Concerns Around JOLTS Data and Upcoming Volatility

Concerns Around JOLTS Data and Upcoming Volatility

New JOLTs data today showed that vacancies at U.S. employers decreased to 10.87mn in January, from 11.2mn in December. Despite this slight decline, it still beat estimates of 10.5mn openings and highlights the robust demand for labor which has put upward pressure on wages.

So how is the labor market still this strong?

It may have something to do with how the JOLTS (Job Openings and Labor Turnover Survey) is calculated.

“In some cases, jobs in the US must be posted publicly even if they plan to hire internally, but in many cases they don’t. So this could also be influencing the US data.

Possible behavioral changes are compounded by the JOLTS’ dwindling de facto sample size. It covers 21,000 establishments, out of approximately 11 million in total. This is in contrast to the payrolls data which surveys about 400,000 establishments, accounting for about one third of jobs in the country.

But the actual sample size has fallen further due to the collapse in survey-response rates. All surveys have been impacted since the pandemic, but the JOLTS has been particularly affected, the response rate halving to 31% from close to 60% in 2019. Even with the increase in establishments in the survey from 16,000 to 21,000 just before the pandemic, the drop in the response rate means the actual sample size is now 35% smaller.” - ZeroHedge

This is important to know since the predominant narrative is that there is still a super-hot jobs market. This could change at any second. We’ve all already seen the numerous headlines of Tech/RE layoffs…

In Linkedin’s February Workforce Report, it found that hiring is down 23% YoY, most notably in tech (-43.2% YoY) and real estate (-31.2% YoY).

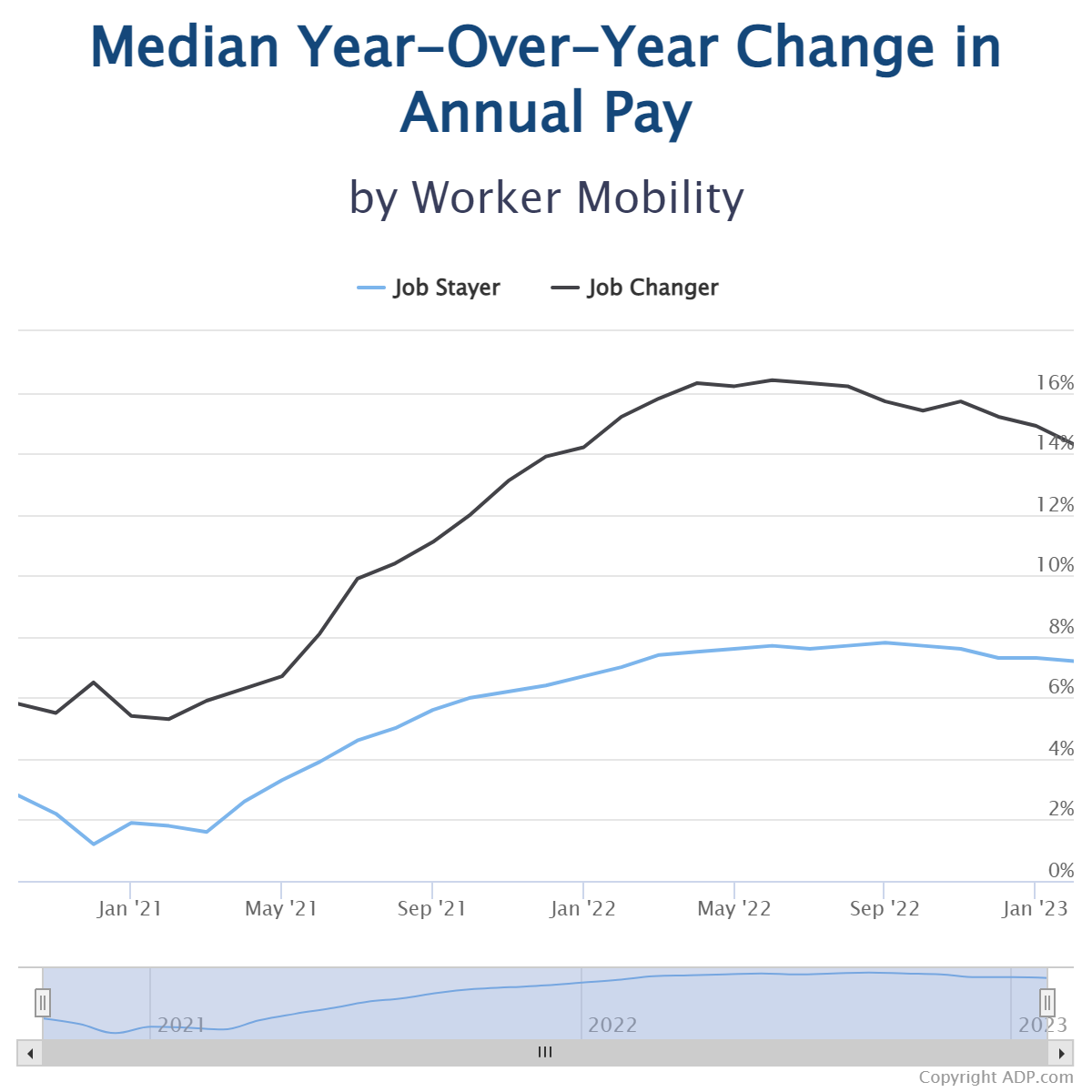

In addition, ADP data recently found that pay growth for job stayers slowed to 7.2% in February, the slowest pace of gains in 12 months. On the other hand, pay growth decelerated for job changers, too, falling to 14.3% from 14.9%.

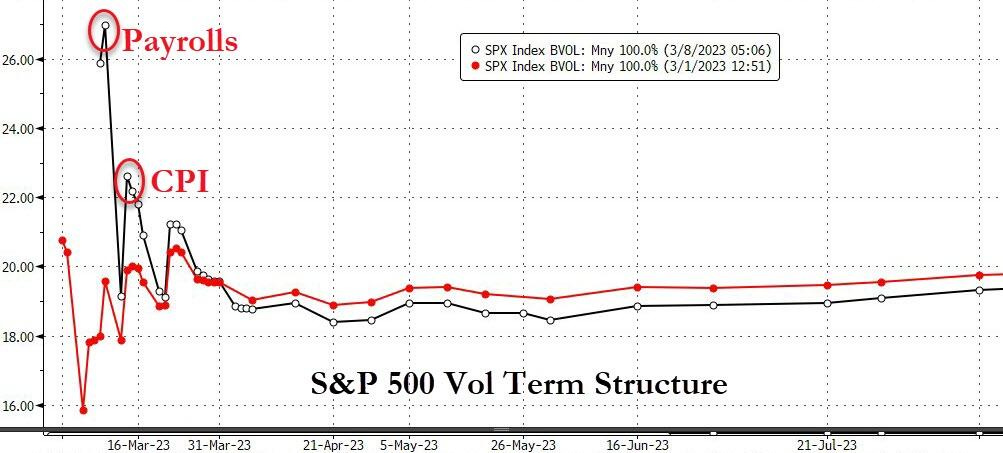

While we continue to wait for more economic data, the markets are continuing to prepare for higher volatility…

VIX call interest has trended higher relative to puts while short-term equity vol is extremely elevated ahead of payroll data and CPI.

It is worth mentioning however that the VIX has decoupled from MOVE (bond vol index) in recent weeks.

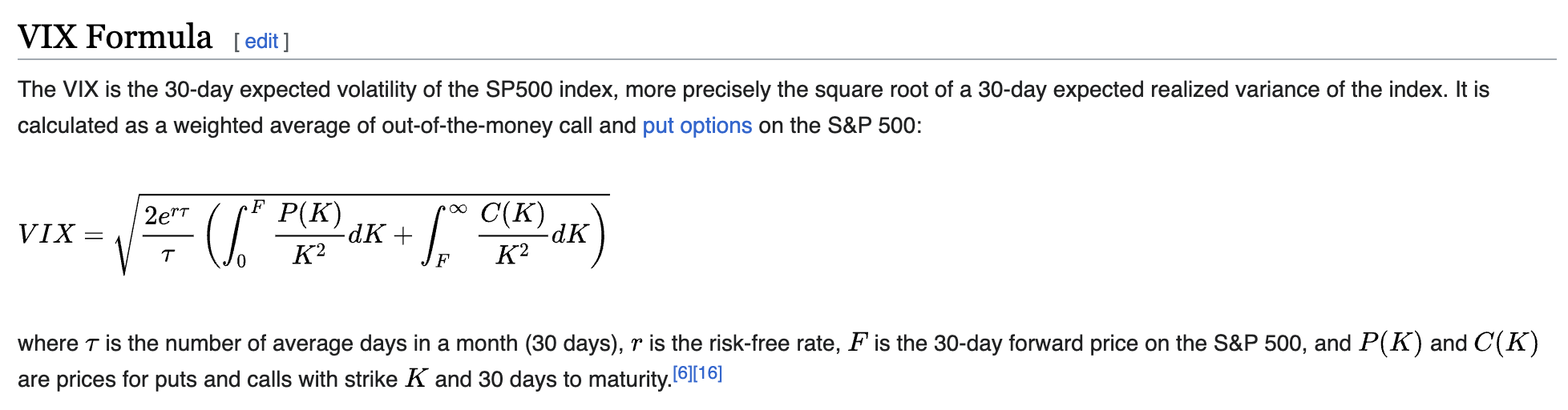

This comes at a time when 0DTE options contracts, have exploded since mid-2022 to as much as 50% of trading volume, at times causing volatile moves in the underlying assets.

So how is this causing a VIX decoupling from its traditional relationship with the S&P 500?

The VIX is the market’s expectations for volatility over the coming 30 days and only takes options expiring in 23 to 37 days from the present as inputs. This means that almost 50% of options trading volume is currently not being accounted for in the VIX calculation.

If you’re planning on using the VIX to hedge your portfolio against vol, I’d caution that it may not deliver the results you are expecting.

Thanks for reading and I’ll see you in the next one!