JPow's Testimony and Market Complacency

JPow's Testimony and Market Complacency

Jerome Powell gave remarks yesterday in front of the Senate Committee on Banking, Housing, and Urban Affairs. Most of his comments were in line with previous Fed communications, which took note of strong momentum in labor markets, less disinflation than previously indicated, and the Fed’s willingness to do more in terms of rate hikes to bring inflation to the 2.0% target.

It’s notable that in February’s press conference, JPow mentioned ‘disinflation’ 13 times, but made no mention of tight labor markets and avoided saying that a return to 2% inflation would require softness in the labor market. However, in yesterday’s remarks, JPow noted that “Restoring price stability [would likely require] some softening in labor market conditions”.

The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes. - Jerome Powell, 3/7/23

Powell also noted the importance of “two or three” data releases to analyze before the time of the March FOMC meeting, stating that “Those are going to be very important in the assessment we have of this relatively recent data”. My guess is that he is referring to the February payroll numbers this Friday, and a CPI and retail sales report next week.

The market sure took notice of this hawkish tone. The odds of a 50 bps hike at the March FOMC meeting before JPow’s remarks were just 31%. At the time of writing, the odds are now 73.5%.

Meanwhile, the Fed Pivot narrative is pretty much dead at this point. The market’s expectation for the terminal rate is now at 5.65%. This means another ~105 bps of rate hikes!

Meanwhile, there were also major moves in the Treasury market…

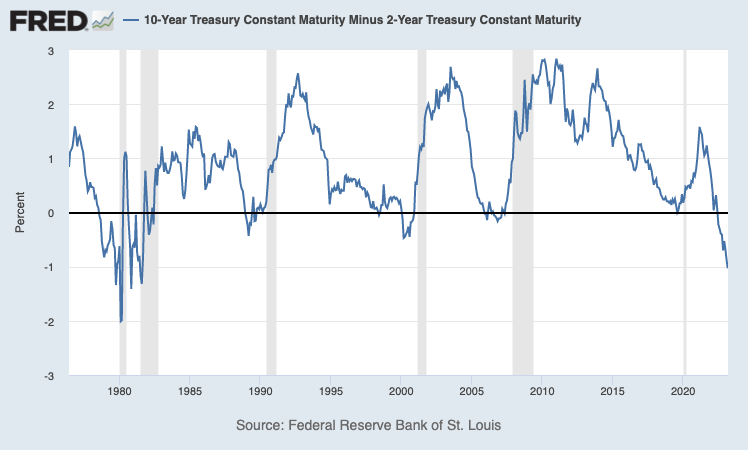

The 2-year/10-year spread broke below -100 bps for the first time since Sept. 1981…

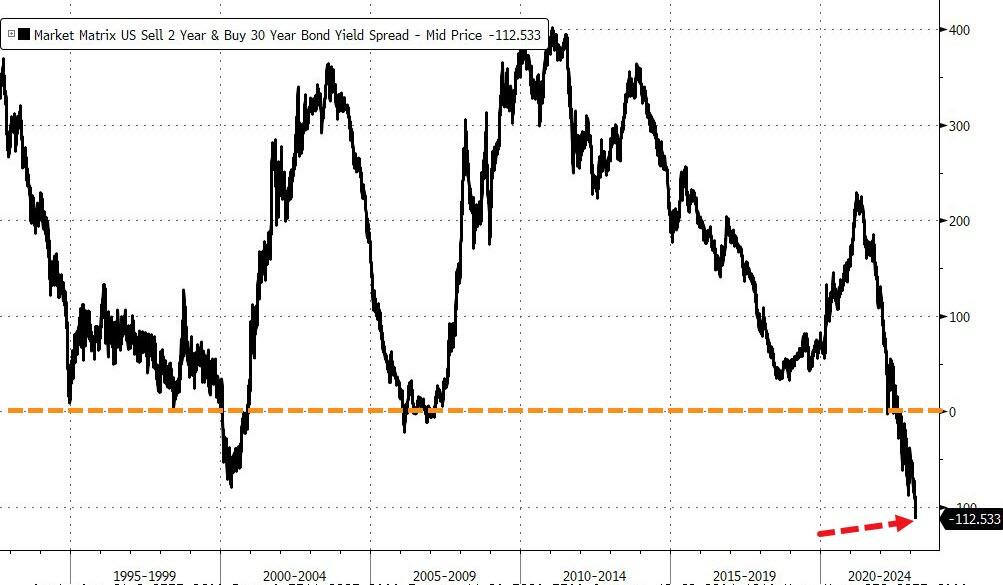

While the 2-year/30-year spread continued its record collapse.

So what’s next?

Per JPM, “The Fed will heavily depend on near-term data for upcoming rates decisions. With January’s macro data mostly printing on the hawkish side, NFP (Non-Farm Payrolls) Friday and CPI next Tuesday are the most critical catalysts for Fed’s decision between 25bp and 50bp. Keep in mind that the Fed will start its blackout period this Saturday so CPI will be released during the blackout period, so data itself will be more impactful in absence of guidance from Fed speeches."

If we get hot February data, we may get yet another painful u-turn by the Fed which has already essentially abandoned forward guidance.

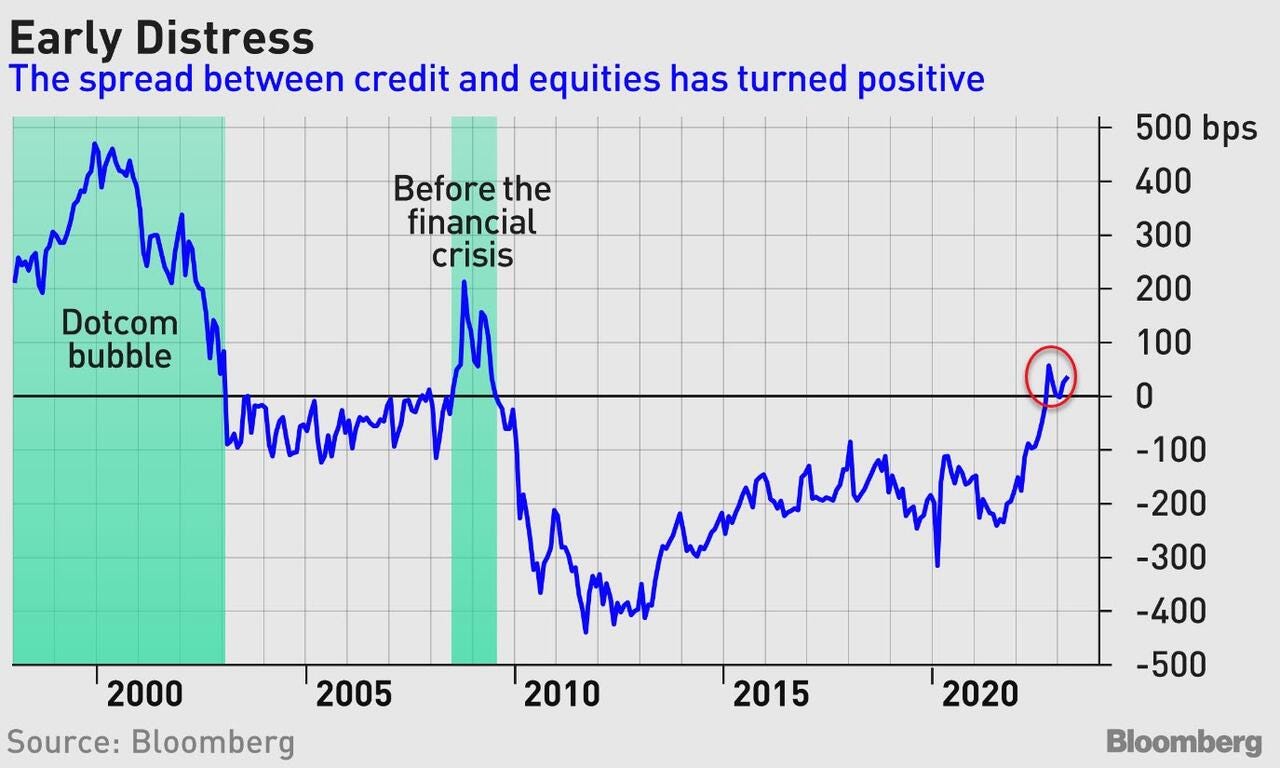

The credit and equity markets are already displaying a cautionary message about the future of global financial assets and the economy. The spread between BBB-rated dollar-denominated corporate debt and the earnings available on the S&P 500 has turned positive, indicating that investors may be underestimating the risks associated with equities.

Additionally, the Nasdaq 100 has seen significant gains this year, concurrent with a significant outflow from junk bonds, indicating a possible flow of funds from speculative-grade credit to higher-risk tech stocks.

The current earnings yield on stocks is equal to the terminal Fed rate being priced in by the markets. The markets apparently believe that stocks don’t require any risk premium over Treasuries. Complacency on another level.

A study of the S&P 500's duration has shown that the index could decline by about 7% for every 100-basis point increase in the Fed funds rate, highlighting the potential for stocks to fall further.

As Jerome Powell described today, it’s “hard to make a case that we have over-tightened. You are a long way from anything that looks like a recession”.

Buckle up.