SVB Finally Acquired, Financial Risk Lying Everywhere, Mixed Signals Coming from the Housing Market

SVB Finally Acquired, Financial Risk Lying Everywhere, Mixed Signals Coming from the Housing Market

Silicon Valley Bank has been acquired!

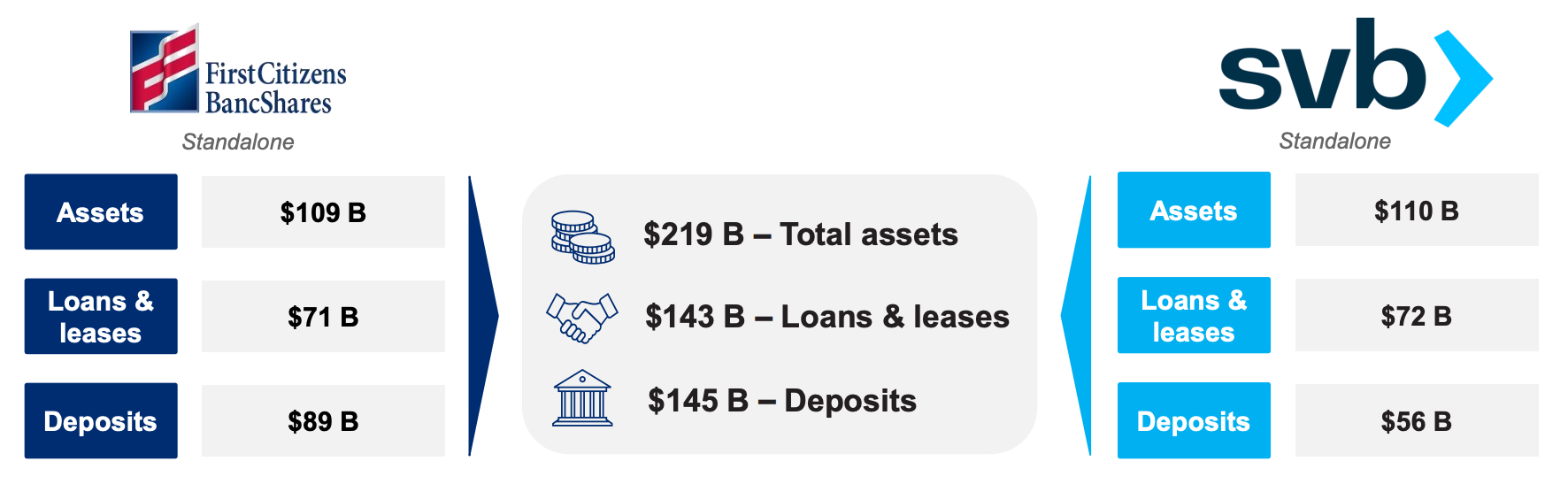

The Federal Deposit Insurance Corporation (FDIC) entered into a purchase and assumption agreement for all deposits and loans of Silicon Valley Bridge Bank, National Association, by First–Citizens Bank & Trust Company, Raleigh, North Carolina.

The 17 former branches of Silicon Valley Bridge Bank, National Association, will open as First–Citizens Bank & Trust Company on Monday, March 27, 2023.

According to the FDIC, the acquisition includes $119 billion in deposits and $72 billion of SVB's loans at a discount of $16.5 billion (23% off). Meanwhile, around $90 billion of SVB's securities will remain under FDIC receivership. In addition, the FDIC will get equity appreciation rights in First Citizens Bank with a potential value of $500 million.

Here’s the part of the FDIC statement that caught my eye:

The FDIC and First–Citizens Bank & Trust Company entered into a loss–share transaction on the commercial loans it purchased of the former Silicon Valley Bridge Bank, National Association. The FDIC as receiver and First–Citizens Bank & Trust Company will share in the losses and potential recoveries on the loans covered by the loss–share agreement.

Loss-share agreements allow the FDIC to absorb a portion of the loss with the purchases of a failing bank. It’s important to know that these loss-share agreements do not result in a bill for the taxpayer. Any loss-sharing payments are made from receivership funds from the failed bank, in this case, SVB, or from the FDIC’s Deposit Insurance Fund, which is funded by other banks.

In the SVB’s case, the FDIC expects the cost of the failure of SVB to its Deposit Insurance Fund to be approximately $20 billion, the costliest in the history of the fund.

In addition to the loss-share agreement, the FDIC also provided First Citizens Bank with a $70bn line of credit to help meet liquidity needs that arise as it integrates SVB into its operations. It also provided the bank with a five-year, $35 billion loan at a 3.5% interest rate to help finance the deal.

It’s almost as if the government is paying First Citizens to take SVB off its hands and giving them everything it can to make sure it can work. As a Bloomberg journalist comically described the situation, “In other words, Silicon Valley Bank is a broken-down jalopy on the government’s driveway and FDIC is giving First Citizens a case of beer to cart it away and fix it up”.

The WSJ had a great piece yesterday titled “Where Financial Risk Lies, in 12 Charts”. Here were the stats that caught me eye.

Deposits are increasingly uninsured. “Nearly $8 trillion of deposits at the end of 2022 were uninsured, up nearly 41% from the end of 2019”.

“Nearly 200 banks would be at risk of failure if half of uninsured depositors pulled their money from the banking system, according to a paper published by economists from the University of Southern California, Northwestern

“Unrealized losses on commercial real-estate debt securities reached $43 billion last quarter. Banks held $444 billion of these securities at the end of 2022.”

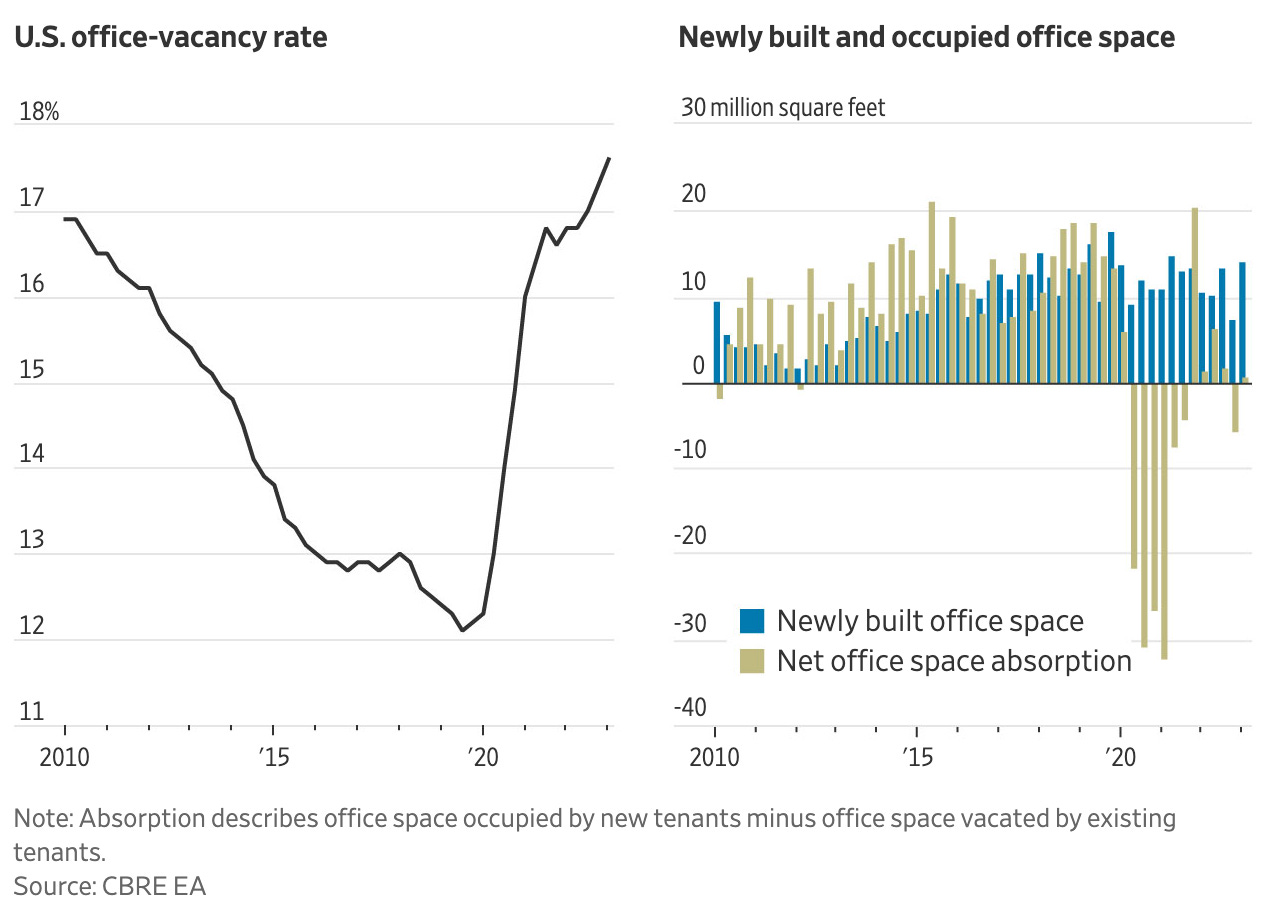

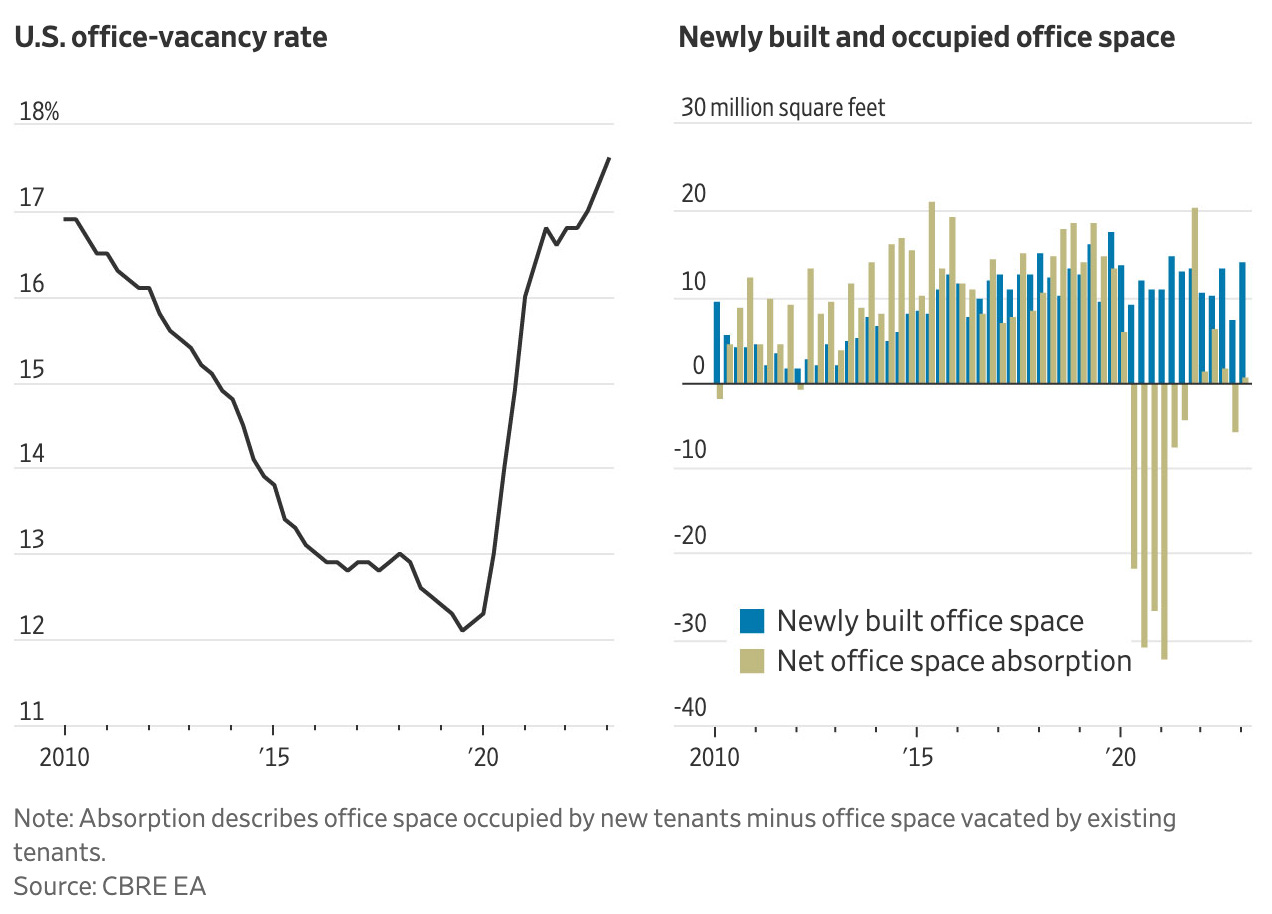

Office-space vacancy rates are expected to keep rising through 2024.

Small banks hold $2.3 trillion in commercial real-estate debt, or 80% of commercial mortgages held by banks.

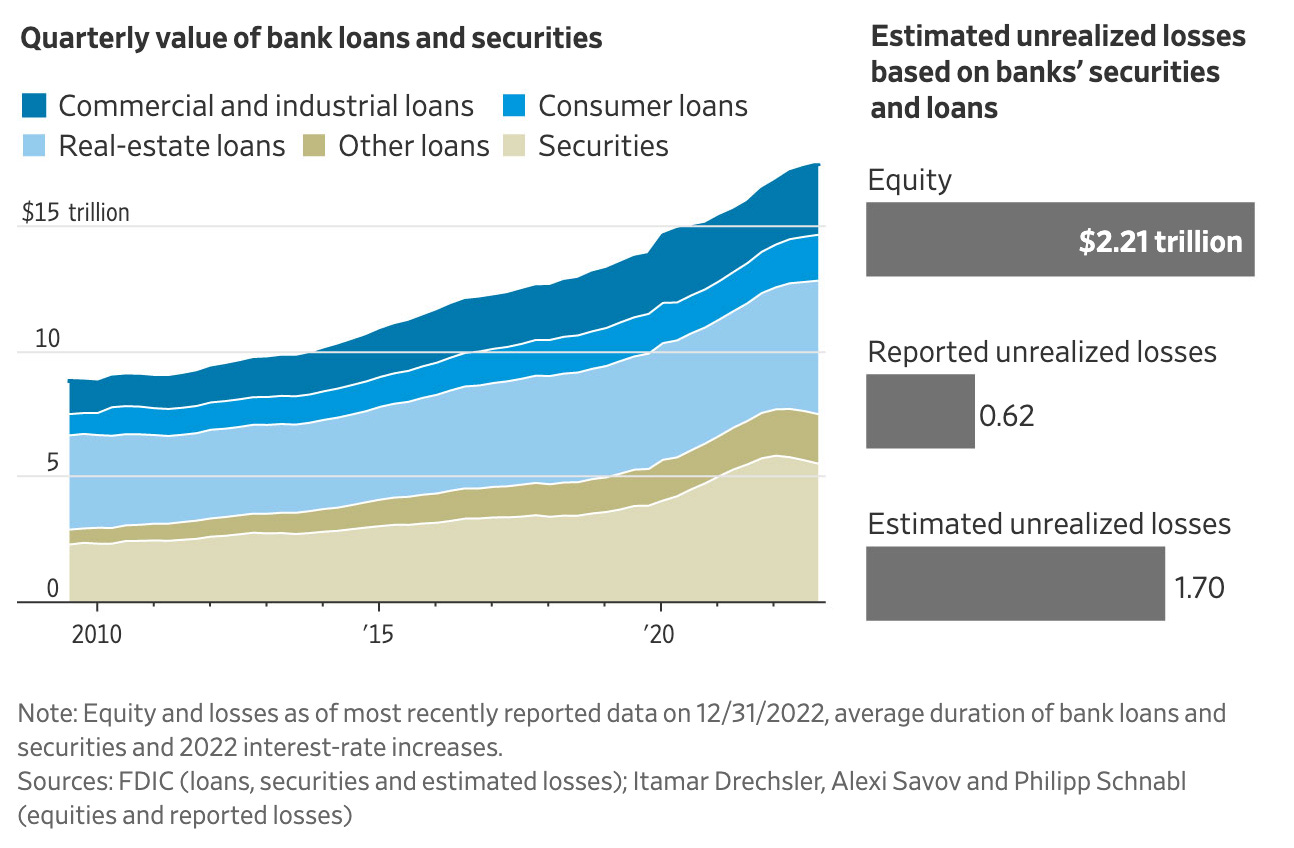

Banks hold $17.5 trillion in loans and securities while equity in the banking system is more than $2 trillion. According to a paper by NYU professors, the estimated unrealized losses on total bank credit reached $1.7 trillion.

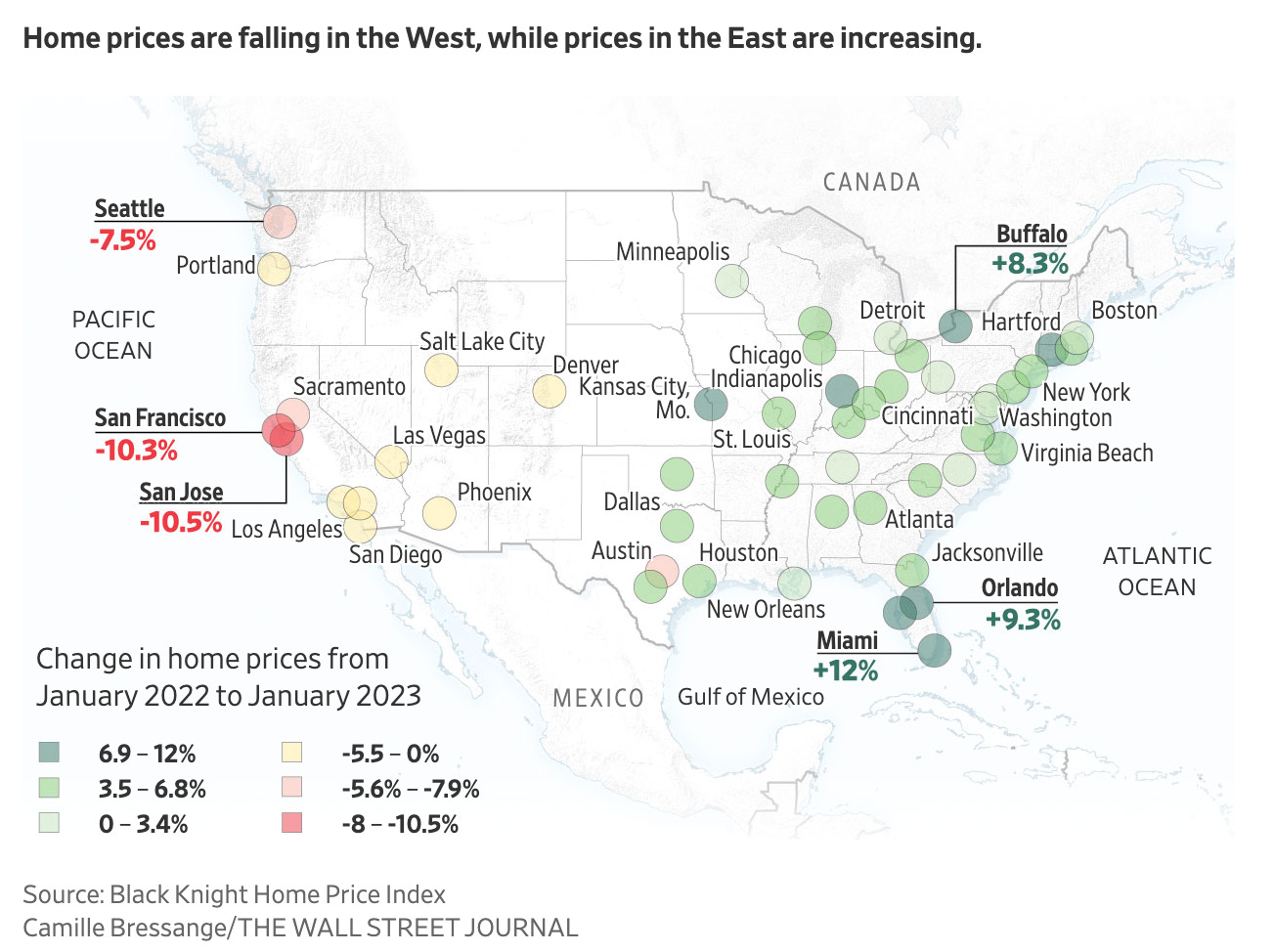

Real estate on the West Coast have experienced significant price increases since the 1990s, mainly driven by the rapid expansion of the technology sector. However, as the tech sector enters recession, cities such as San Jose and San Francisco have seen home prices drop by over 10% in January compared to the previous year, while Seattle experienced a 7.5% decrease.

On the other hand, in the Eastern half of the United States, states like Florida continue to draw in businesses and create jobs. Orlando's home prices increased by 9.3%, while Miami saw a 12% rise—the highest among the top 50 largest metropolitan areas. This growth can largely be attributed to friendlier business laws, the influx of financial companies that relocated to Miami in 2021 and 2022, and the ongoing arrival of their employees.

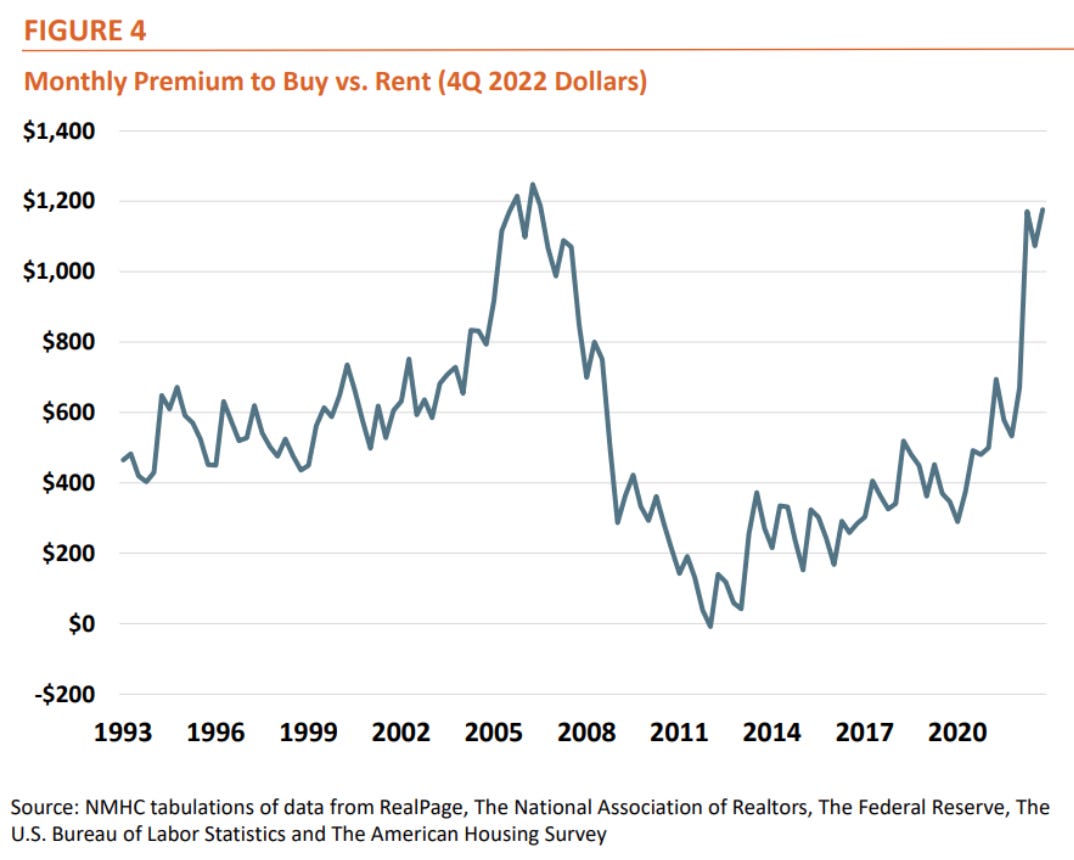

Overall, the housing market is still quite hot. According to the National Multifamily Housing Council, the monthly payment for a newly purchased home — assuming a 10% down payment and a 30-year fixed rate mortgage — was $1,176 more than renting an apartment at the end 2022.

The cost of homeownership has surged 71% over the past three years, or an average of about 20% per year, compared to average annual rent growth of 6.3% over the same period. The spread between buying and renting is now the largest since the third quarter of 2006.

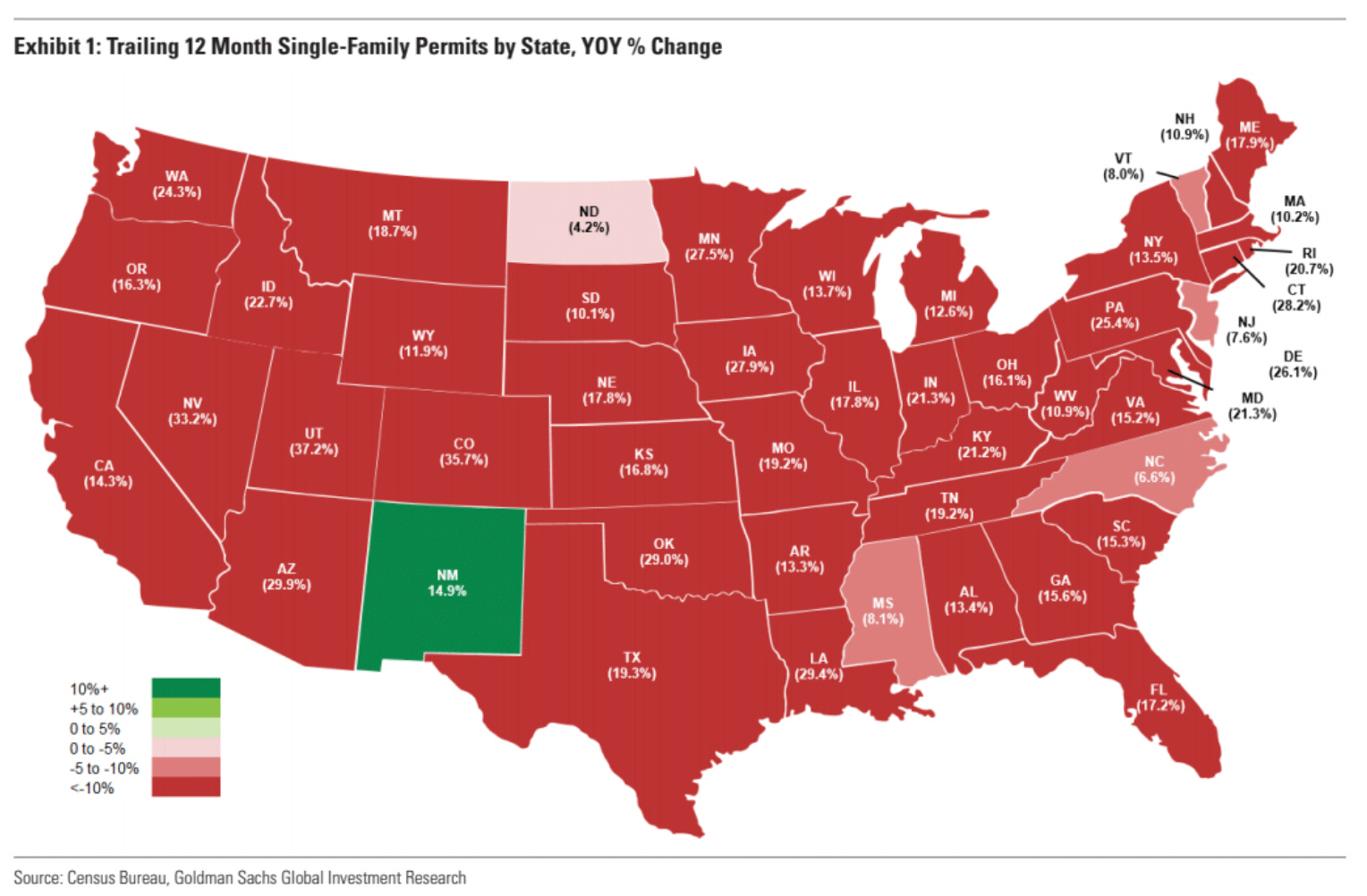

Increasing costs are largely due to a lack of housing supply of all types. Freddie Mac estimates that the U.S. is short by 3.8 million units while a another study found that there was a shortage of 600,000 apartments.

Even though mortgage rates are high and building activity has slowed down dramatically (see chart below0, there’s a structural demand for more houses.

https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/lossshare/index.html

https://www.cnbc.com/2023/03/27/heres-why-the-us-had-to-sweeten-terms-to-get-the-svb-sale-done.html

https://www.wsj.com/articles/where-financial-risk-lies-in-12-charts-792bca35?mod=hp_lead_pos6

https://www.wsj.com/articles/home-prices-housing-market-trends-east-west-83c9eb56?mod=hp_lead_pos7

https://www.nmhc.org/research-insight/research-notes/2023/putting-rent-increases-into-perspective/

https://www.freddiemac.com/research/insight/20210507-housing-supply

https://www.nmhc.org/research-insight/research-report/us-apartment-demand-through-2035/