'Ghost' Job Listings and Employment Scams Soar, History Implies Rate Cut Could Come Sooner Than Later, Money Market Inflows Raise Recession Risk

'Ghost' Job Listings and Employment Scams Soar, History Implies Rate Cut Could Come Sooner Than Later, Money Market Inflows Raise Recession Risk

In past posts (see below), we’ve talked extensively about how the robust labor market may not be as hot as it seems. Even though there were 10.8 million job openings in January, many of these openings aren’t being filled. Some employers don’t even have the intention of hiring despite having ‘openings’.

A survey from Clarify Capital found that “despite 96% of employers claiming they’re actively trying to fill an open role quickly, 40% of employers don’t expect to fill their active job posts for 2-3 months. In fact, 1 in 10 managers reports having job openings posted for over 6 months.”

So why are employers still posting these jobs despite not having any intention of immediately hiring? “Employers post ‘ghost jobs’ for a variety of reasons. Around half of companies keep job postings open because they are always open to new people, but 43% aren’t actively trying to fill positions because they want to keep employees motivated or they want to give off the impression that the company is growing.”

In addition to these ghost jobs, employment scams are also on the rise. Per the WSJ, these schemes often involve “fictitious job listings, interviews with fake recruiters and sham onboarding processes to steal job seekers’ money or identities”.

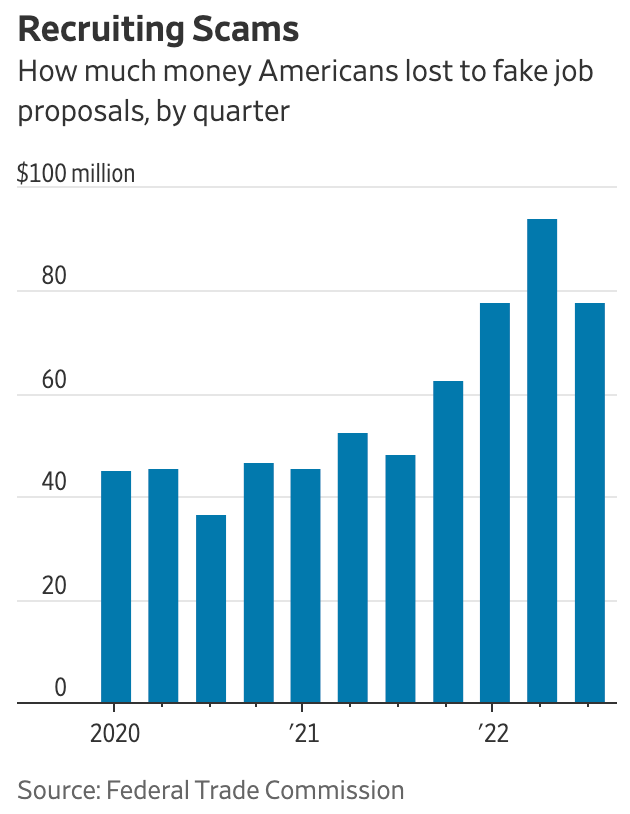

According to the FTC, the number of reported job scams tripled to 104,000 between 2019 and 2021. US workers lost more than $200 million from employment-related scams in 2021, up from $133 million in 2019. ‘Business and Job Opportunities’ is now the 5th most common fraud in the United States, with a median loss of $2,000.

You can read one of these sad stories here, in which a person was approached by someone claiming to be a recruiter for Coinbase. According to Linkedin, more than 21 million fake accounts were detected and removed between Jan 1st and June 30th. There was a 28% increase in fake accounts caught compared to the previous six-month period.

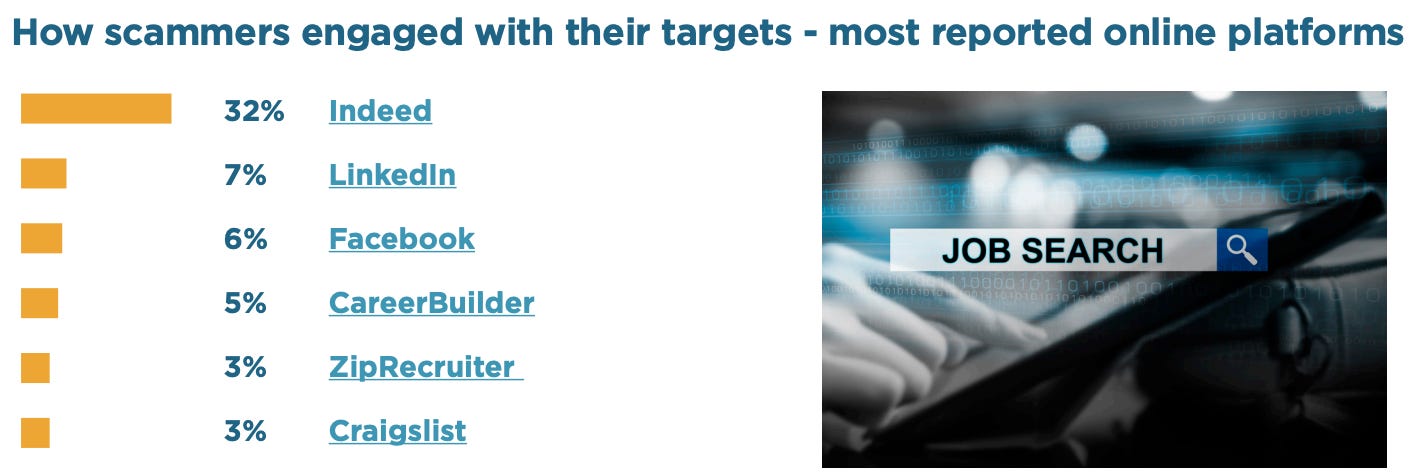

According to the BBB, 32% of fake job listings come from Indeed, while Linkedin accounts for 7% of fake listings.

Here are some resources that may help you identify fake jobs if you encounter a fishy opening:

https://www.linkedin.com/pulse/6-warning-signs-job-posting-fake-jt-o-donnell/

https://www.topresume.com/career-advice/job-scam-warning-signs

https://www.indeed.com/career-advice/finding-a-job/how-to-know-if-a-job-is-a-scam

As discussed previously, there is a large gap between where the Fed thinks the terminal rate lies and where the market is pricing the terminal rate.

The Fed (see first chart below) believes that the fed funds rate will peak at 5.00%-5.25% (implying one more 25 bps hike in 2023) and that there won’t be any rate cuts this year. On the other hand, the market (via fed fund futures) is pricing no more rate hikes AND 2 rate cuts this year.

Despite dovish market expectations, there’s an argument to be made that the labor market, the yield curve, and an ongoing banking crisis will force the Fed to cut rates even sooner than both the Fed and the market expect.

Let’s examine each.

Going back yet again to the labor market, almost 20% of states are seeing jobless claims rise more than 25% on an annual basis. Per Bloomberg, this is at a level that is often “preceded by a further rapid deterioration and a jump higher in the nationwide number, which has in most cases culminated in a recession”.

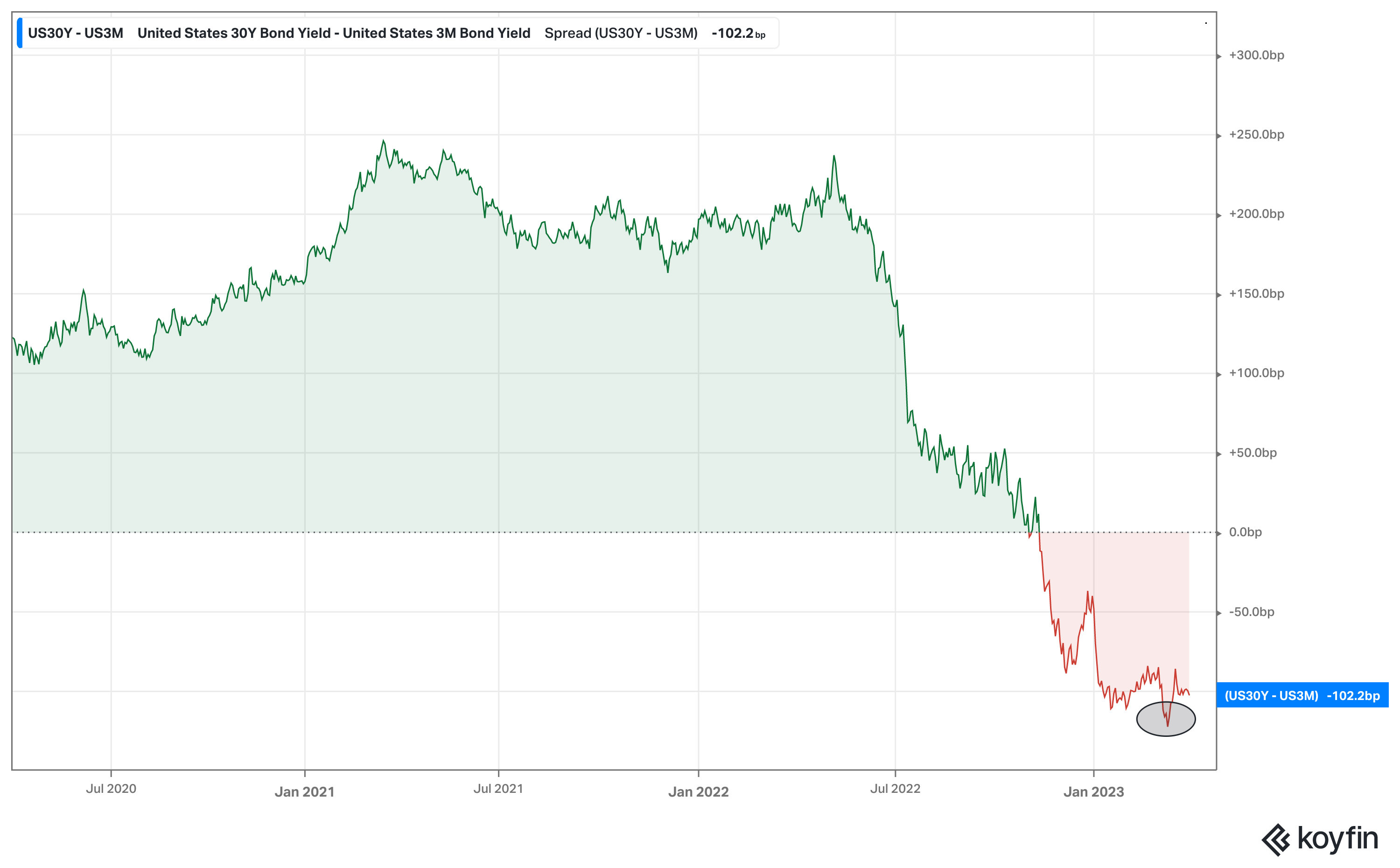

The Fed typically begins cutting rates 2-3 months before the recession starts and 6-8 weeks after the 3-month - 30-year spread begins to steepen.

As seen below, if the 3m-30y did indeed bottom on March 10th, then this implies a potential rate cut in late April - early May. Following this logic, if the Fed cuts rates in May, then this means the ‘official’ recession could start in July or August.

This is purely an extrapolation of historical trends so take this with a major grain of salt.

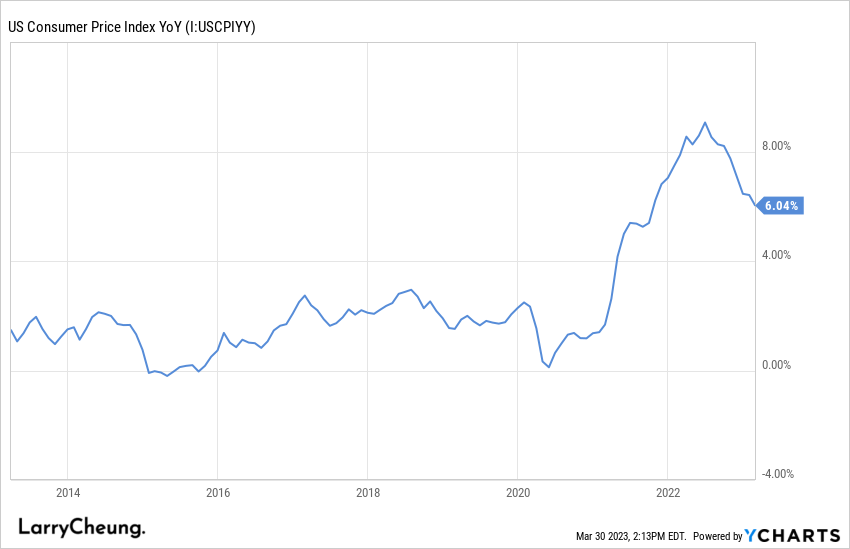

Moving on to inflation. Inflation is undoubtedly still quite elevated. But will inflation stop the Fed from cutting rates even if the labor market was worsening and a recession looked imminent? Historically, the answer is no. On average, the Fed starts cutting rates six months after CPI peaks. Inflation peaked nine months ago.

Lastly, there’s a growing concern that record money market inflows could actually raise recession risks. As banks refuse to raise their deposit rates, money market funds have seen record inflows while bank deposits have declined.

Assets in money funds have now reached a record $5.13 trillion with more than $238 billion of that being added in the two weeks to March 22. Meanwhile, deposits at US banks recently posted the biggest decline in nearly a year. Per the Federal Reserve, “Bank deposits fell by $98.4 billion to $17.5 trillion in the week ended March 15. Deposits at small banks slumped $120 billion, while those for 25 largest firms rose almost $67 billion.”

So why is the flight to money market funds potentially bad for the economy?

It starts with understanding how money market funds work.

Money-market funds are a type of investment that focuses on highly liquid, cash-equivalent assets. These funds invest in various short-term assets, such as Treasury bills and repurchase agreements (repos). In addition to these investments, money-market funds may also allocate assets to short-term corporate debt.

Right now, close to $2.3 trillion is stashed in the Fed’s reverse repo facility (RRP), which offers an annual rate of 4.80% for overnight cash and is primarily used by money-market funds. The rate on the Fed’s RRP beats out what most banks are offering, with the average one-year certificate of deposit rate lying around 1.5%.

If money funds continue to gain popularity compared to traditional bank deposits, it could maintain or even intensify the downward pressure on banks' reserve levels. Smaller US banks have already experienced a decline in deposits, which raises concerns about potential reductions in lending to businesses and households if this trend persists.

Small lenders are the biggest drivers of lending. Per Goldman Sachs, “banks with less than $250bn in assets account for roughly 50% of US commercial and industrial lending, 60% of residential real estate lending, 80% of commercial real estate lending, and 45% of consumer lending.”

As reserves decline → lending declines / stricter lending requirements / financial conditions tighten → risks of a recession increase

This puts the banks in a tough spot. As Bloomberg writes:

All this puts the banking system at a crossroads. Banks can aggressively boost the rate paid to depositors even though it will still lag money-market yields. They could tap funding avenues like the Federal Home Loan Bank system or tighten lending standards to reduce funding needs. They could also realize losses by selling securities to support loan growth, but that would negatively affect their earnings and regulatory capital.

Thanks again for reading! This newsletter has grown quite quickly over the past few weeks and I truly appreciate each one of you :)

https://www.wsj.com/articles/that-plum-job-listing-may-just-be-a-ghost-3aafc794?mod=hp_lista_pos3

https://www.wsj.com/articles/laid-off-workers-are-flooded-with-fake-job-offers-11673387875

https://clarifycapital.com/job-seekers-beware-of-ghost-jobs-survey//

https://www.ftc.gov/system/files/ftc_gov/pdf/CSN-Data-Book-2022.pdf

https://www.linkedin.com/feed/update/urn:li:activity:7011049036350668800/

https://about.linkedin.com/transparency/community-report#fake-accounts

https://www.bbb.org/content/dam/0734-st-louis/job-scams/JOB%20SCAMS%20STUDY%20v5.pdf

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

https://www.zerohedge.com/markets/feds-first-rate-cut-may-be-right-around-corner