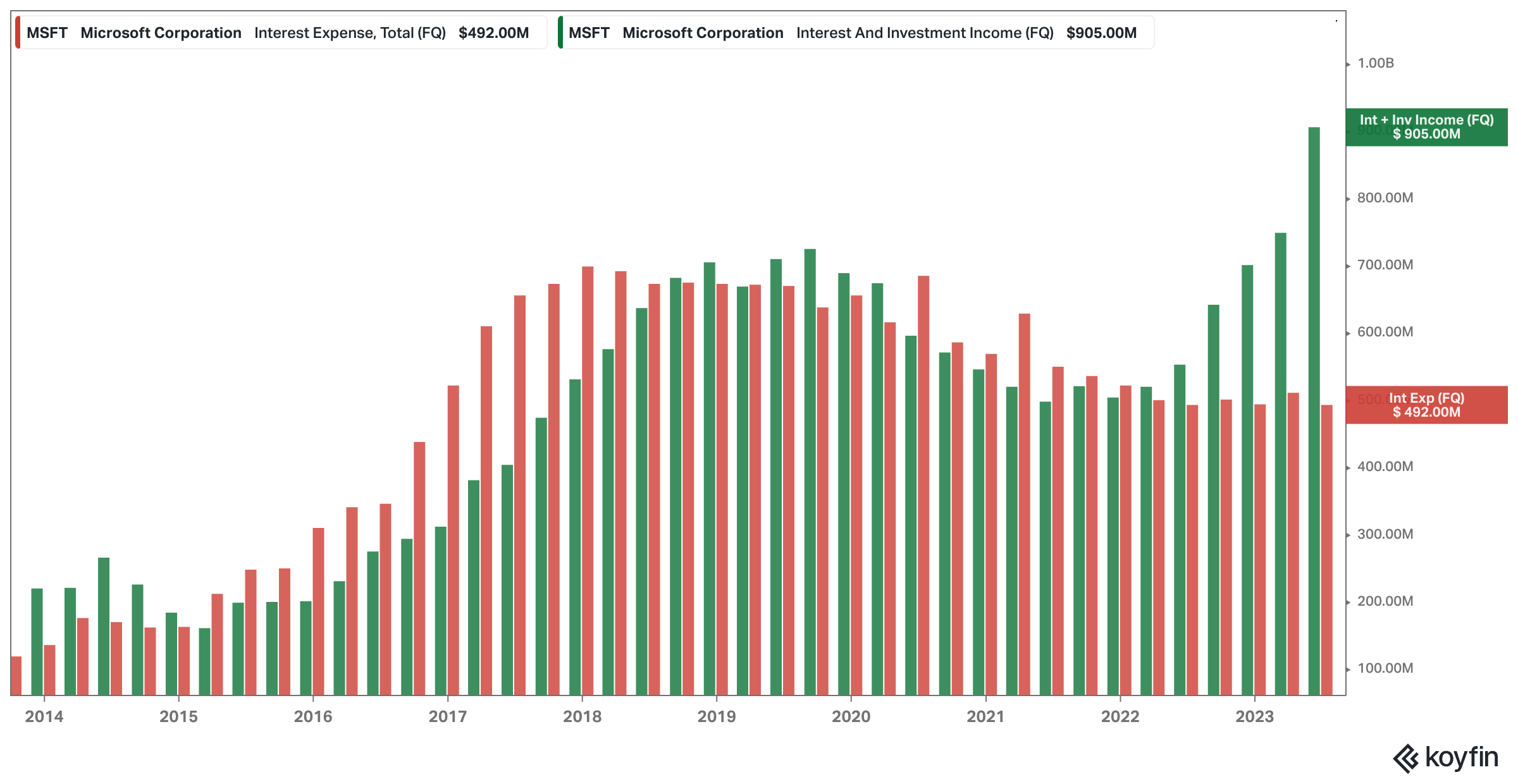

For instance, Microsoft has more cash and short-term liquid investments than debt and has fixed borrowing costs. It paid $492 million in interest in its latest quarter, the exact same amount as a year earlier. However, the amount Microsoft earned on its cash and short-term investments was very different than a year earlier. It earned $905 million in interest just in the quarter, up from $552 million.

On aggregate, corporate net interest payments, the interest paid on debt minus that received on savings, fell as interest rates rose, the opposite of what usually happens.

Even for weaker companies, the pain from higher rates has been surprisingly minimal. The quant research team at SocGen found that the interest rate being paid by the largest 10th of companies in the S&P 1500 index is barely up from its lows and still below its prepandemic peak. Meanwhile, the rate paid by the smallest half of companies in the index has risen to the highest in more than a decade, while those in the middle are roughly back at prepandemic rates.

The Fed is in a rough spot. It either raises rates even higher, squeezing vulnerable companies, or keeping rates high for long enough to where companies locked in low rates will need to refi at higher rates.

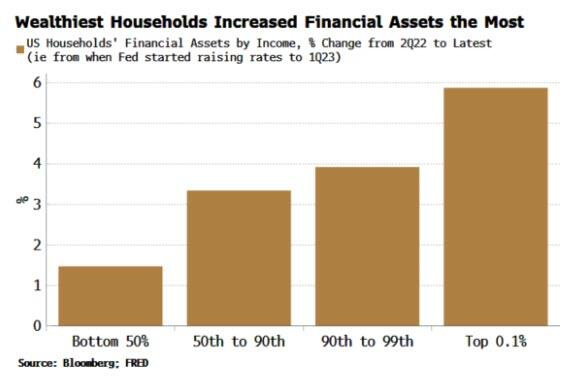

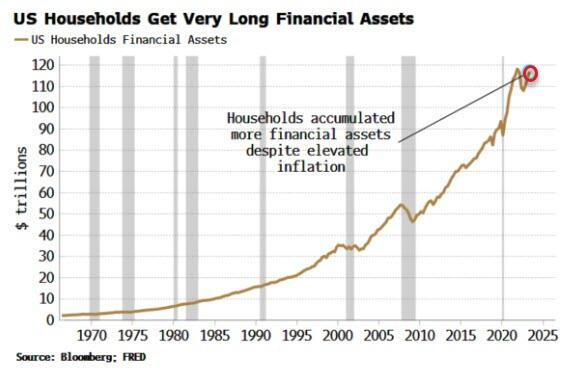

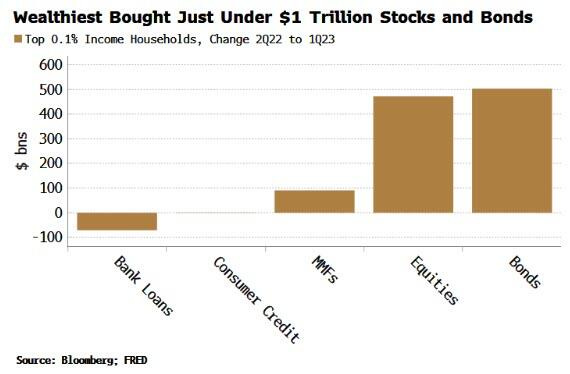

Financial Assets Surge for the Wealthy While Lower-Income Households Lean on Credit

Per Bloomberg, the top half of the highest-earning US households have increased their ownership in financial assets to near all-time highs.

The 90th to 99th-percentile top households by income (those earning ~$210k-$570k per year) increased their holdings of financial assets the most, by over $1.5 trillion to $43 trillion between Q2’ 22 and Q1’ 23.

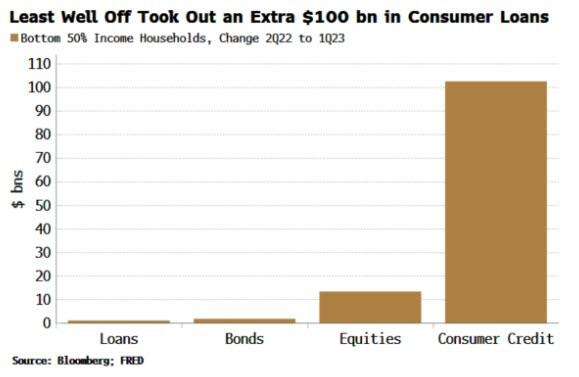

The least well-off households (those in the bottom half, earning under $70k a year) saw the smallest increase, only $36 billion, taking their total to $2.5 trillion.

The top 0.1% of households, who have at least $38 million of annual income, added over $1 trillion in stocks and bonds between Q2’ 22 and Q1’ 23. They also added some exposure to money market funds.

Meanwhile, the bottom half of households own the smallest amount of financial assets, so it’s not surprising their increase in stocks and bonds has been minimal. However, the $100 billion rise in consumer credit, taking the total to $2.7 trillion, is pretty concerning.

This jump is even more concerning when you factor in that it was the lower-income households who were seeing the fastest wage rises. Now though, the wage growth of those in the bottom quartiles is falling the most, meaning that their reliance on credit will rise just as borrowers are facing more difficulty from banks tightening lending standards.

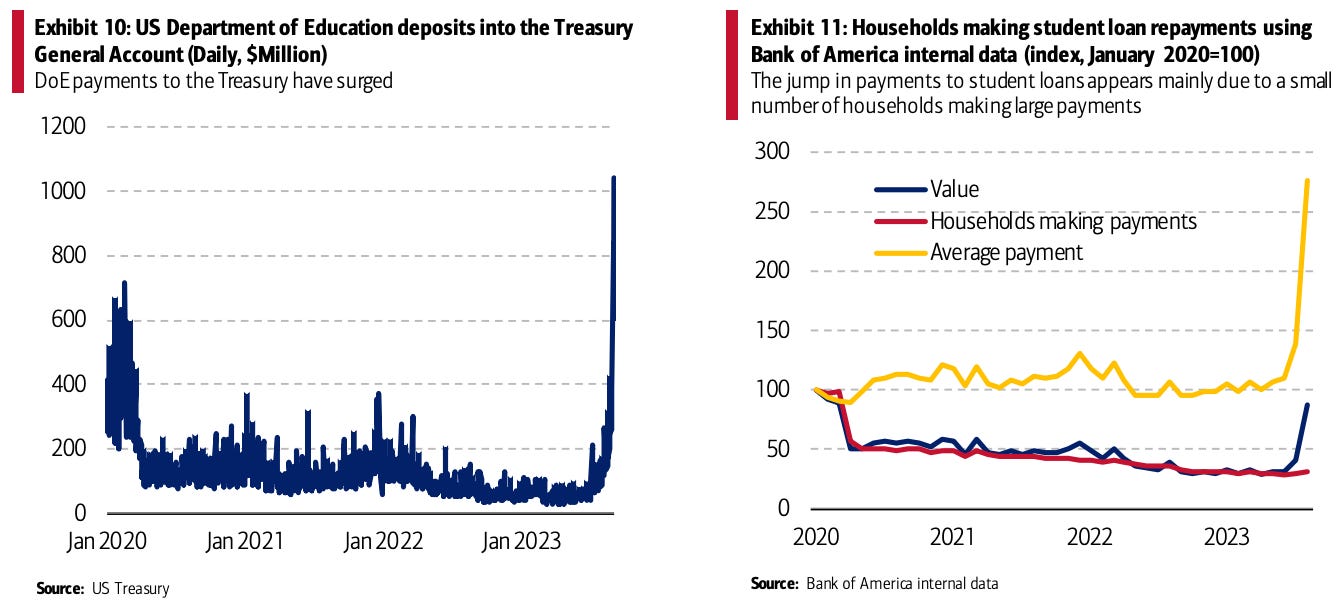

Early Moves on Student Loan Repayments as Spending Sees Mild Uptick

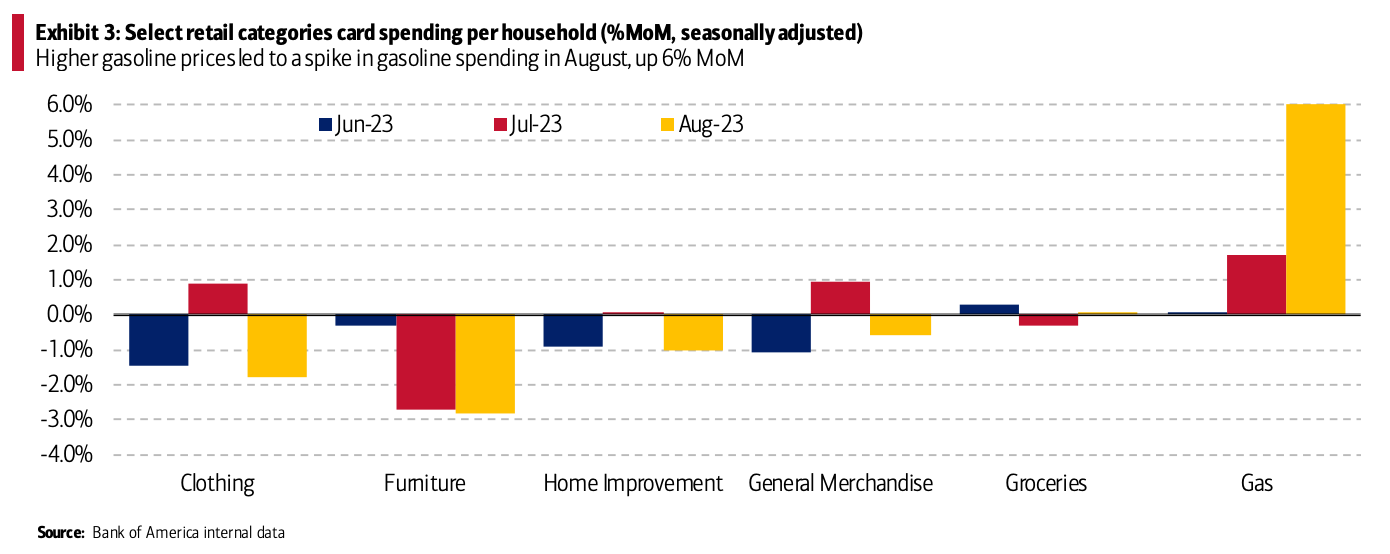

In August, consumer spending in the US remained largely stable. Per BofA, total card spending per household increased by 0.4% year-over-year (YoY), a slight rise from 0.1% in July.

There's a notable trend related to student loan repayments. Even though the formal resumption of these repayments is set for October, Bank of America's internal data has shown a spike in such payments in August.

This trend is likely due to a small subset of borrowers choosing to clear their remaining debt or making lump-sum repayments ahead of the interest resumption that began on September 1.