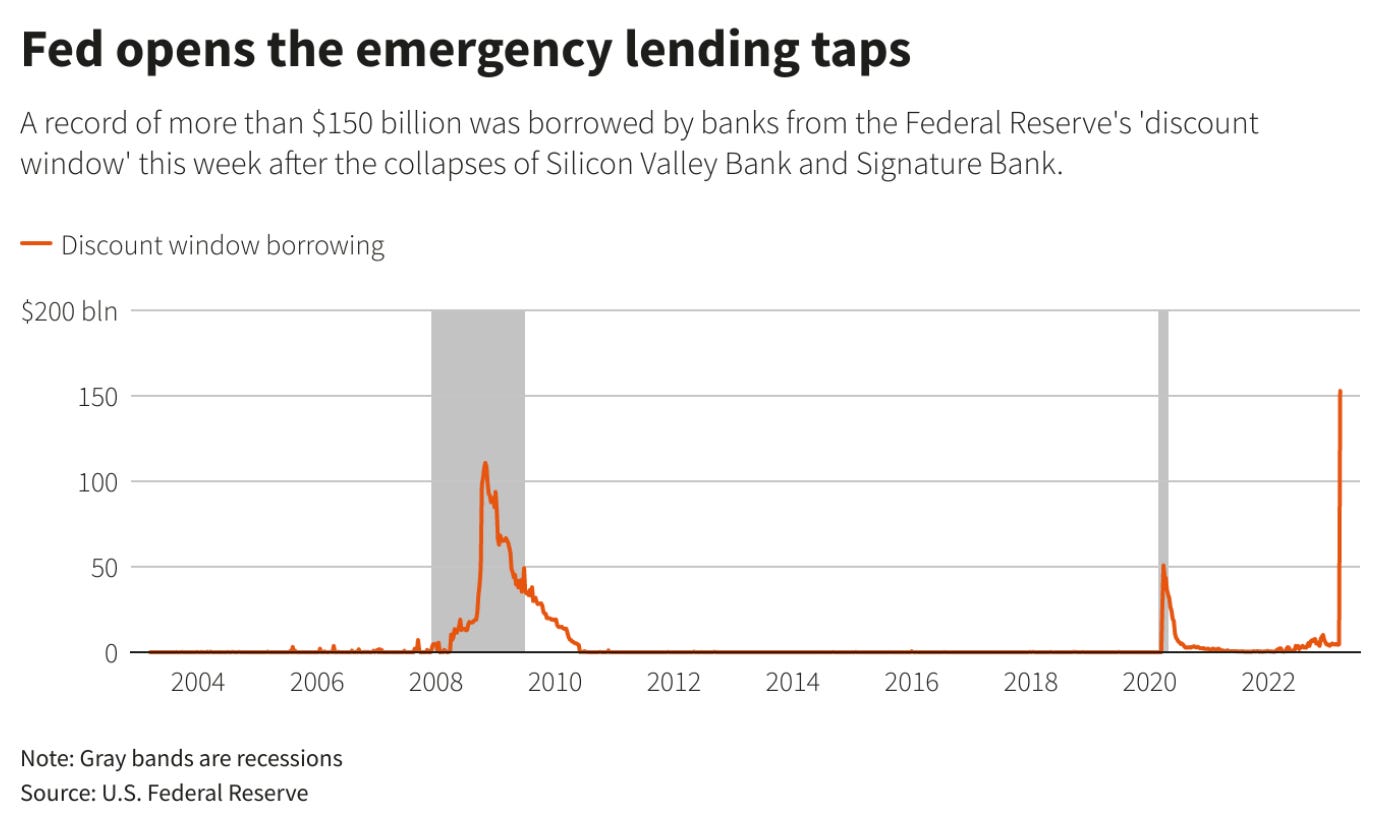

A couple of days ago, we discussed how the banks have been borrowing record amounts from the Fed…

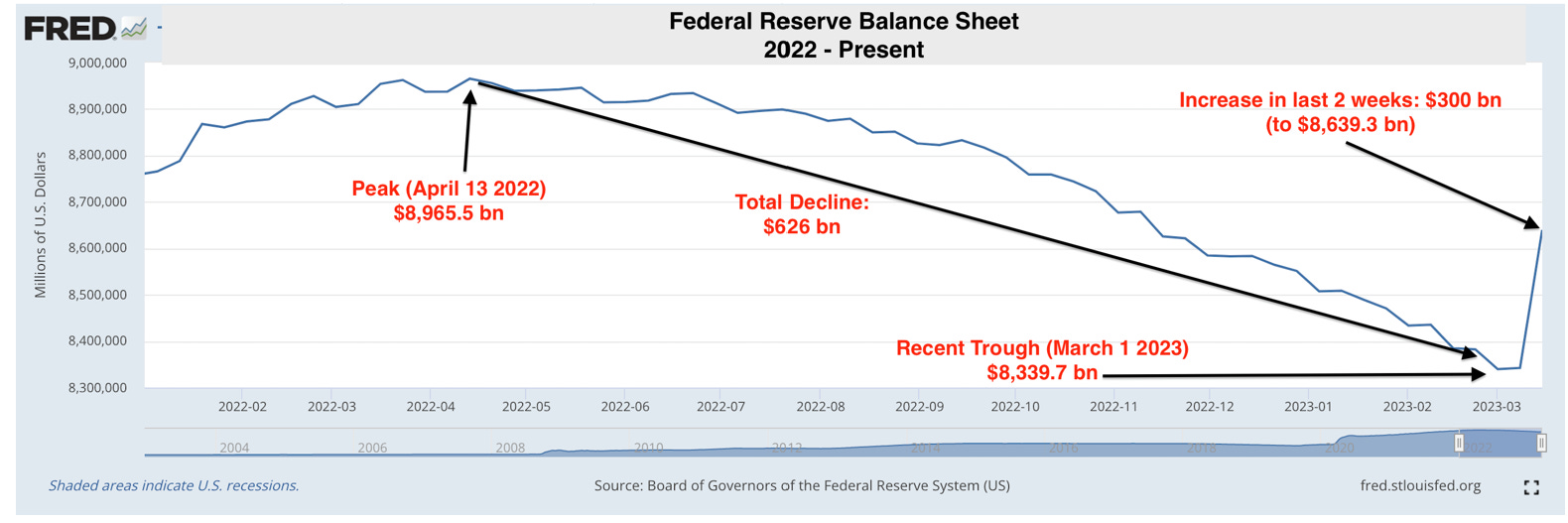

Over the past 2 weeks, the Fed’s balance sheet has expanded by $300 billion, which has reversed almost half the net amount of its 11-month QT program ($626 bn).

There are two major reasons for this change of direction.

The first is an increase of $148 billion in bank usage of the Fed's Discount Window. This is a facility the Fed provides where banks can post collateral and receive cash in return. The discount window usage over the past few weeks trounced the prior record of $112 billion in the fall of 2008, during the most acute phase of the financial crisis.

The second is a $143 billion increase in collateralized loans made to banks insured by the Federal Deposit Insurance Corporation (FDIC).

There was also some pretty interesting news coming out of the Federal Home Loan Banks (FHLB), which is a system of 11 regional banks that act as a backstop used by banks for short-term funding. Yesterday, the FHLB raised $88.7bn via short-term notes. This stoked expectations that many banks will need to tap the FHLB for funds and that this was the FHLB getting ready… As Academy Securities described it, “the offering suggests that there is robust demand for financing as institutions seek to quickly raise dollar funding to replace outgoing deposits”.

Last week, the Federal Home Loan Bank System (FHLB) issued $304 billion in debt, nearly twice the $165 billion that banks borrowed from the Federal Reserve.

Per Bloomberg, “The debt issued last week included notes, which mature in less than a year, and $151 billion in longer-term bonds. The bond issuance eclipsed the nearly $55 billion supplied for the entire month of February and roughly $130 billion for January. Total debt issued last Monday was $112 billion, one of the biggest-ever days of financing for the FHLB system, according to a person familiar with the matter. The next day, the system issued $87 billion in notes and bonds.”

The surge in debt issuance last week indicates that banks continue to have a strong need for cash.

Thanks for reading Quantitative Edge! Subscribe for free to receive new posts and support my work.

Adding to the increasing fear, U.S. officials are reportedly exploring potential methods to temporarily extend FDIC insurance to all deposits in order to prevent a potential financial crisis. Treasury Department staff are assessing if federal regulators possess the sufficient emergency authority to temporarily insure deposits exceeding the current $250,000 cap on most accounts without requiring formal approval from a highly polarized Congress.

Good lord.

So how would this even work?

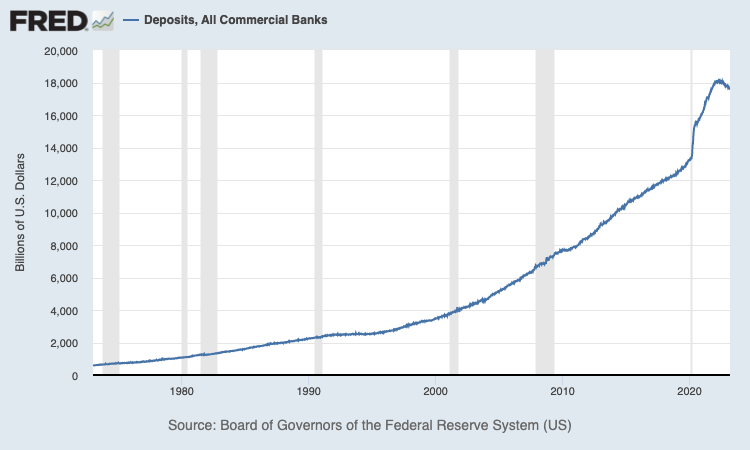

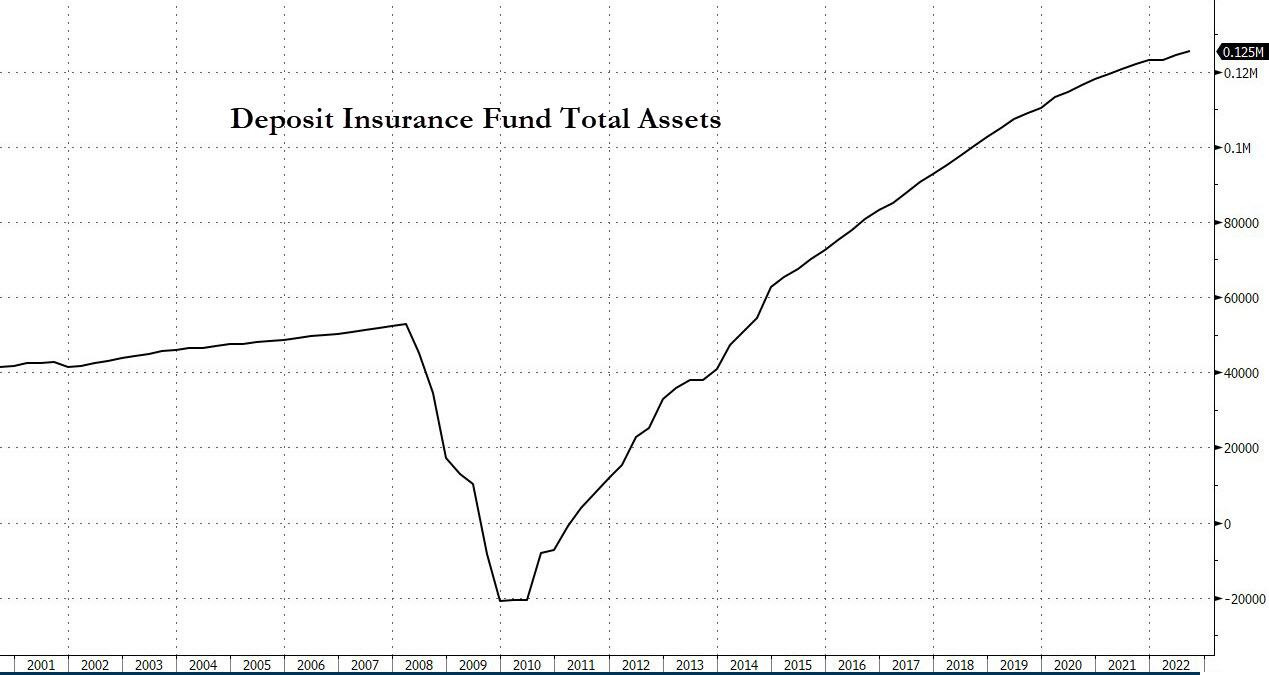

There are currently ~$18 trillion in total deposits at commercial banks and just ~$125 billion in the FDIC's Deposit Insurance Fund. Quite the gap.

So how could the gap get filled? As Bloomberg hypothesizes, it could come through the Exchange Stabilization Fund.

The Exchange Stabilization Fund (ESF) is an emergency reserve account that can be used by the U.S. Department of Treasury to mitigate instability in various financial sectors, including credit, securities, and foreign exchange markets.

The ESF has been used during the 2008 financial crisis and 2020 COVID-19 pandemic to help stabilize financial markets.

But as ZeroHedge pointed out today, “that ESF pot of money is used to buy or sell currencies and to provide financing to foreign governments. A bigger problem: the ESF only has $25 billion currently in it as parts of its BTFP backstop.... but it has to do, as it is the only pot of money under the full authority of Janet Yellen, with other spending and financing under the jurisdiction of Congress.”

Extremely tough situation. But no fear!

“Due to decisive recent actions, the situation has stabilized, deposit flows are improving and Americans can have confidence in the safety of their deposits,” a Treasury spokeswoman said in a statement.

How comforting…

Within the past few weeks, an office landlord controlled by Pacific Investment Management Co. defaulted on about $1.7 billion of mortgage notes on seven buildings in places such as San Francisco, Boston and New York. Before that, a Brookfield Corp. business defaulted on loans tied to two Los Angeles office towers. A $1.2 billion mortgage on a San Francisco complex co-owned by former President Donald Trump and Vornado Realty Trust has showed up on a watchlist of loans that may be in jeopardy. - Bloomberg

While much of the news surrounding the bank crisis has been about Silicon Valley Bank and Credit Suisse, the fall of Signature Bank needs to be talked about more as it will likely cause massive ripples through the commercial real estate market.

Signature Bank was one of the top commercial real-estate lenders in the U.S., especially in New York, where it had a 12% market share.

The bank’s $35.7 billion in real-estate loans accounted for about a third of its $110.4 billion in assets at the end of 2022, according to the FDIC. The bank grew its real-estate loan book by over 4x over the past decade.

No other bank has issued a higher number of commercial real-estate mortgages against New York City buildings since Jan. 1, 2020. Only Wells Fargo. and JPMorgan lent more money.

Commercial properties were already under pressure from rising interest rates. More expensive debt means buyers can’t make an acceptable return on their investment except by paying lower prices for buildings. As property values fall and landlords’ equity dwindles, borrowers have less incentive to make debt repayments.

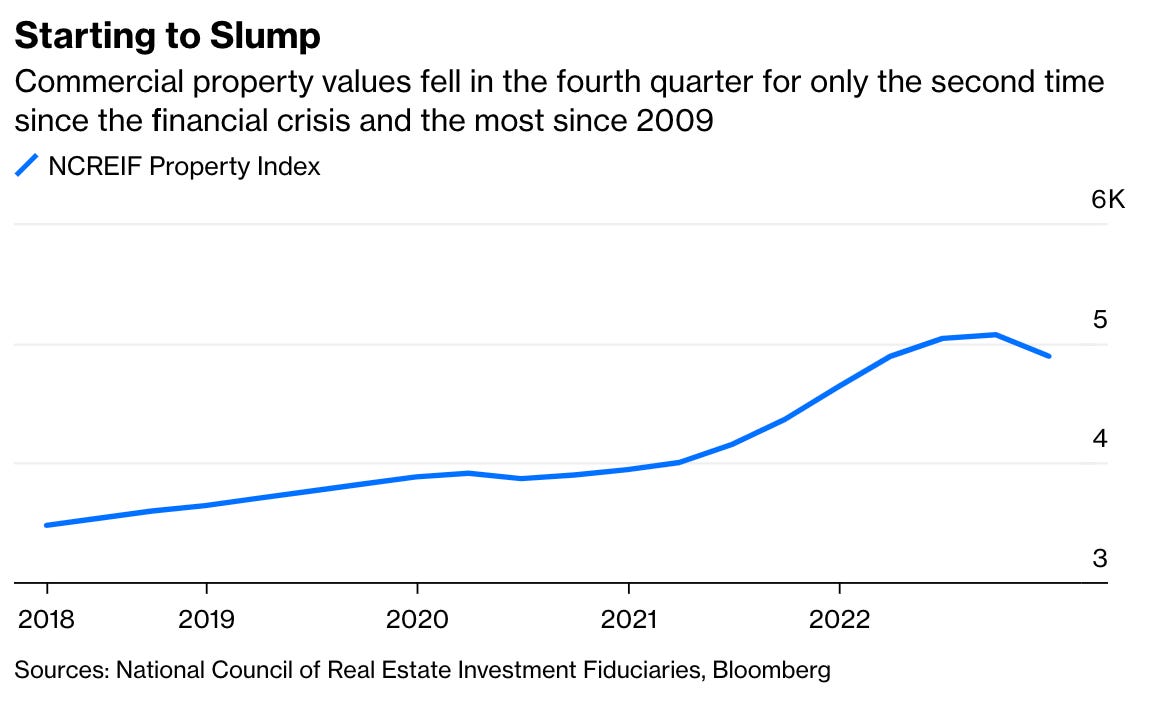

And declining property values are already here. An index of commercial real estate prices published by the National Council of Real Estate Fiduciaries fell 3.5% last quarter, the biggest decline since 2009 and only the second quarterly drop since then. The decline was led by office and apartment properties.

Commercial mortgage-backed securities (CMBS) have already dramatically reflected these growing concerns, with spreads widening as much as 220 bps in the past two weeks.

So where does the risk lie for banks? Likely small/regional banks.

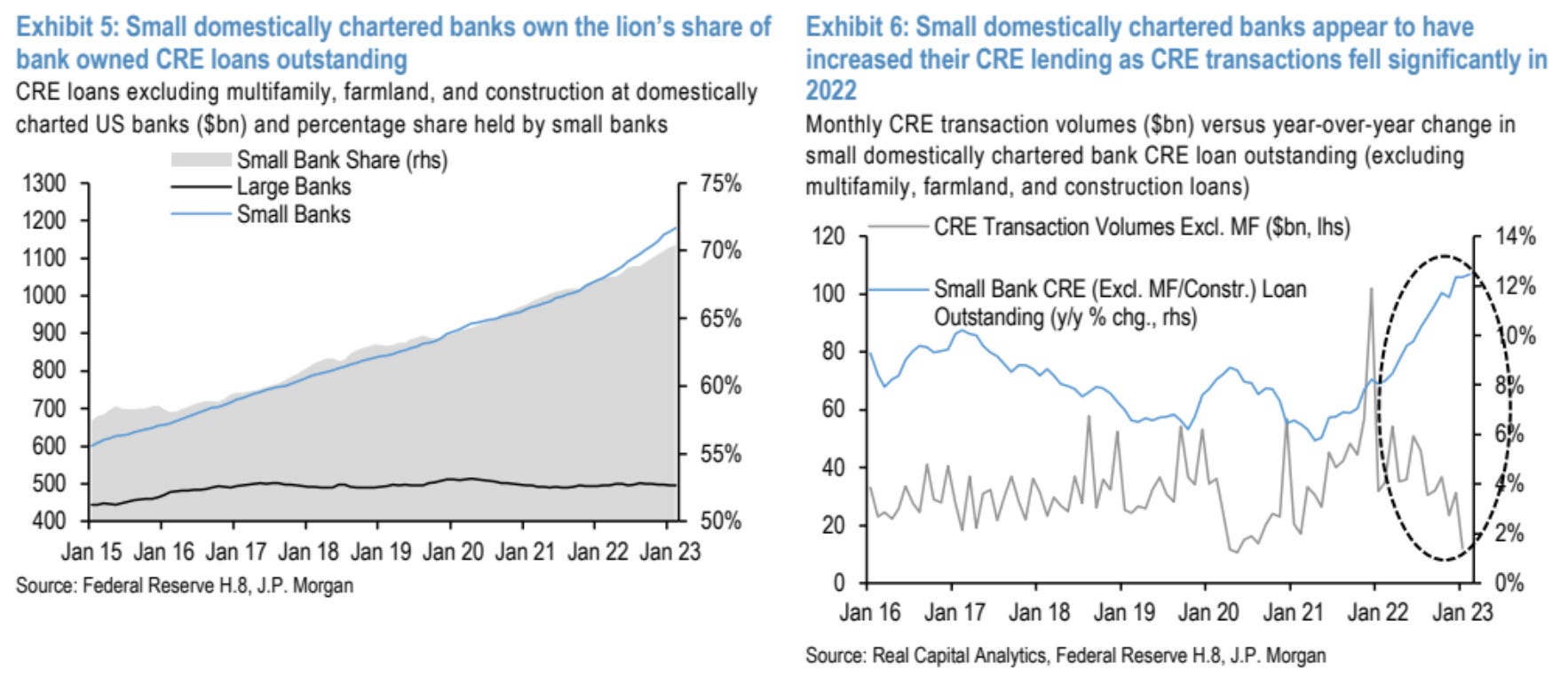

As of February 2023, small bank account for 70% of total commercial real estate (CRE) loans outstanding. This continued growth in market share is particularly notable considering CRE transaction volumes have been declining over that period… These small banks are surely more vulnerable to loan defaults if the market downturn persists or worsens, which could have significant implications for their financial stability.

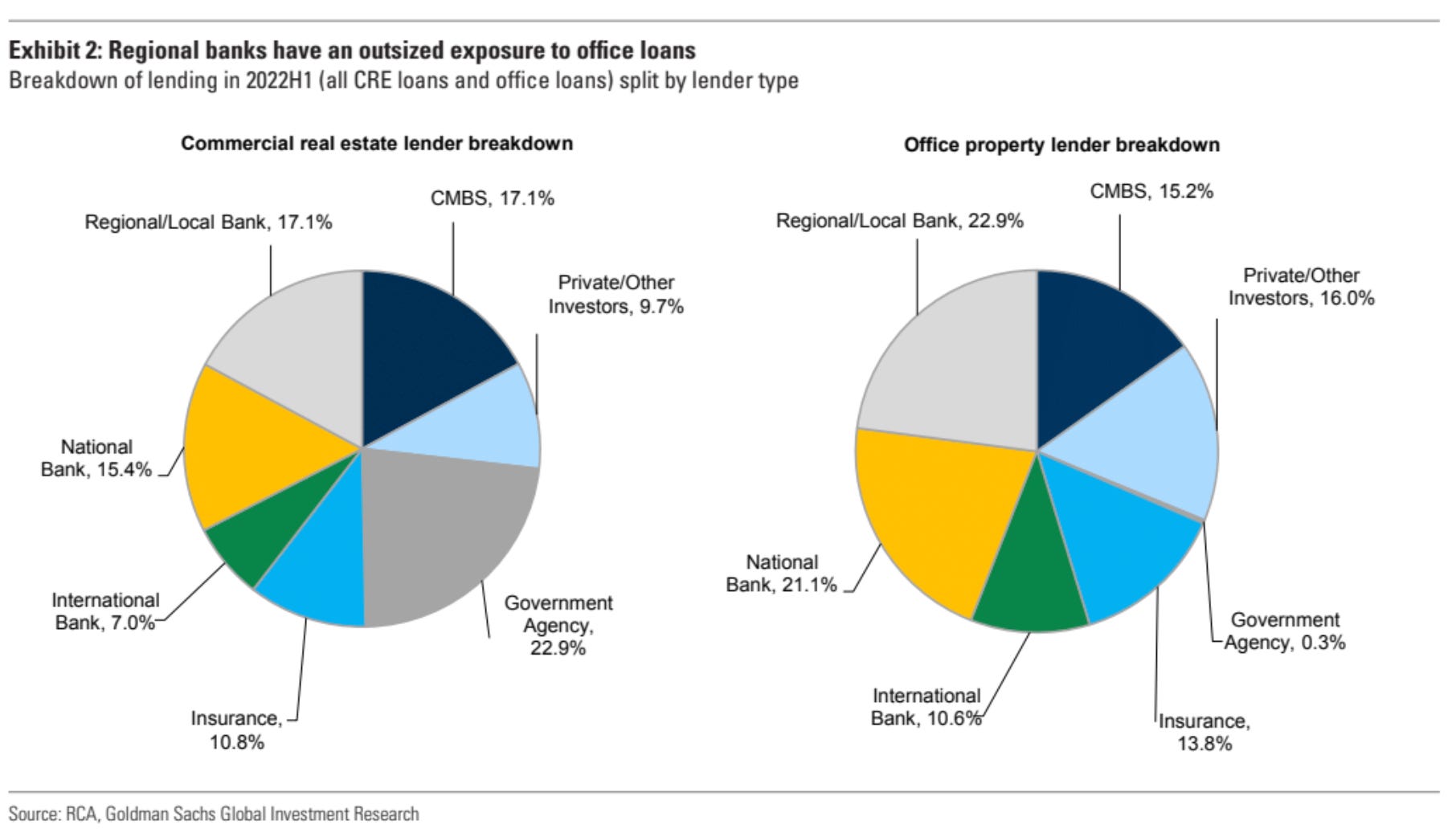

In the chart above, we can see that small/regional bank’s CRE holdings have outsized exposure to office loans, which is quite troubling. Goldman noted that “as office utilization has shrunk by approximately 50% since the onset of the COVID-19 pandemic, the vacancy rate of office properties has grown from 9.5% to 13%. This has pressured rents and leasing activity for office landlords; Green Street estimates that office appraisal values have fallen by 25% over the past year, with a 10% decline in February alone. Consequently, the aggregate level of leverage for office borrowers has grown, with offices composing ~20% of total commercial real estate asset values but ~30% of total commercial mortgage debt.”

Stress on office properties will likely continue, leading to an increase in the proportion of delinquent office loans from the current manageable level of 2.4%. This rise will probably be driven by two primary factors.

First, commercial real estate borrowers are grappling with urgent refinancing and hedging requirements in an environment where debt service costs have significantly risen. Second, falling occupancy rates will likely compel office property owners to reduce rents and/or agree to lesser square footage from tenants as existing leases expire.

Lastly, BofA’s Global Fund Manager Survey was released today and offered some incredible insight into how fund managers with a collective $621bn AUM are thinking about the economy and markets…

Here were the notable highlights from the survey.

Thanks for reading Quantitative Edge! Subscribe for free to receive new posts and support my work.