Implications of Silicon Valley Bank's Collapse

Implications of Silicon Valley Bank's Collapse

By now, you’ve probably heard about Silicon Valley Bank and its recent collapse and subsequent takeover by the FDIC.

In this article, I’ll go over how we got here, what happened over the past few days, and what it may mean for other banks. There’s a TON of information circling online, so I hope this will give you a through explanation of the situation.

Silicon Valley Bank (SVB) was the go-to bank for VC funds and startups. As the 18th largest bank in the US, it did business with nearly half of all US venture capital-backed startups and 44% of US venture-backed tech and healthcare companies that went public last year.

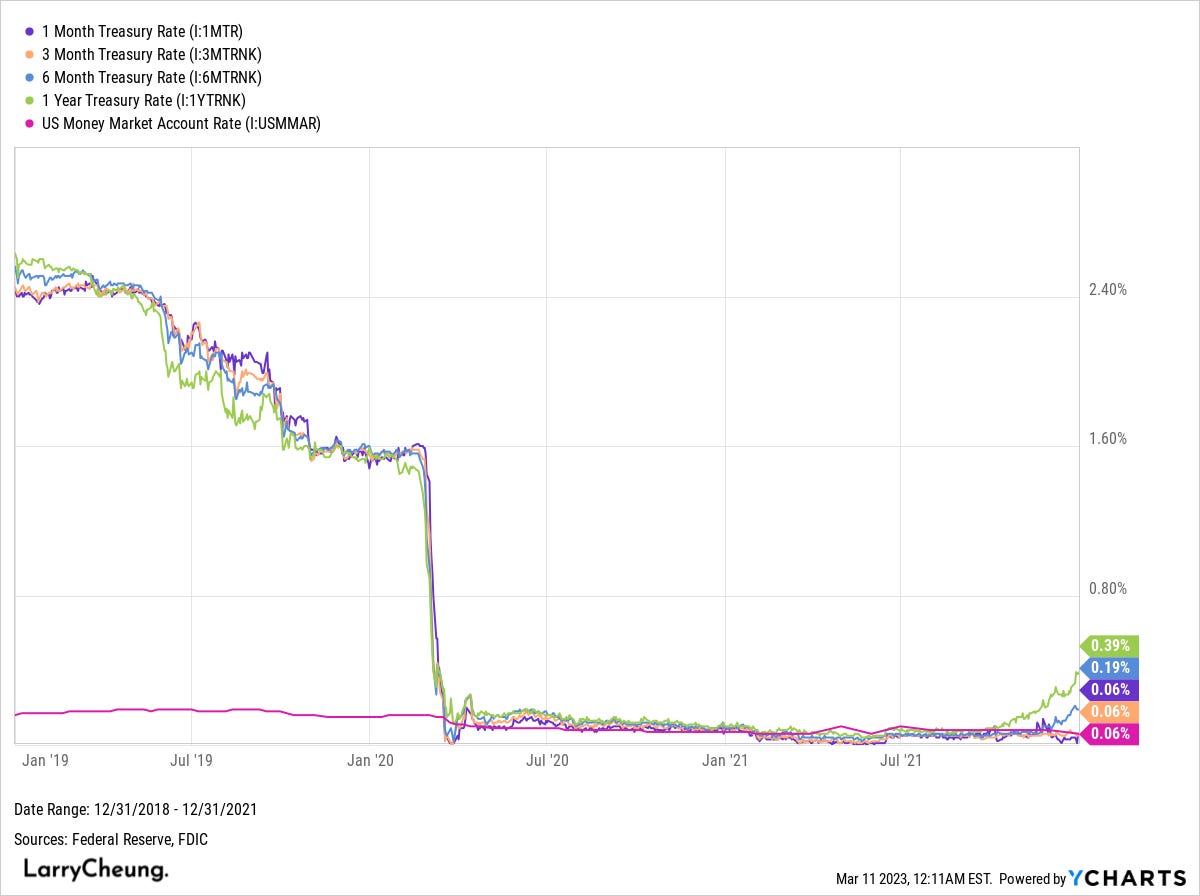

When the pandemic hit, the Fed slashed rates to 0 (Zero Interest Rate Policy, ZIRP). And because of ZIRP, asset prices skyrocketed. As VC investment increased, SVB’s deposits tripled.

With such a massive influx in deposits, SVB had to put the money to work somehow. But at the time, short-term Treasury bills and money market funds paid nothing. In addition, everyone was telling us that inflation was no worry and that the Fed wouldn’t need to raise rates.

To be clear, I am not defending SVB’s subsequent actions. Just providing the necessary context.

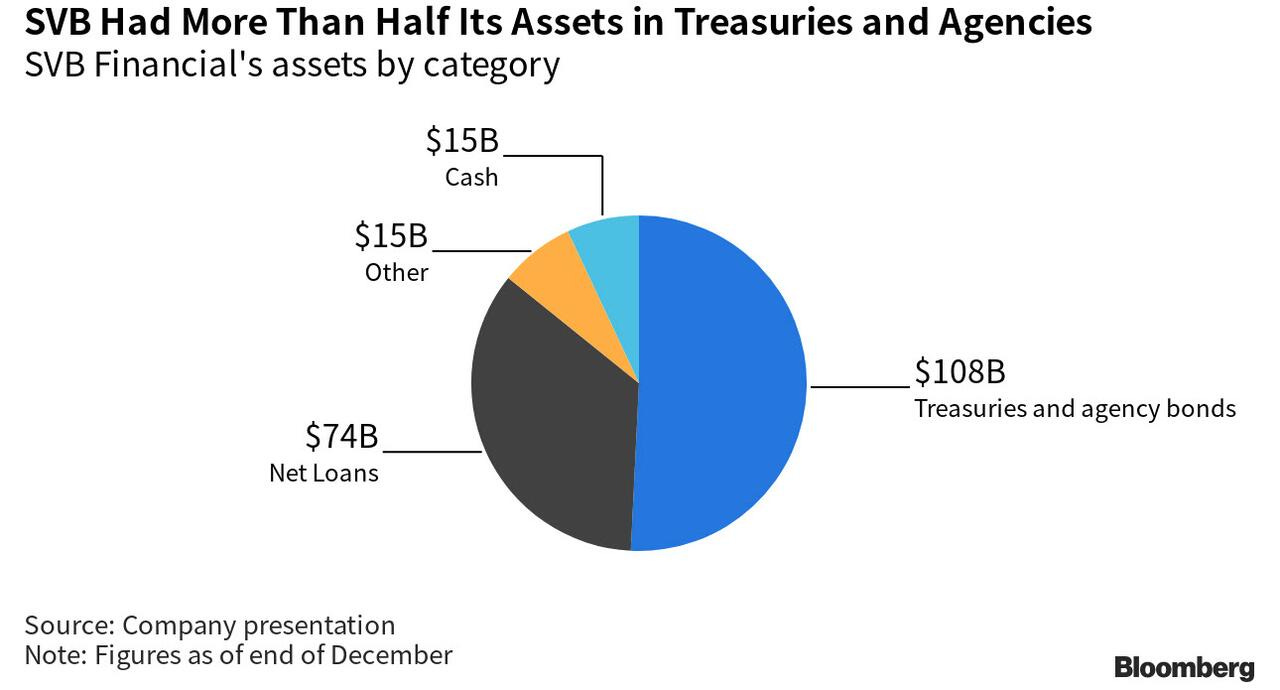

So SVB decided to purchase >$80 billion in mortgage-backed securities, 97% of which had a duration of 10+ years, at a weighted avg. yield of 1.56%. Yikes.

Now SVB had an outsized portion of its assets in its investment portfolio. The largest percentage of any U.S. bank.

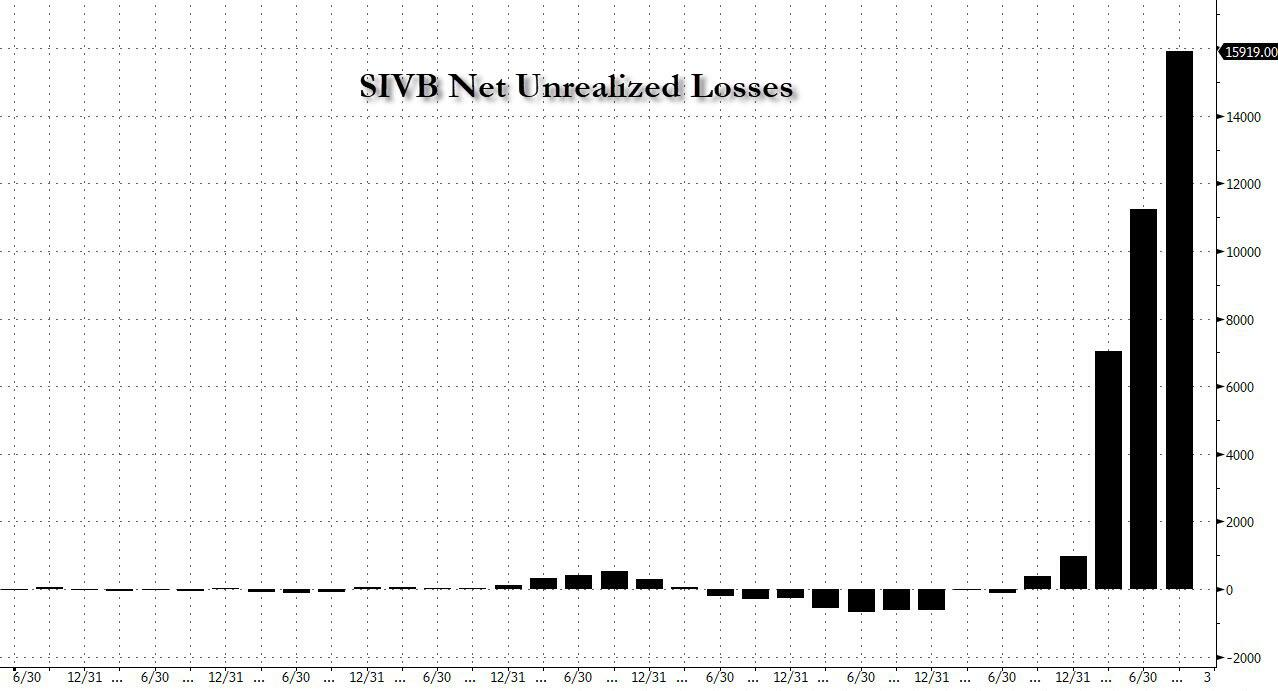

As inflation reached 40-year highs and the Fed raised rates, bond prices started to collapse. Note that there is an inverse correlation between interest rates and bond prices.

This led to SVB suffering massive unrealized losses on its bond portfolio.

At the same time, VC funding started to dry up…

VC investing is one of the riskiest forms of investing as many investments go straight to 0. It’s almost like playing the lottery. When the cost of playing the lottery is 0, you’ll play all day. But when rates go up, the lottery costs go up. So you’ll probably play less often.

Even though VC funding dried up, SVB’s clients (mainly startups), were still burning cash at levels 2x higher than pre-2021.

We already know that SVB is a pretty unique bank as it primarily deals with startups. But it’s also unique because of its extreme sensitivity to interest rates.

Usually, banks can benefit from higher rates as it means higher interest income. But for SVB, higher rates mean 1) a lower value of SVB’s debt portfolio and 2) less supply of cheap deposits as VC funding declines.

In addition, while most banks have hedges that can offset interest rate risk, SVB had none. SVB had $5mn in interest rate swaps for a $120bn security portfolio, most of which are long-duration fixed-rate assets. Crazy.

At some point, the withdrawal velocity from customers got too fast for SVB to handle, and it had to sell some of its securities to pay them back. But remember, these securities were massively underwater. This is a scary cycle. You sell at a loss to pay back depositors… Depositors get spooked and withdraw even more, so you have to sell even more securities at losses.

This led to many notable VC firms advising their portfolio companies to withdraw from SVB, contributing to the massive bank run on March 9th. A whopping $42bn was withdrawn on March 9th, 25% of SVB’s deposits…

The contagion didn’t just end with just VCs and startups. Many publicly traded companies such as Roku and Roblox had cash in SVB. Roku had ~25% of its cash in SVB!

Circle’s USDC stablecoin reserves were also affected as it had 8% ($3.3bn) of its assets backing USDC in SVB. This led to USDC breaking its peg from the dollar, falling to as low as $0.87…

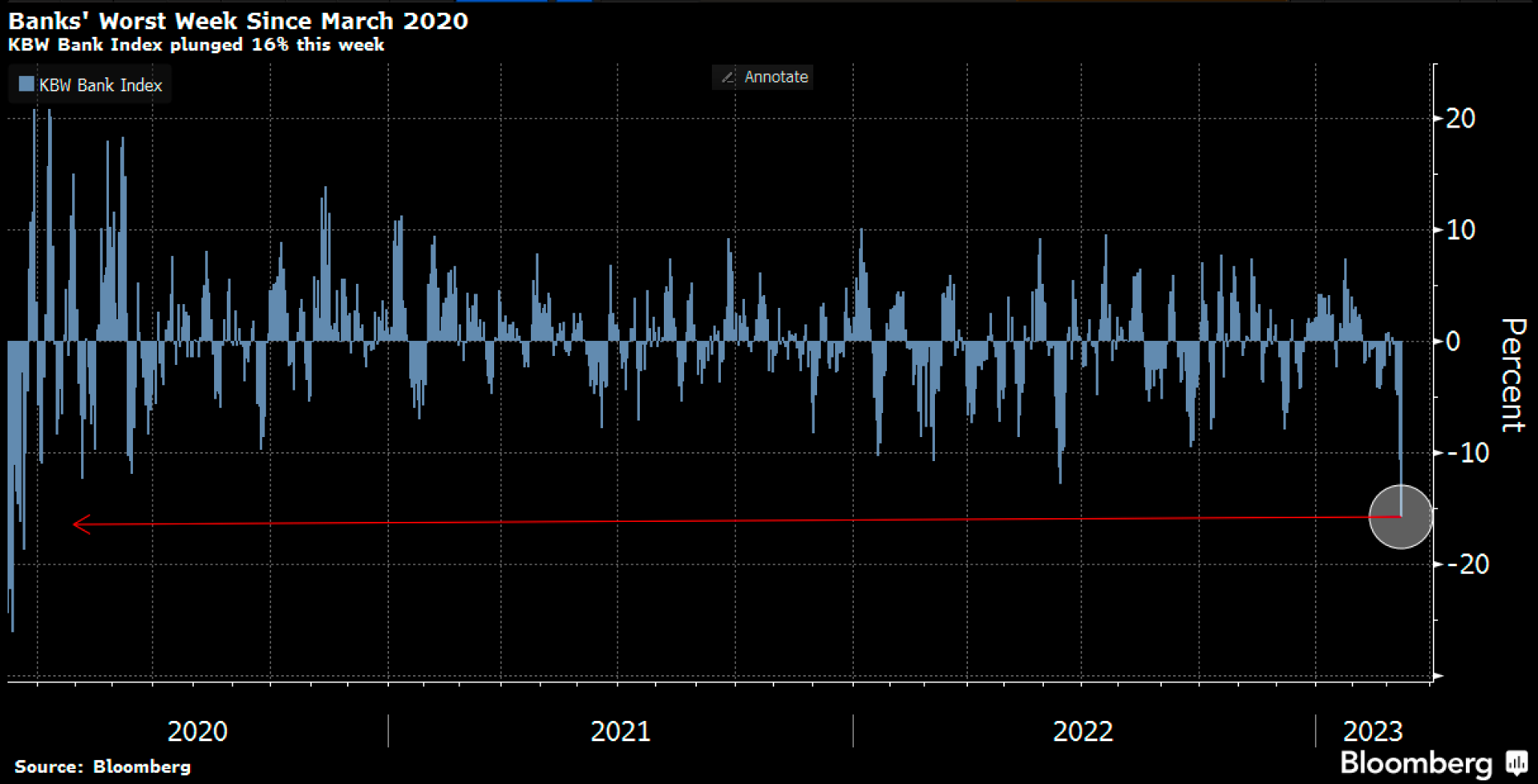

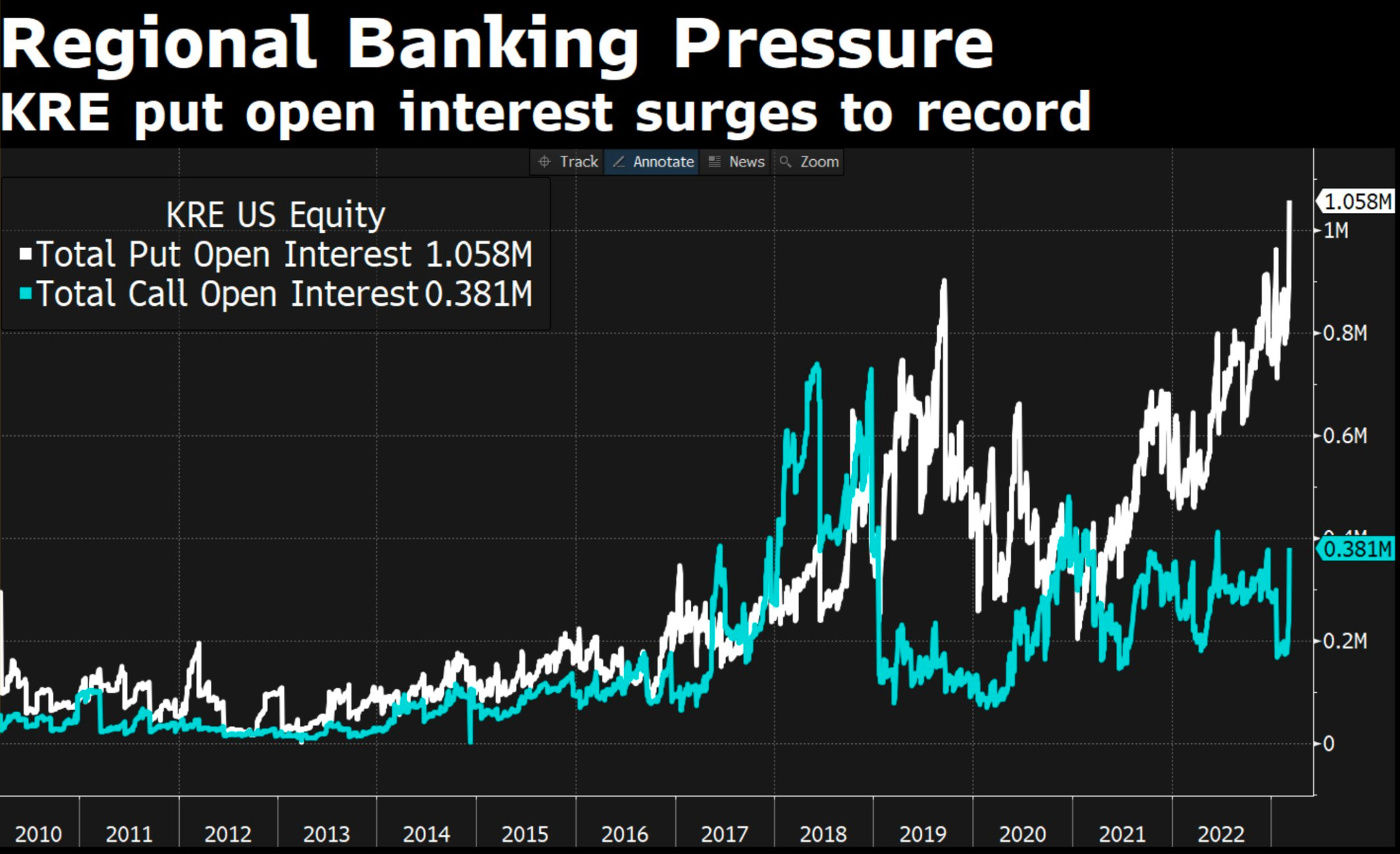

Troubles at SVB caused mass fear across the financial sector as bank stocks experienced one of their worst weeks in 3-years.

Most notably, CDS spreads for the big banks and the regional bank put open interest both skyrocketed.

So why is there massive fear?

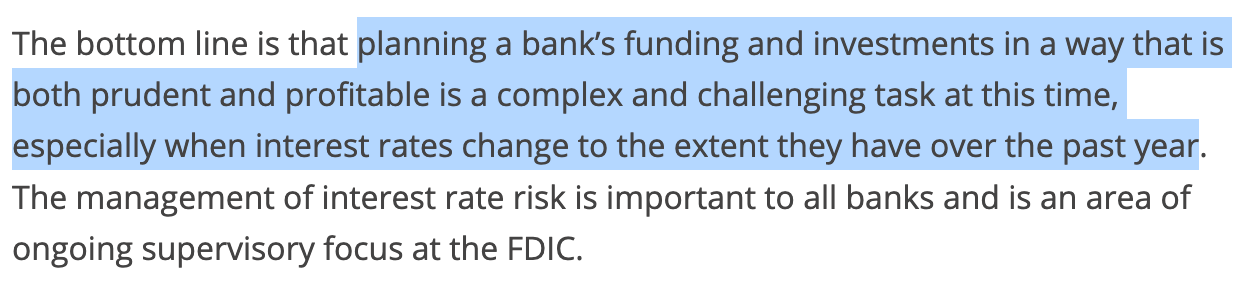

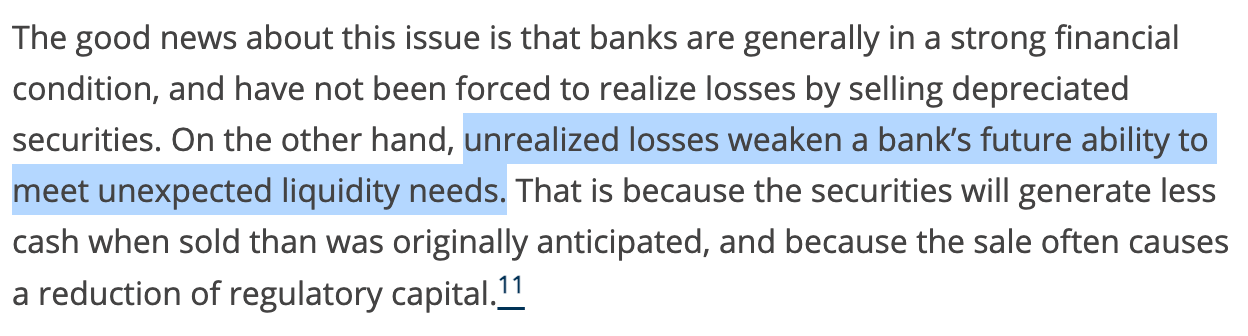

It has to do with the unrealized losses that many banks are holding onto and deposit outflows that haven’t been seen in decades. Just a few days before the collapse of SVB, the chair of the FDIC noted the challenges of running a bank when interest rates change to the extent they have and that these unrealized losses weaken the bank’s liquidity.

So what exactly is he talking about?

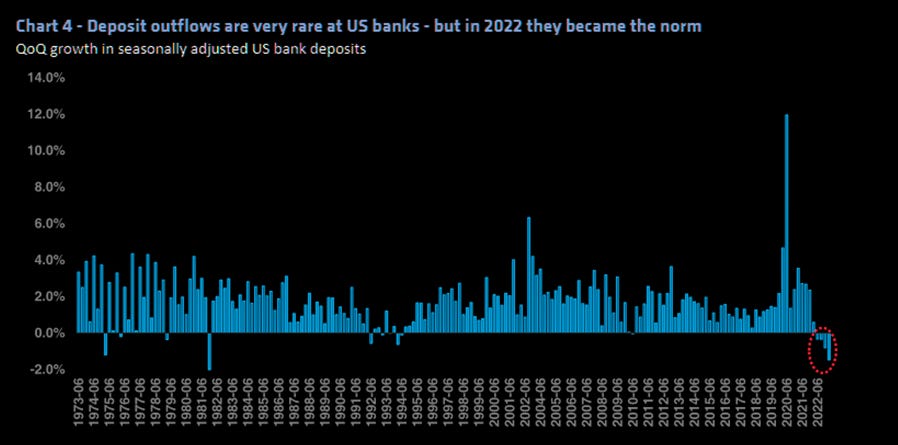

Deposits at banks have seen outflows over the past few quarters, which rarely happens. This is because rising rates cause depositors to spend down their balances to deal with rising costs elsewhere, or search for better places to put their cash. But for banks, the dwindling deposits mean they lose a low-cost source of funding.

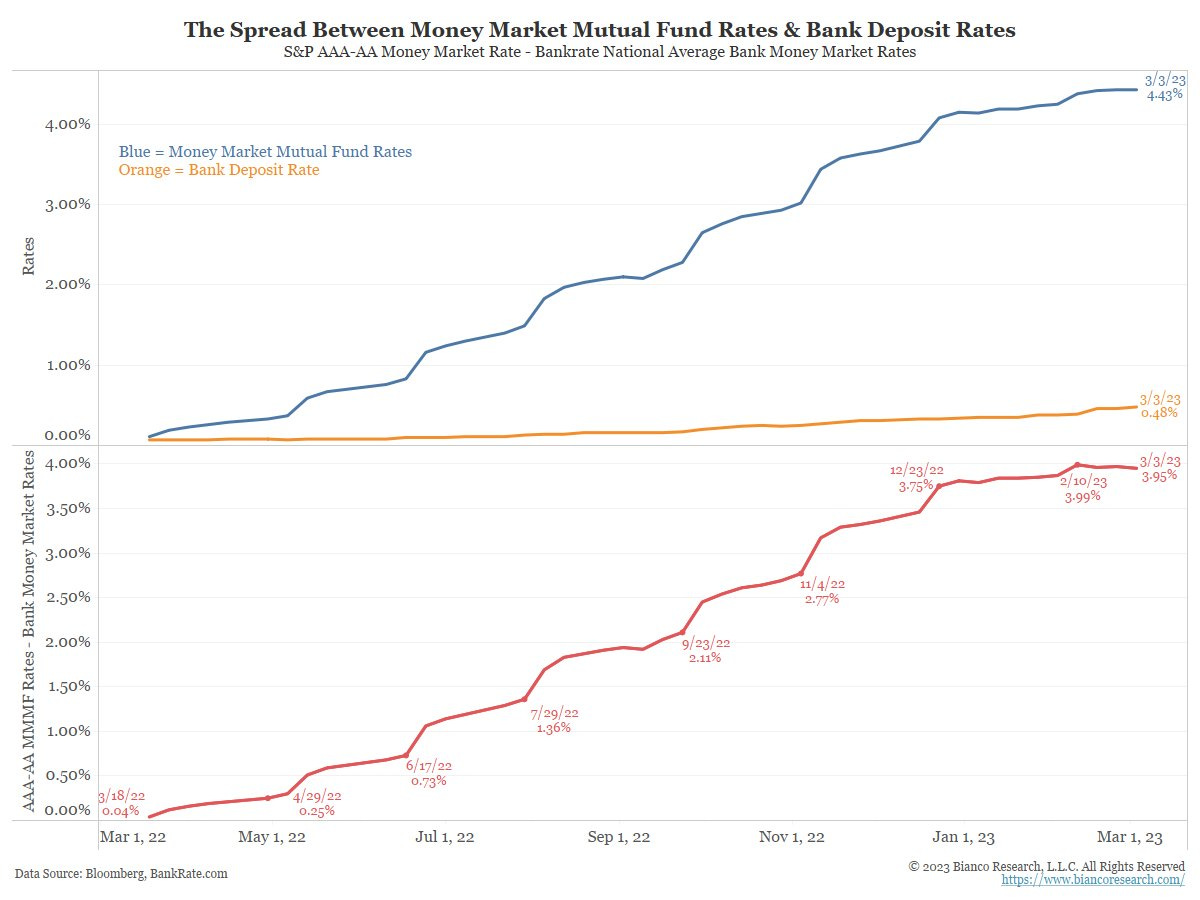

Over the past year, banks kept rates on checking/saving accounts extremely low compared to money market funds. The avg. yield on a MM fund reached as high as 4.43% recently, while bank rates remained at just 0.48%. The gap is almost 4%…

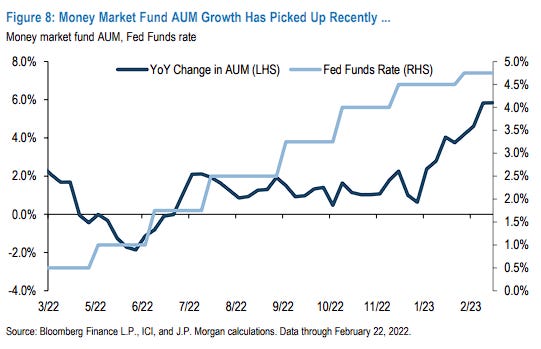

So as MM fund rates and Treasury yields increased, people moved money away from banks and into these ‘risk-free’ assets. After all, would you rather have your counterparty be a bank or the US Treasury?

As we discussed earlier, the record rate hikes over the past year have been devastating for bond returns. If banks can’t reliably use deposits as a source of funding, they’d have to sell securities on their balance sheet, which are generally Treasuries and other fixed-income assets. Note in the chart below that the big banks are sitting on massive unrealized losses at the moment.

However, it’s important to note that the big banks generally (hopefully) have strong risk management protocols and strict capital requirements, which can help hedge interest rate and duration risk.

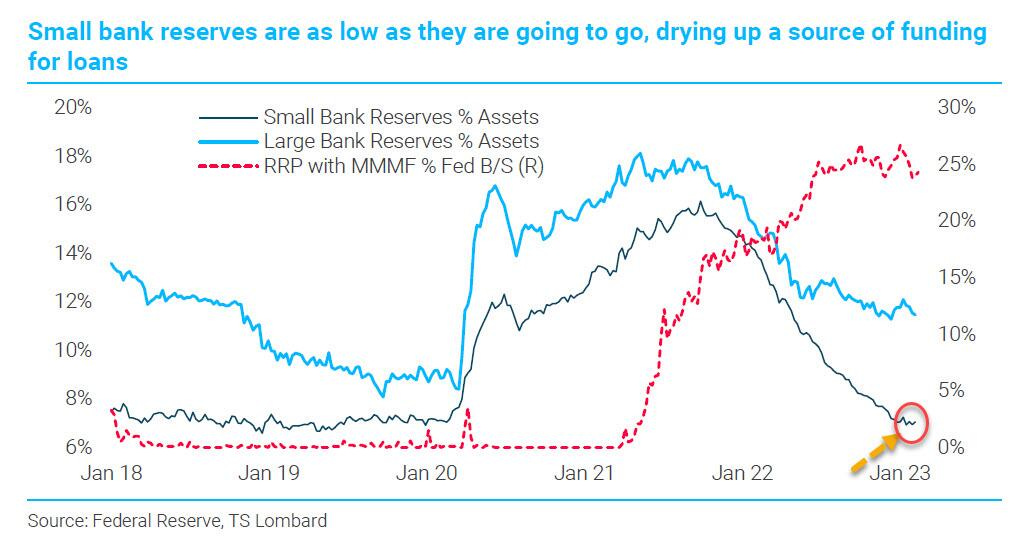

On the other hand, regional/small banks may have a harder time. Small banks are more aggressive in lending and borrowing short-term liabilities to fund themselves. In the charts below, we see that small bank lending is also far more concentrated in non-residential real estate than large banks and that small bank reserves as a % of assets have completely dried up.

At the end of the day, it’s important to remember that SVB is still quite a unique scenario.

Most banks have a diverse customer base. SVB did not.

Most banks can benefit from higher rates (higher NII). SVB did not.

Most banks have diversified assets. SVB had an outsized position in MBS and Treasuries.

Thanks for reading! I hope you found this insightful.

well done timothy :)

Well written Tim~