SVB Fallout Blows Up Rate Projections and More...

SVB Fallout Blows Up Rate Projections and More...

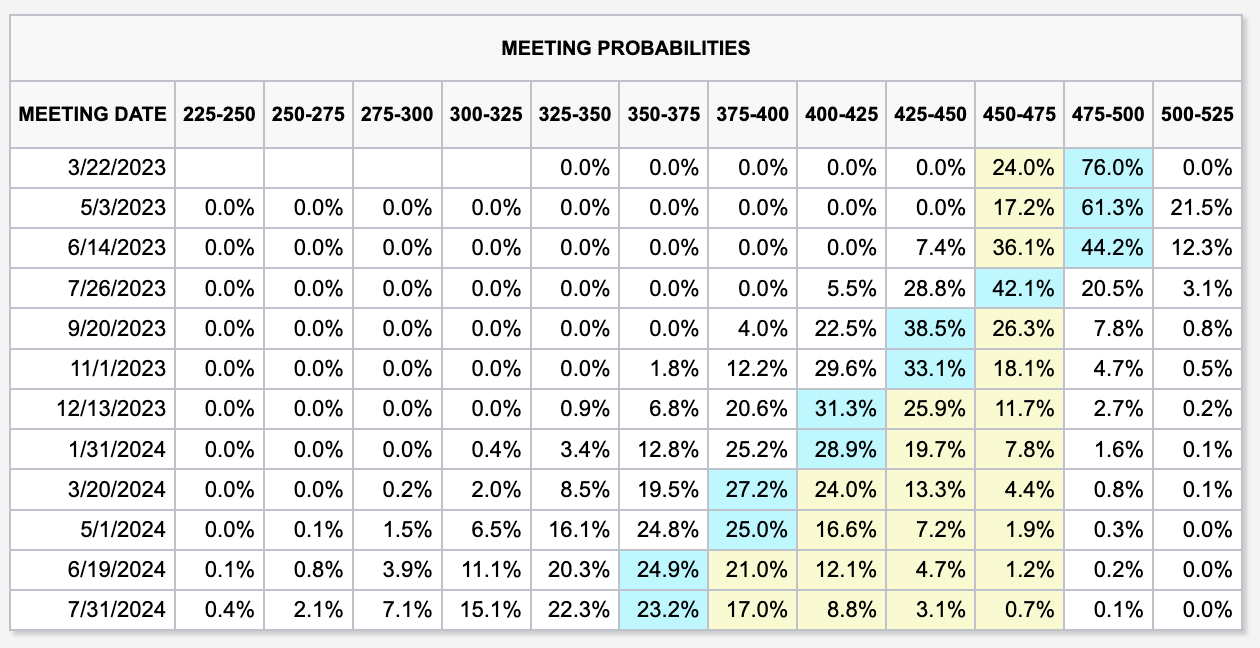

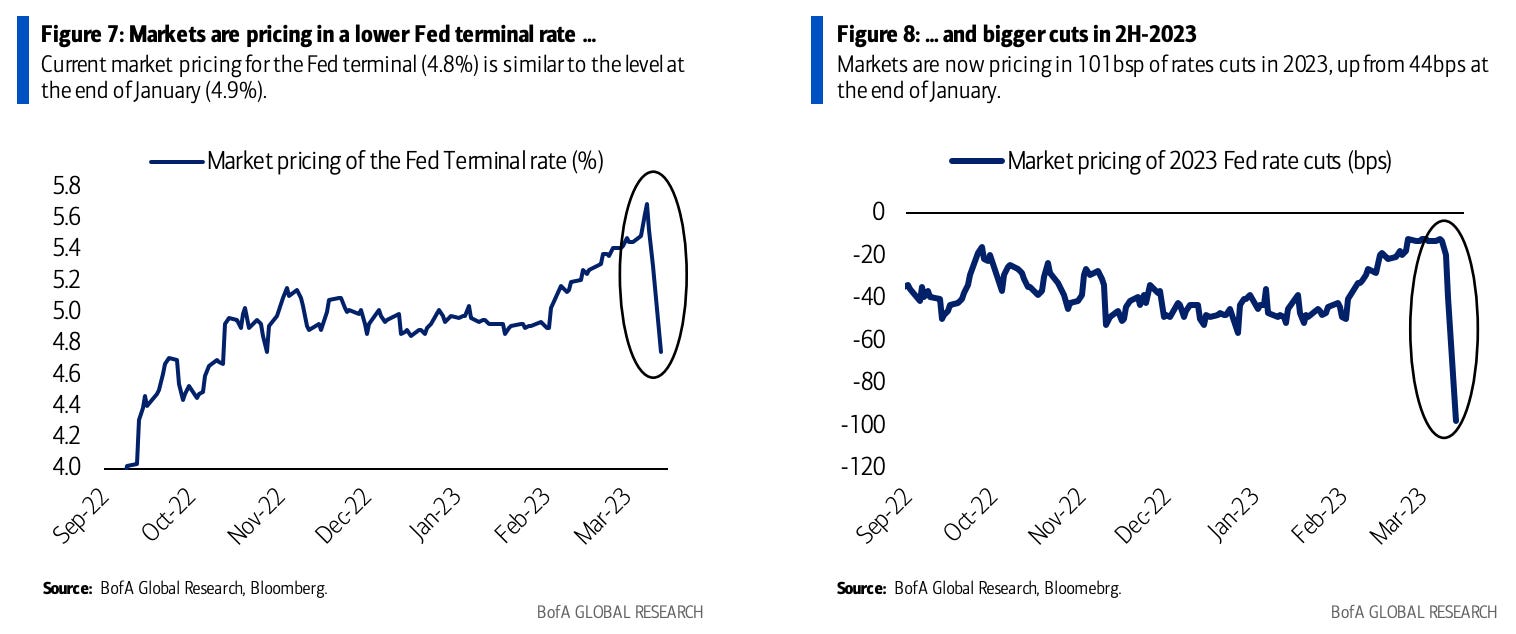

The market is now pricing a 5% terminal rate (implying 25 bps in March) and rate cuts as early as July. Just last week, after JPow testified in front of the Senate, the market was pricing a ~5.7% terminal rate…

And global financial stocks have lost $465bn in market value over the past two days as investors cut exposure to lenders everywhere…

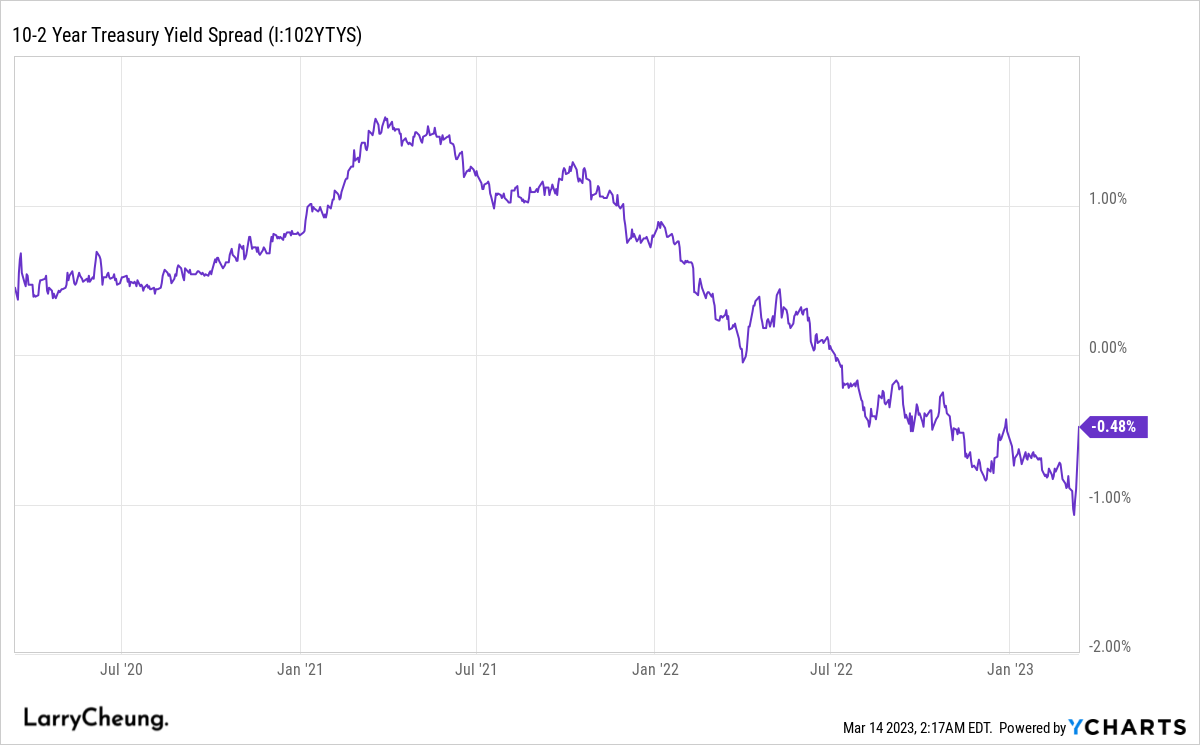

In addition, the rally in US short-dated debt meant a dramatic re-steepening in the yield curve, widely regarded as signaling a recession is imminent. The spread between US two- and 10-year yields is still inverted, but it jumped by 48 basis points on Monday, the most since January 2001, just two months before the official start of a recession that lasted through November of that year.

Another market indicator that caught my eye today was FRA-OIS spreads. A brief explainer of FRA and OIS…

Forward Rate Agreements (FRA) are contracts where two parties exchange at a fixed interest rate swap for a certain period. The interest rates usually refer to LIBOR.

Overnight Index Swap (OIS) are contracts where overnight interest rates swap for fixed interest rates, referring to US fed funds rates.

FRA represents the interest rates demanded by banks, while OIS reflects the overnight risk-free rate.

The spread between FRA and OIS represents the trends of borrowing costs and surges when the market demands higher risk premiums. FRA-OIS spreads are seen as a proxy for the banking sector and a measure of how expensive or cheap it will be for banks to borrow in the future, relative to the risk-free rate.

Yesterday, the FRA-OIS spread blew out to levels not seen since the peak of Covid, and pre-Lehman before that. In short, bank liquidity is drying up at a record pace.

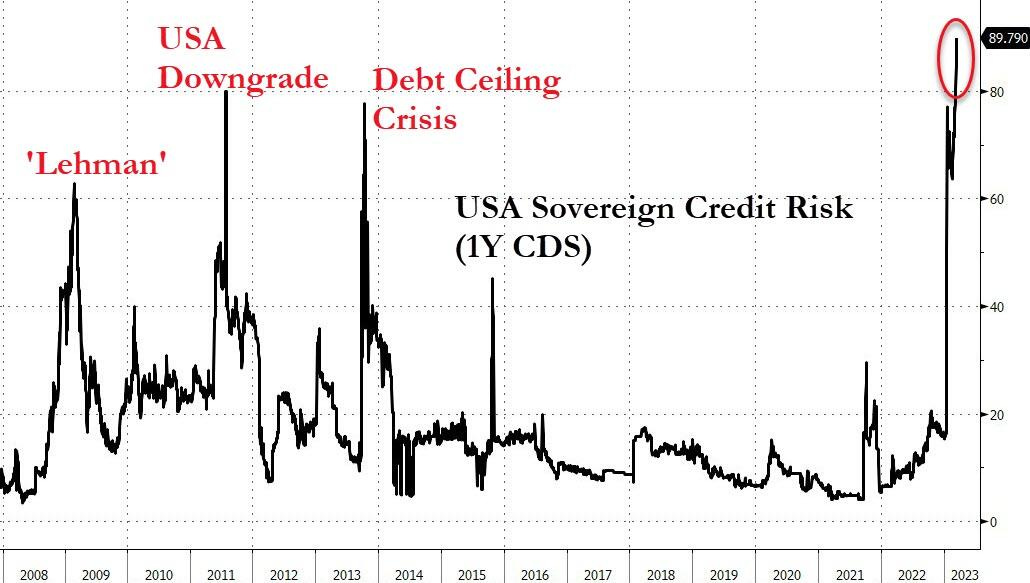

Yesterday also saw the US sovereign 1Y CDS spreads reach a record high. Yes. A record high.

Since my last post on SVB, which you can find below, a lot has transpired…

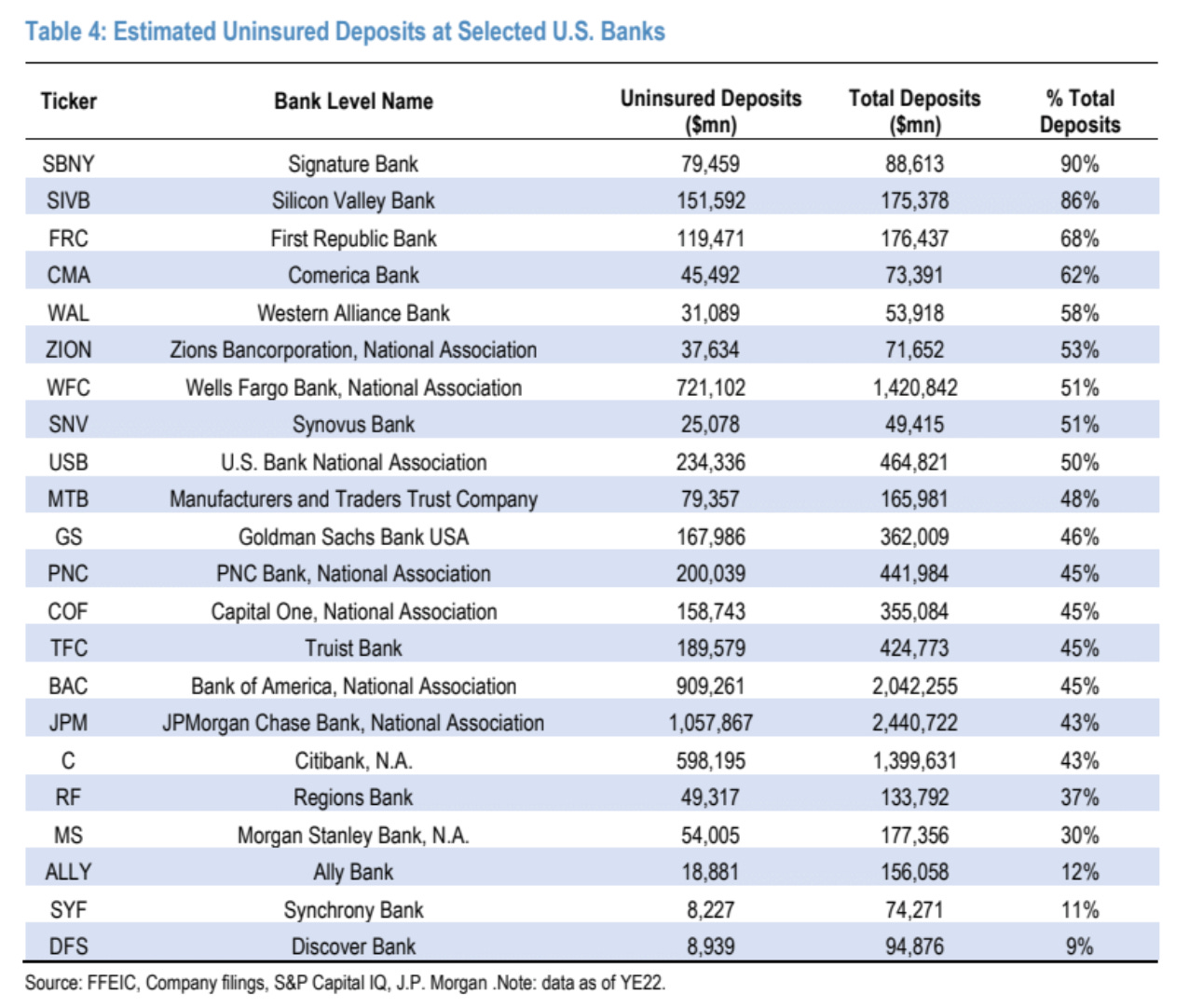

In a joint statement, the Treasury, Federal Reserve, and the FDIC announced that it would protect all depositors of SVB. In addition, Signature Bank of New York would also see its depositors made whole. Much like SVB, with clients made up almost entirely of businesses, Signature had a deposit base that was mostly uninsured (~90% of deposits). This may have attracted the attention of regulators looking into banks with large uninsured deposits.

The statement made it very clear that “shareholders and certain unsecured debtholders” would not be protected and senior management would be fired.

The Fed also announced that it would provide additional funding for eligible banks through a new facility called the Bank Term Funding Program (BTFP). The fund will offer loans up to one year in length while holding US Treasuries, agency debt, and mortgage-backed securities as collateral.

Here’s where it gets interesting. The collateral will be valued at par. Remember all those unrealized losses that the banks were holding? Say you buy bonds for $100 and it’s now worth $75. You can now go to the Fed and borrow $100 against that $80 while posting a collateral of $100 in the eyes of the Fed. Is money even real? lol

In its announcement, the Fed said that this facility will be “an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell securities in times of stress”.

There was also some pretty interesting news coming out of the Federal Home Loan Banks (FHLB), which is a system of 11 regional banks that act as a backstop used by banks for short-term funding. Yesterday, the FHLB raised $88.7bn via short-term notes. This stoked expectations that many banks will need to tap the FHLB for funds and that this was the FHLB getting ready… As Academy Securities described it, “the offering suggests that there is robust demand for financing as institutions seek to quickly raise dollar funding to replace outgoing deposits”.

As you can expect, many Wall Street firms had much to say about the ramifications of these actions, the state of the banking sector (note the inherent bias), and what could come next for the market and economy…

Deutsche Bank…

“A systemic financial event is not a necessary condition for recessionary dynamics. Competition for deposits is likely to become irreversibly more intense in the US banking system going forward, leading to an upward drift in the bank-based cost of financing and an extra layer of tightening hitting the real economy.”

Nomura…

Calls for 25 bps CUT in March.

“The sensitivity of individual depositors to deposit rates might have increased due to the FDIC’s announcement of making all Silicon Valley Banks’ depositors whole. We could see a significant outflow from commercial banks, which may compel banks to liquidate their loan portfolios unless banks raise their deposit rates substantially.”

“If the Fed keeps the policy rate “higher for longer”, banks would be averse to liquidating securities holdings for which selling would realize losses in securities any time soon.”

“The fact that other banks are facing a serious bank run risk suggests an increased risk of over-tightening by the Fed, which also supports a rate cut in the near term. As we argued, the cumulative rate hikes are disproportionately reducing the supply of credit through bank loans relative to financial market conditions.”

Barclays…

“We emphasize “pause” because we believe that the turmoil is likely to be contained in the coming weeks, especially following the backstops implemented over the weekend. We continue to believe that the Fed will see additional hikes as the baseline scenario, which it would carefully condition on an assumption that markets settle and that credit continues to flow from regional banks.”

Goldman Sachs…

In light of recent stress in the banking system, we no longer expect the FOMC to deliver a rate hike at its March 22 meeting with considerable uncertainty about the path beyond March

We would be surprised if, just one week after going to great lengths to support financial stability, policymakers risked undermining their efforts by raising interest rates again.

It is possible that market-based measures of financial conditions could ease, though this might be offset by tightening in bank lending standards. So far the net move in our financial conditions index has been limited, but it is possible that the combination of the recent policy announcements and a Fed pause could cause equity prices to recover while interest rates remain lower. However, a fallback in lending by smaller banks could have an offsetting or even larger negative impact on the economy.

Bank of America…

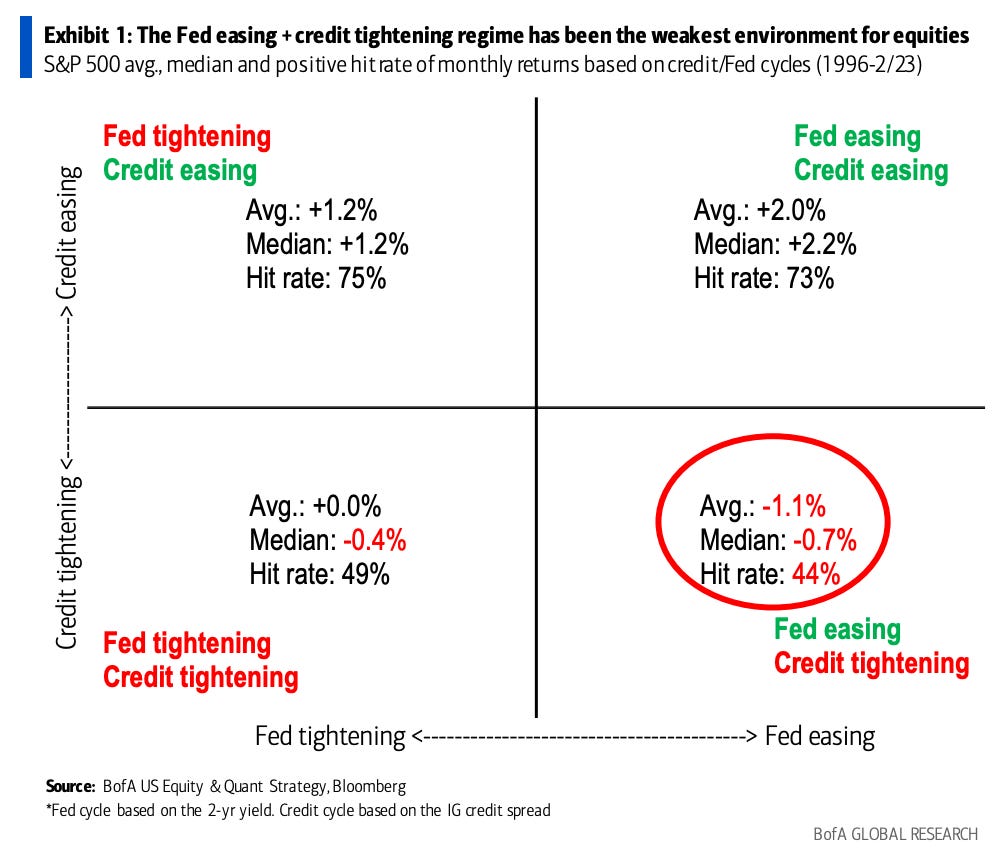

“The rates market has done an about-face and is now pricing in two rate cuts by year-end (vs. three hikes just a week ago). Before equity bulls start to celebrate a Fed pivot, remember that easy Fed policy and tightening credit conditions have been the worst phase for stocks.”

“Of the four scenarios based on easy vs tight Fed vs credit, Fed easing (falling 2-yr yield) and credit conditions tightening (widening credit spread) is the regime typically seen in a recession. Since last Wednesday, the 2-yr yield fell by ~100bps and the credit spread rose by ~20bps. Historically, Fed easing and credit tightening has resulted in losses for the S&P 500, the only regime of the four during which we have seen losses on average.”

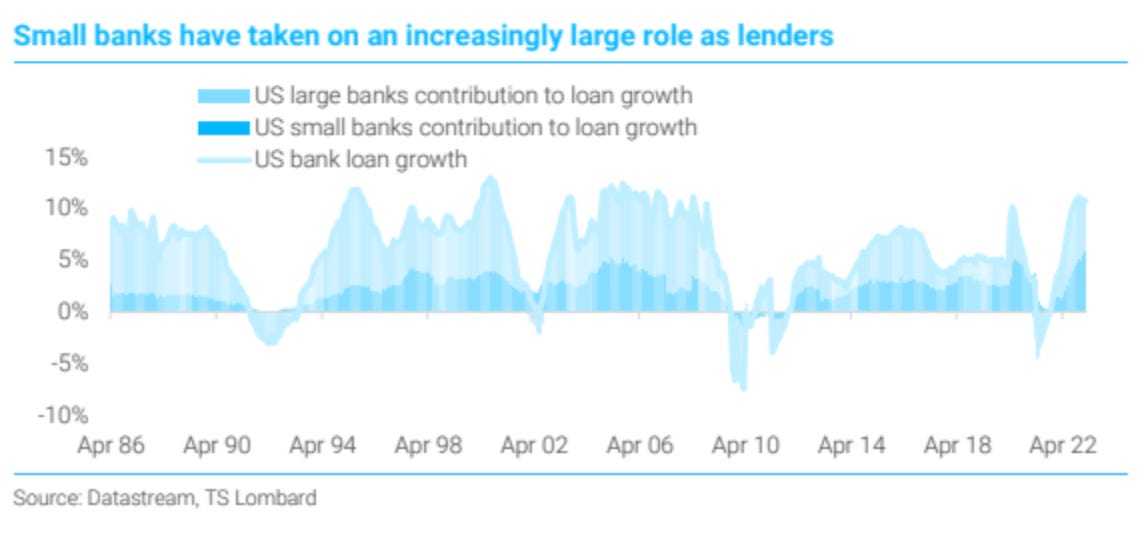

TS Lombard…

Small banks are close to critical balance sheet ratios and are now even more likely to pull back on lending. They have an increasingly large role as lenders. After GFC, big banks deleveraged and pulled back on lending.

JP Morgan…

For large banks, deposit funding is much more diversified with the largest proportion from the retail segment. Retail deposits accounted for 57% of total average deposits in 4Q. Corporate deposits were next at 34% and wealth management at 10%.

Smaller regional banks are generally much more heavily skewed towards commercial deposits and couple to wealth management deposits, which are more prone to rapid withdrawals.

I will continue to follow this topic very closely and give more updates as things develop. Thank you for the support!

Sources

Research from Bank of America, Nomura, Barclays, Goldman Sachs, Morgan Stanley, JP Morgan, TS Lombard, and TD Ameritrade

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

https://www.zerohedge.com/markets/usa-sovereign-credit-risk-hits-record-high

https://www.zerohedge.com/markets/nomura-first-bank-call-rate-cut-next-fomc-meeting-end-qt

👍🏻🙌🏻