Credit Suisse Backstopped, The Macro Impact of Small Bank Stress, and More Market Technicals...

Credit Suisse Backstopped, The Macro Impact of Small Bank Stress, and More Market Technicals...

Contagion from US bank stress has officially spilled over to Europe, specifically Credit Suisse.

Wednesday saw Credit Suisse’s stock sink to record lows and its bonds collapse. This was all sparked by the Saudi National Bank, Credit Suisse’s biggest shareholder, who announced that it would “absolutely not” inject more cash into the bank.

In the aftermath, short-term debt for the bank sold off as much as 40 cents on the dollar to levels that signal financial distress. The price of Credit Suisse’s 1y credit default swaps, the cost of insuring a company against default, also skyrocketed.

In total, CS stock declined 24%, and European banks fell 8.4%, including a 16.6% decline for the three biggest French banks.

Credit Suisse is just a few months into a restructuring process that involves separating its investment banking unit and focusing on its wealth management business. However, this plan has not been successful in convincing investors or stopping clients from leaving, and the recent collapse of Silicon Valley Bank has added to the market's unease about financials.

Despite this, CEO Ulrich Koerner continued to ask for patience and assured that the bank's financial position is stable, while Chairman Axel Lehmann stated that the bank is not seeking government assistance and its profitability efforts are not comparable to the issues faced by smaller US lenders experiencing liquidity problems.

Credit Suisse has faced numerous scandals in the past including “a criminal conviction for allowing drug dealers to launder money in Bulgaria, entanglement in a Mozambique corruption case, a spying scandal involving a former employee and an executive, and a massive leak of client data to the media”. Fun stuff.

In addition, like many banks, it’s also seen unprecedented levels of client outflows.

And like Silicon Valley Bank, it’s receiving the help of regulators.

In response to the record decline in Credit Suisse's shares and to restore confidence in the troubled lender, the Swiss National Bank, and Finma have jointly stated that the bank will receive a liquidity backstop as it meets the capital and liquidity requirements for systemically important banks.

In the press release, it states “Credit Suisse is taking decisive action to pre-emptively strengthen its liquidity by intending to exercise its option to borrow from the Swiss National Bank (SNB) up to CHF 50 billion under a Covered Loan Facility as well as a short-term liquidity facility, which are fully collateralized by high quality assets”.

In English, Credit Suisse took out a loan with the Swiss National Bank in order to prevent forced asset liquidations (which is what happened to SVB). The problem isn’t solved though… This does nothing to fix the deposit outflows that the bank has been seeing.

The statement does, however, mention that “Credit Suisse is conservatively positioned against interest rate risks. The volume of duration fixed income securities is not material compared to the overall HQLA (high quality liquid assets) portfolio and, in addition, is fully hedged for moves in interest rates”.

Cool, I guess. Disaster avoided and yet another government ‘bailout’ in the books.

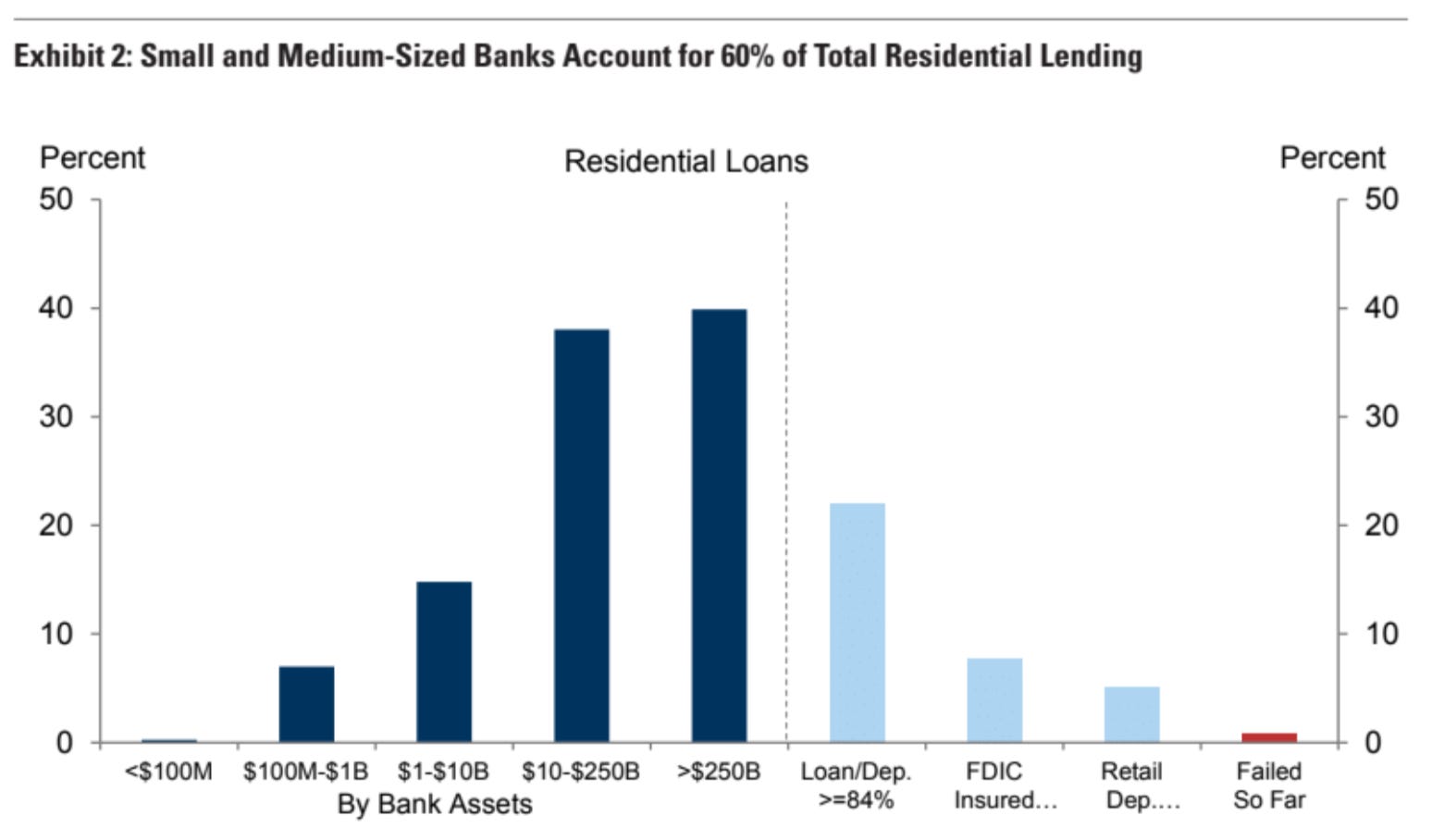

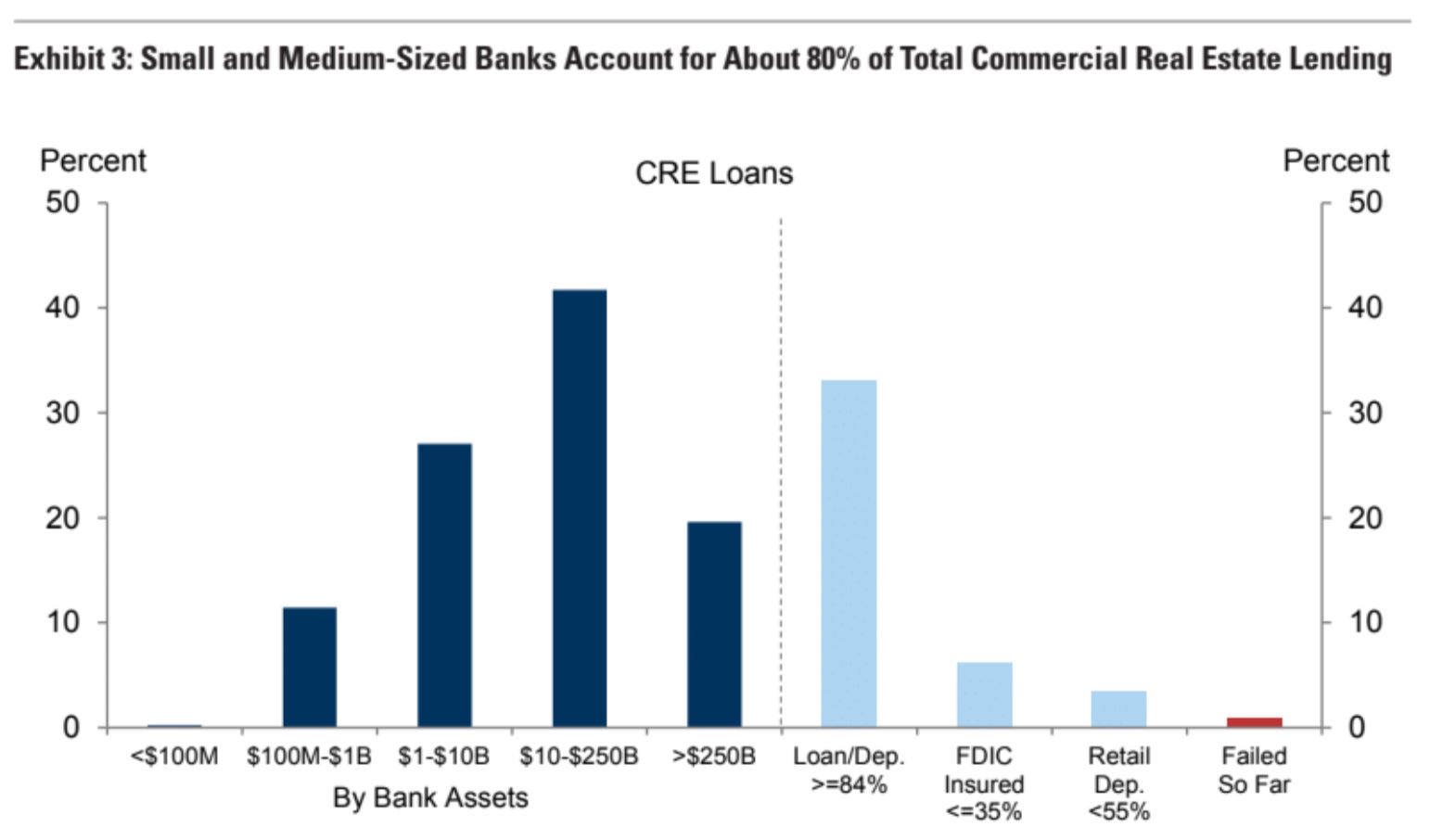

In previous posts, we’ve discussed how smaller banks are at higher risk due to their larger exposure to lending. Banks with less than $250bn in assets account for roughly 50% of US commercial and industrial lending, 60% of residential real estate lending, 80% of commercial real estate lending, and 45% of consumer lending.

Ongoing pressure could cause smaller banks to become more conservative about lending in order to preserve liquidity in case they need to meet depositor withdrawals, and tightening lending standards could weigh on aggregate demand.

In recent quarters, bank lending standards have tightened to levels typically only seen during recessions, likely due to the recession concerns shared by many bank risk divisions. It’s worth noting that lending standards were already tight before the recent small bank stress, meaning that the impact of further tightening may be less significant than initially perceived.

According to Goldman Sachs, “The macroeconomic impact of a pullback in lending will remain highly uncertain until the extent of the stress on the banking system becomes clear… Our analysis implies that the incremental tightening in lending standards that we expect from small bank stress would have the same impact on growth as roughly 25-50 bps of rate hikes would have via their impact on market-based financial conditions”.

This may be partially why the market has been aggressively repricing the Fed’s terminal rate…

Some market technicals to close it off…

“Biggest move in the two year yield since 1987, biggest move in 2s30s since 9/11… plenty of cross market vol but equities aren’t reacting. Over the last year the SPX P/E multiple has had a -65% correlation to rates vol, which at current levels suggests P/E should be 15x – 2 turns lower or an SPX of ~3400” - Morgan Stanley Quantitative and Derivative Strategies Team

Dispersion rose sharply over the last 2 days given the big moves in Financials…

High dispersion means more opportunities in the market…

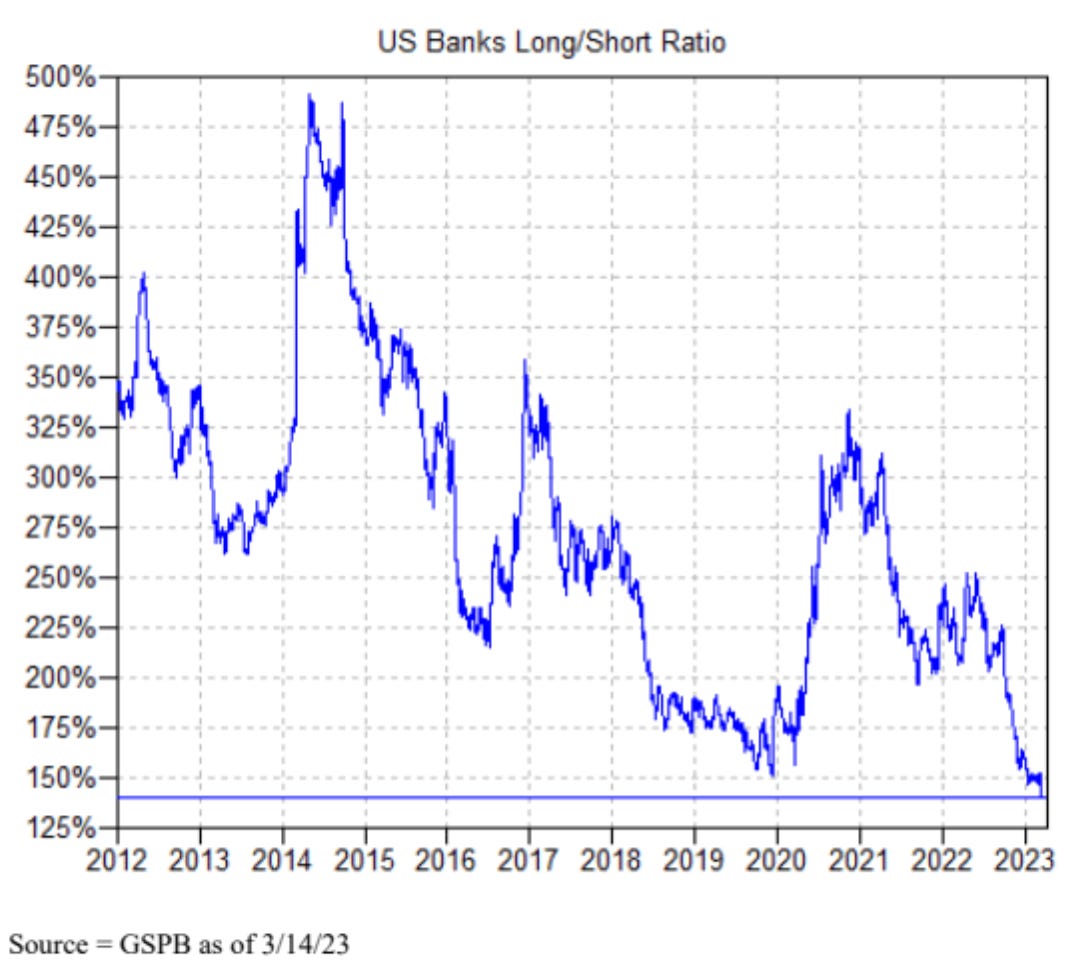

Per Goldman’s Sales and Trading unit, the US Banks Long/Short ratio dropped to fresh all-time lows (140%) and at the fastest pace on record driven by aggressive short selling… Contrarian play is going long on Banks in hopes that the government will bail them out…

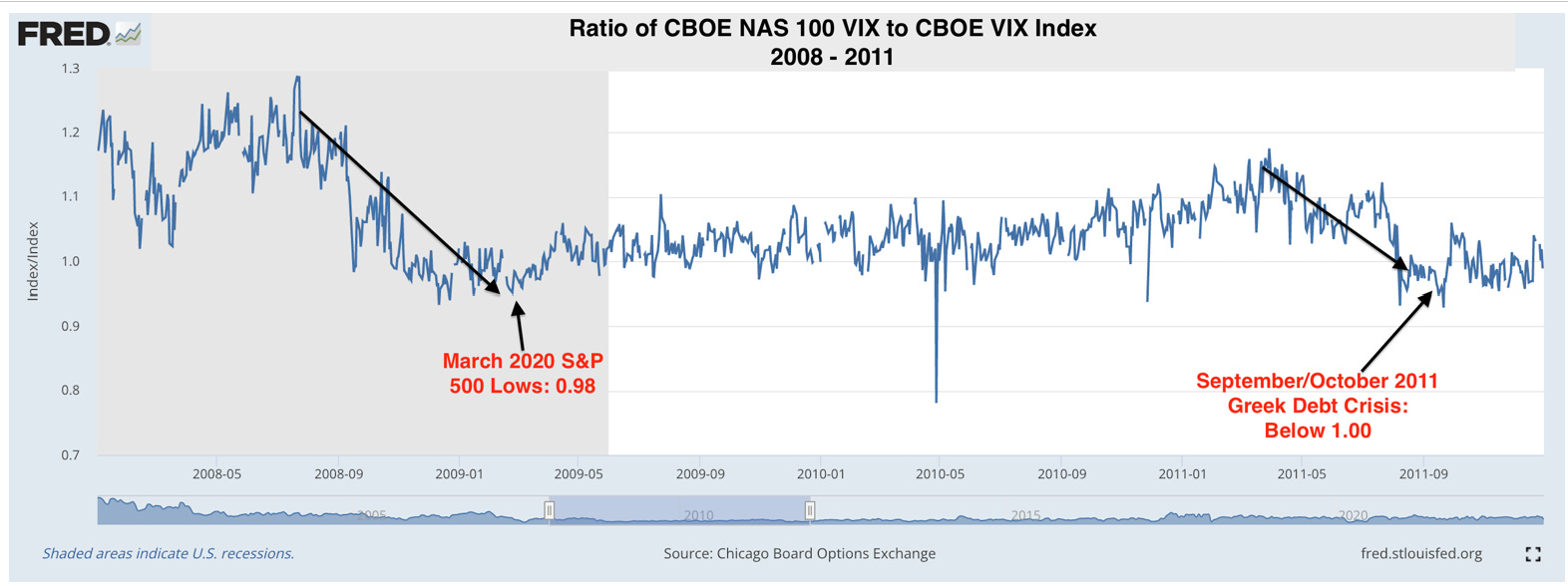

Per DataTrek, “When markets start to worry about systemic financial risk, the relative volatility of the QQQs (Nasdaq 100) tends to fall relative to the S&P 500… During the 2008/2011 Financial and Greek Debt Crises, the ratio of the NAS “VIX” to the S&P VIX went to 1.0x. We are close now (1.1x), but still higher than past signals of market lows”.

“We are close, but not yet at, a level on the VXN/VIX ratio which signifies truly outsized market worries about the US/global banking system. Frankly, this is not surprising. The current situation is not even a week old, after all. The sub-1.0x VXN/VIX ratio readings during 2008 and 2011 occurred only after months of negative headlines and market duress. This is both heartening (there could still be a fix) and concerning (market sentiment can certainly get worse). We continue to recommend caution in either trading the current market or being overly anxious to call a near-term bottom.”

Sources

Research from BofA, Goldman Sachs, JP Morgan, DataTrek

https://www.credit-suisse.com/about-us-news/en/articles/media-releases/csg-announcement-202303.html

https://www.zerohedge.com/markets/credit-suisse-sparks-global-de-risking-after-top-investor-bails